Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Just as leaves fall in autumn, you can count on the financial press1 to litter websites and other media with year-end “take losses and re-balance your portfolio” stories.

There is nothing wrong with taking losses and adjusting allocations as the year end nears. However, much of this activity, prompted by the press or lazy advisors who haven’t been paying attention during the year, amounts to little more than a squirrel’s frantic seasonal hunt for acorns.

His survival depends on his gathering as many nuts as possible – thus his frenzy. Fortunately, investors’ financial health is not dependent on the specific time of year or on how much activity can be accomplished before the snows come.

Yes, tax losses are tied to a specific year. Investors and their advisors do need to pay attention to the calendar.

However, it is far better to make changes to portfolios throughout the year as the opportunities and conditions present themselves. Pay attention to the fundamentals of the stock, fund, or ETF or allocation considerations as they change and not to what month it is.

From here until the turn of the calendar, assets will fall prey to year-end dumping, as investors are pressured to rebalance before December 31. Mutual funds and institutional investors will tweak their holdings as they window dress portfolios for year end, further distorting asset prices.

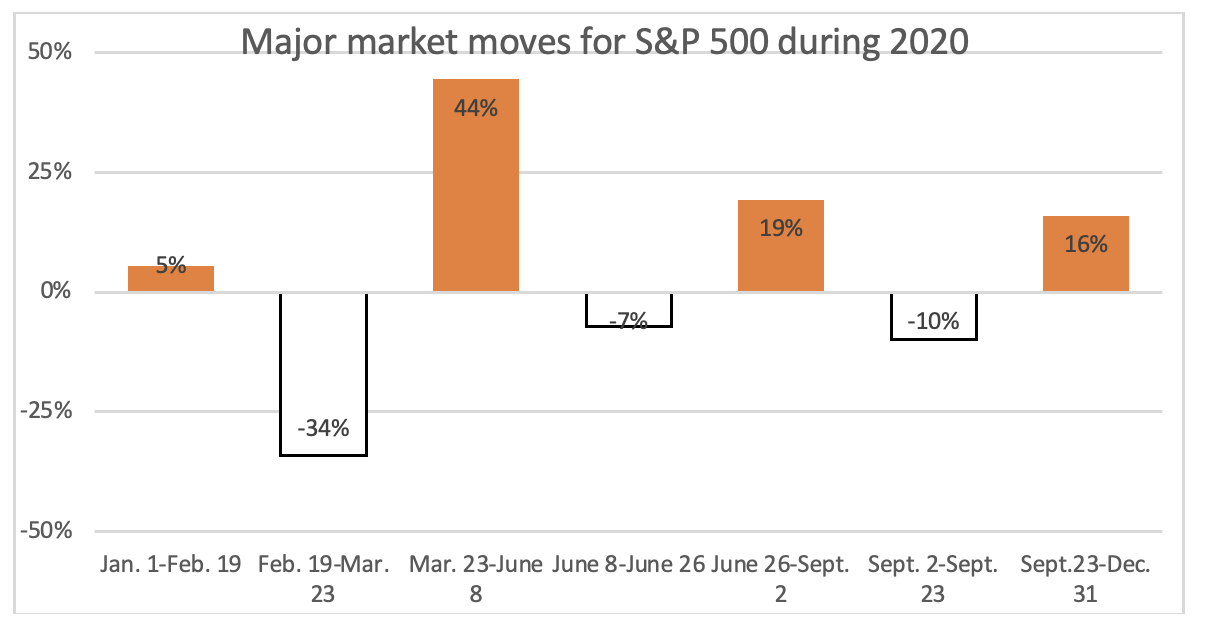

Last year, was a perfect example of why you need to pay attention and take advantage of losses when they occur, not just wait until the “harvest” season. Starting in February 2020, the S&P 500 fell 34% in roughly a month as the full impact of COVID hit investors.

Change in price of S&P 500 index for time period shown during 2020.

From there through early June, the index marked a 44% rebound. It bounced around some more, finally ending up 16% by year end. More importantly, recovery rates varied widely across individual sectors and industries – opening all sorts of opportunity to adjust positions.

No one rings the bell to announce the market top or bottom, but a sharp decline should be your call to action to consider taking losses and properly leverage tax-related harvesting opportunities. Last year, most of those opportunities were gone by the time the financial media turned to its evergreen “time to harvest/rebalance” stories in the late fall.

Tax-loss harvesting shouldn’t wag the portfolio management dog. A particular asset should be held based on a sound reason, one that can be articulated and still applies. When it doesn’t is the time to consider removing it from the portfolio – be it February, June or November.

If investors focus too much on just balancing gains and losses and not underlying fundamentals, they overlook deteriorating situations in the middle.

How many times have you looked at an account statement and scanned the list of stocks or funds for winners and losers? It’s human nature to look at just the outliers.

An individual stock may be keeping up with the S&P 500 or other broad market index, hiding in the middle, even as its sector or industry has been red-hot. That stock has actually underperformed, and it bears investigating why.

Better to figure it out then, before fundamentals catch up and it falls to the bottom of the list. It is all too easy to use short-term performance as a shortcut for measuring the health of the portfolio’s constituents. Look at what is going on with all the names on the list.

Tax-loss harvesting or any other end-of-year-prompted activity is just a tactic in service of strategy. The tactic looks to take advantage of the calendar and tax accounting. The larger strategy is about maximizing wealth while controlling risk over an investor’s timeframe, which generally is long-lived with no precisely knowable endpoint.

Don’t squirrel your portfolio!

Please do follow the good advice you’re bound to see in the weeks ahead recommending you look for tax-loss harvesting or rebalancing opportunities in your or your clients’ portfolios. Just don’t do it because you feel you should do something by year end. Look for the moments throughout the year or as cash needs and risk tolerance dictate and make sure the situation calls for a sale or a change.

Otherwise, that activity is just the random, frantic equivalent of a squirrel stashing acorns.

Ted Everett is a CFA and an investment advisor and financial writer in Boston. He helps financial service companies create readable and insightful investment-thought leadership whitepapers and other content. He has edited and written extensively for various investment newsletters and served as portfolio manager and trusted advisor for families, trusts, smaller institutions, and non-profit entities.

1Excluding Advisor Perspectives.