Wall Street’s passive revolution is turning out to be anything but, with active investing alive and kicking in even the sleepiest corners of the ETF world, according to the latest research.

For all the trillions poured into low-cost index-tracking funds, the U.S. equity market overall is just as active as the halcyon days of the conventional stock picker two decades ago, academics at Cornell University and the University of Technology Sydney have found.

In a new paper, they use exchange-traded funds to upend the established critique of the $11 trillion index frenzy as money-management business on autopilot, with dumb cash blindly chasing companies on the way up and down.

Not only are ETFs being enthusiastically deployed by discretionary managers of all stripes, they’re often designed in more active ways than their detractors would have you believe.

“ETFs are not simply ‘freeriders’ in the market -- investors are still betting on the outperformance of segments of the market, factors, or individual stocks,” wrote David Easley and Maureen O’Hara of Cornell and David Michayluk and Talis J. Putnins of UTS. “Even ETFs in which the holdings are passively linked to an underlying index can contribute to informational efficiency through the active trading by investors.”

Industry pros have for years acknowledged the hidden human hand in passive vehicles. From writing the rules of an index to deciding how a fund will run to actually executing trades and strategies, it’s always been hard to expunge every trace of discretionary involvement.

The paper, titled “The Active World of Passive Investing,” seeks to quantify the true extent of the shift, considering the above factors and the use of index funds in portfolios. It also outlines a separate category of products dubbed “aggressive passive,” or vehicles tracking a gauge that seeks to generate outperformance.

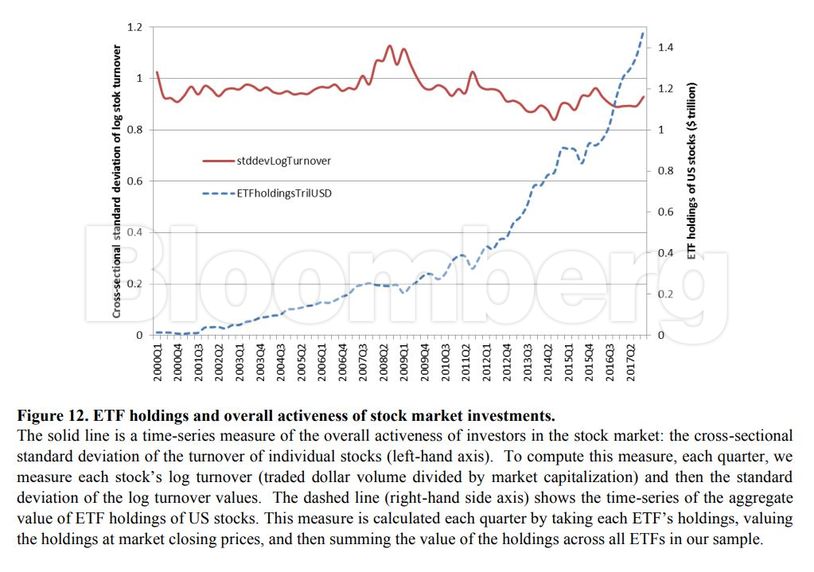

Using data between 2000 and 2017, the group defined two types of active investment for ETFs: form -- where the fund itself is designed to generate alpha -- and function, where the product is used as a building block in a portfolio that is active overall.

They combined these to view fund activeness on a spectrum, with the most passive vehicles being the likes of the Vanguard Total Stock Market ETF (ticker VTI). While this type of fund “comes close” to a completely passive portfolio, they can still be used as hedging tools or form a building block of a bigger, more-active portfolio.

At the other end of the spectrum are narrow industry ETFs and smart-beta funds -- think the iShares MSCI USA Momentum Factor ETF (MTUM) -- that “constitute active bets on some segment of the market or factor.” While these can follow gauges and rules, their structure frequently “leads to an equilibrium closer to that of active management than passive,” the paper says.

Overall the conclusion is that most products qualify as highly active, while both flows and trading activity are concentrated in the most active.

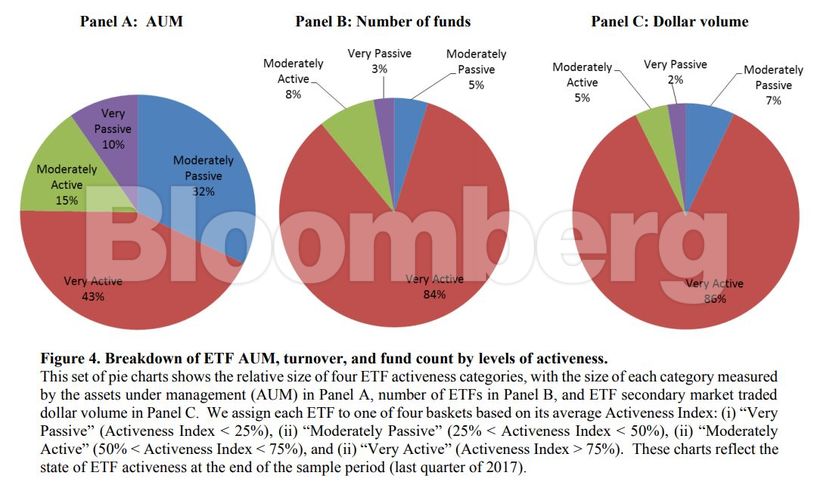

Active-in-form and active-in-function ETFs account for approximately 58% (15% and 43%) of the ETF market by assets, 93% (42% and 51%) by number, and 78% (10% and 68%) by dollar volume traded in the secondary market, the researchers found.

Defining active and passive and understanding how products are being deployed in wider portfolios is a tricky business, leaving lots of room for interpretation. But the study comes after a related paper from a team at the University of Toronto.

In “Closet Active Management of Passive Funds,” the academics showed that a third of supposedly passive index funds and ETFs exhibited more activeness than the median actively managed fund.

All told, the two papers are a rebuttal to naysayers targeting the indexing industry. With more than $11 trillion in index products -- both ETFs and mutual funds -- concerns range from the inefficient allocation of capital to intensified volatility and price distortion.

Still, in their conclusion the researchers from Cornell and UTS hint that, just because ETFs may be less passive than intended, it doesn’t automatically absolve them from all charges.

“Precisely because many ETFs are active investment vehicles, their impact on the market more generally is an important area for future research,” they wrote. “Issues such as whether ETFs enhance market stability, or how ETFs impact liquidity, or whether particular types of ETFs (such as leveraged products or exchange-traded notes) can be harmful seem fruitful areas for inquiry.”

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.