How the 4% Rule Undermines Advisors and Clients

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Do-it-yourself investment tools that help individuals build their retirement savings are perceived threats to the advisory business model. But building a nest egg is not where advisors add their greatest value.

Rather, advisors should distinguish themselves by managing the distribution of those retirement savings. And the complexity of this function cannot be displaced by simple rules of thumb.

When building retirement savings, portfolio diversification and consistent account contributions will serve an individual well. Advisors play a key role in managing clients’ behavioral impulses so that they don’t veer from that model, but these basic guidelines work.

When it comes to drawing down a portfolio, however, simple rules are deeply flawed. Investors who choose to follow rules of thumb do so at their own peril.

Dissecting the 4% rule

The golden rule of withdrawal rates is, of course, the “4% rule.” It suggests a simple way to draw down your nest egg by withdrawing 4% during the first year. In following years, adjust that withdrawal amount in line with annual inflation, and you should be able to safely fund a 30-year retirement.

Though the research from the mid-1990s that gave rise to the 4% rule never suggested that everyone should follow it, the industry and popular media have touted the rule and turned it into conventional wisdom. Its simplicity encourages many retirement savers and retirees to take a DIY approach to wealth planning, letting that basic rule dictate their entire retirement path.

But the 4% rule often leaves considerable money on the table and robs individuals of the retirement they deserve. Retirement income planning requires sophistication. By accounting for the full range of inputs to a plan, advisors can help clients understand they may be better off than they thought and give them the confidence to enjoy retirement.

There are three primary reasons the 4% rule is misguided and should be done away with when it comes to retirement spending.

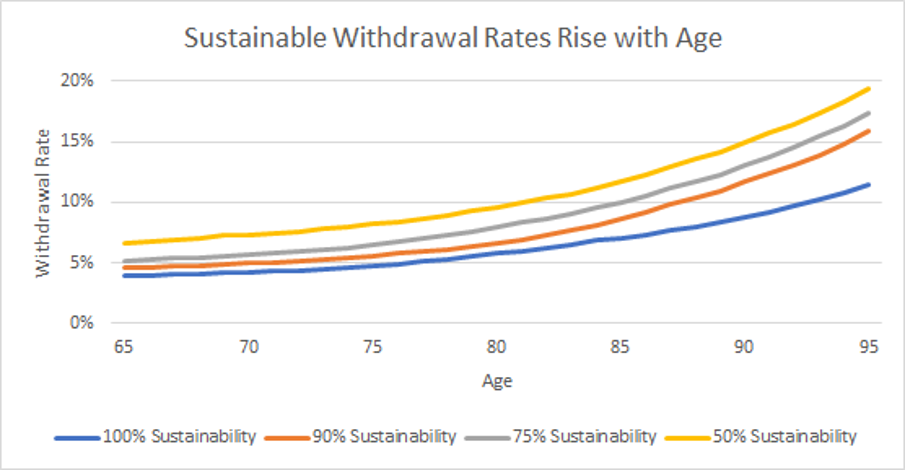

The first is longevity. An individual’s age and health deeply affect one’s withdrawal rate. With a shorter planning horizon, the risk of any withdrawal rate is lower. It may be perfectly safe to switch to a higher withdrawal rate at, say, age 80, than the rate someone is using at age 65.

The chart below puts the dynamic relationship between longevity and withdrawal rates in perspective. It shows the withdrawal rate that could be taken from a 60/40 stock and bond portfolio at various levels of “sustainability,” defined as the estimated chance that a portfolio would survive a given withdrawal plan to the end of, or past, the corresponding planning horizon.

Each sustainability line arcs upward. If an investor planned to retire at age 65 and felt comfortable knowing there was a 75% chance their nest egg would last 30 years, the investor could start retirement with a 5% withdrawal rate (already much higher than the 4% rule suggests). As the person ages and medical costs increase, the withdrawal rate could continue to rise without increasing the probability of running out of money.

Source: Author’s calculations from Society of Actuaries RP-2014 mortality tables.

A 4% rule overlooks the fact that investors can increase their withdrawal rate as they age, without taking on more risk. It leaves the investor less confident about what they can spend in retirement, and what income will be available when they get older.

The 4% rule overlooks realistic spending trends

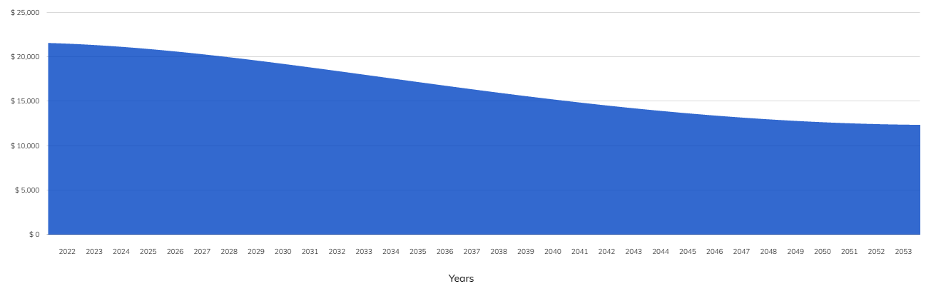

Longevity isn’t the only reason the 4% rule fails investors. The rule also locks retirees into maintaining the same purchasing power through retirement. If a couple is spending $10,000/month in 2021 at age 65, the rule assumes they will also need $10,000/month, in today’s dollars, in 2041 at age 85.

But research on spending patterns in retirement does not support this assumption of flat, inflation-adjusted spending. Instead, retirees often spend the most early in retirement, followed by a long period of decreases in inflation-adjusted spending. Toward the end of life, some may increase their inflation-adjusted spending for medical reasons. This pattern, sometimes called the “retirement smile” or the “go-go”, “slow-go”, and “no-go” years, looks like this:

Source: Income Lab

Planning for realistic spending needs goes a long way toward providing more income to individuals in the early phase of retirement, when they need it most, without depriving them of the income they need later in life. But this requires moving beyond simplistic rules of thumb.

Non-portfolio cash flows add complexity to the distribution puzzle

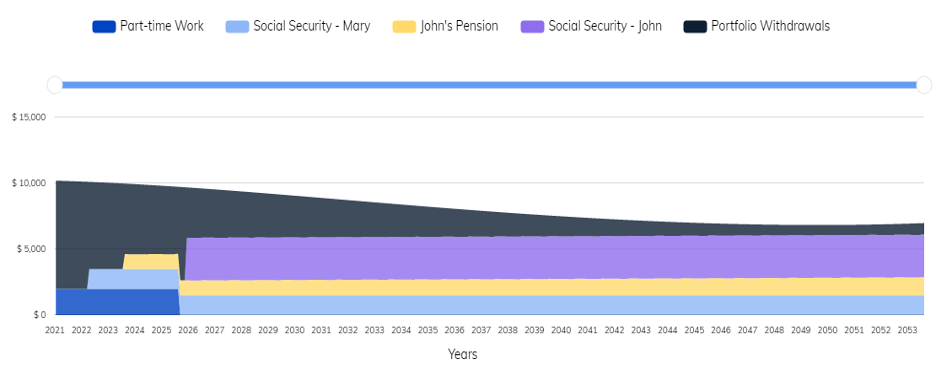

Yet another flaw with the 4% rule is that it fails to acknowledge that non-portfolio cash flows are typically a major source of a retiree’s income. Social Security, pensions, rental properties, part-time jobs, house downsizing, inheritance, etc. make the actual cash flow picture for most families quite complex.

The chart below serves as a hypothetical example for a retired couple. It is a glimpse of what retirement often looks like. It assumes part-time work for five years, a pension, and two Social Security income streams (one at full retirement age and the other at age 70).

Source: Income Lab

At first, only portfolio withdrawals and part-time work will be used to fund retirement income, leading to an initial 9.8% withdrawal rate. As Mary’s Social Security and John’s pension kick in, annual planned withdrawals would decrease to approximately $79,000 and $63,000 respectively. After a brief increase in withdrawals when John stops working part time, his Social Security begins, and withdrawals reduce further to $46,000. Because of the retirement smile, withdrawals continue to decrease in real terms, going as low as $9,000/year later in the plan.

The complexity of these different cashflows makes following a withdrawal rate rule of thumb impossible.

Distribution planning: An advisor’s biggest value-add

Debates over whether DIY investment platforms enable an investor to plan retirement without an advisor often focus only on building the portfolio. That debate is misleading. While advisors add value in investing, the argument overlooks the advisor’s greatest value add: retirement income planning.

Income distribution is the most complex aspect of the retirement puzzle. The multiple variables that come with it require complex and dynamic planning, not rule-of-thumb thinking. For an advisor, this is one of the greatest ways to add value.

Johnny Poulsen is the co-founder and CEO of Income Lab. Before co-founding Income Lab, Johnny worked for more than 24 years in financial services sales, distribution, and executive management, most recently at Jackson. He received an MBA from City University of Seattle and studied business law at Syddansk Universitet (University of Southern Denmark). Johnny is a Certified Financial Planner™ (CFP®) professional.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All