Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

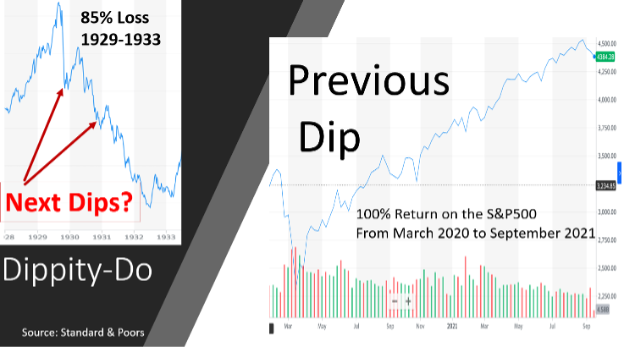

Last year, after the March market correction, I warned baby boomers against buying the dip. Since the market rebounded 100%, that was bad advice. But I double down on that advice today for the same reason. Baby boomers cannot afford the risk. Someday, there will be a series of dips on the way to a prolonged market retreat.

Will the next dip be the first in a long sequence of dips to follow?

One of my most-read articles, Baby Boomers Should Not 'Stay The Course' Because Most Are On The Wrong Course, attracted more than 60,000 readers and was written shortly after the March 2020 market correction.

Readers who took my advice back in July 2020 are surely cursing me now because the stock market recovered big time, doubling in value from its March low. But my advice is the same in this recent dip. In fact, I’m more emphatic this time, in large part because the stock market has reached even higher highs. More baby boomers have entered the “risk zone” spanning the 5-10 years before and after retirement when investment losses can irreparably ruin the remainder of their lives.

Baby boomers cannot afford the 60/40 stock/bond risk that they are taking.

Baby boomer warning extends to their heirs and advisors

There are 78 million baby boomers who collectively own $60 trillion in assets. They are at risk. Research by the Employee Benefit Research Institute (EBRI) reports that the average baby boomer is invested 60/40 stock/bonds. despite the danger of sequence-of-return risk. A 60/40 allocation lost more than 30% in 2008, but boomers were not in the risk zone then. Now, most boomers will spend much of this decade in the risk zone.

I wrote my book, Baby Boomer Investing in the Perilous Decade of the 2020s, as a warning. But too few people have read the book. There are two compelling reasons for baby boomers to protect their savings at this critical time in their lives: (1) losses in this decade could ruin the rest of life – that’s risk management; and (2) the economy is fraught with peril – that’s market timing.

When someone says, “It’s different this time,” they are usually wrong. But check out these five reasons it is different this time:

- Bond yields have never been lower, so bond risk has never been higher

- Stock prices have never been higher.

- The U.S. government has never printed more money. M1 money supply has quintupled in two years from $4 trillion to $20 trillion.

- The wealth divide has never been greater, creating havoc in Seattle, Portland and Chicago.

- There has never been 78 million people all simultaneously in the risk zone

Non-boomers, especially young investors, should be concerned about these threats too. But they are likely to live long enough to recover from whatever damage is caused. That said, those who rely on baby boomers should be concerned about domino effects befalling upon them

The wisdom of buying dips

“Stay the course” and “buy the dips” are common mantras that have worked every time since 2008, which is roughly the investment lifetime of millennials. But as shown in the following picture, the day will come when buying the dip will not be smart. The odds of a long-sustained correction are high in light of the five threats listed above.

Better safe than sorry

As I warned last year, baby boomers should not play the buy-the-dip game because their lifetime savings are at stake, and the next recession could outlive them. By “safe” I mean 70% in low-risk, inflation-protected assets like TIPS, real estate and precious metals.

Ron Surz is co-host of the Baby Boomer Investing Show and president of Target Date Solutions and Age Sage, and CEO of GlidePath Wealth Management.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.