JJ Walker and the Stoking of the Medicare Frenzy

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

We’re in the middle of the “Annual Medicare Frenzy.” Truly, I wish we could re-name the Annual Election Period.

This time of year means lots of things to lots of people. The commercials on TV are in high gear, postcards are filling up in mailboxes and the Medicare call centers are out in full force.

Consumers are stressed. Even if they are not enrolled into the Medicare system, they’re stressed! They truly believe that they have something to do during this “open enrollment” even if they are turning 65 in a year.

They have nothing to do.

They’re not enrolled into the system. How could there be anything for them to do…!

But the marketing wins. It raises the antennae on every person close to or enrolled in Medicare.

Agents

We’re stressed. The phone lines blow up. People become impatient. Their particular drug plan with their one generic medication is far more important than anyone else’s and they need immediate answers on October 15 even though the final day to file a plan change is December 7.

(Being facetious here.)

We can use some Zen Medicare moments – please be kind to your agents.

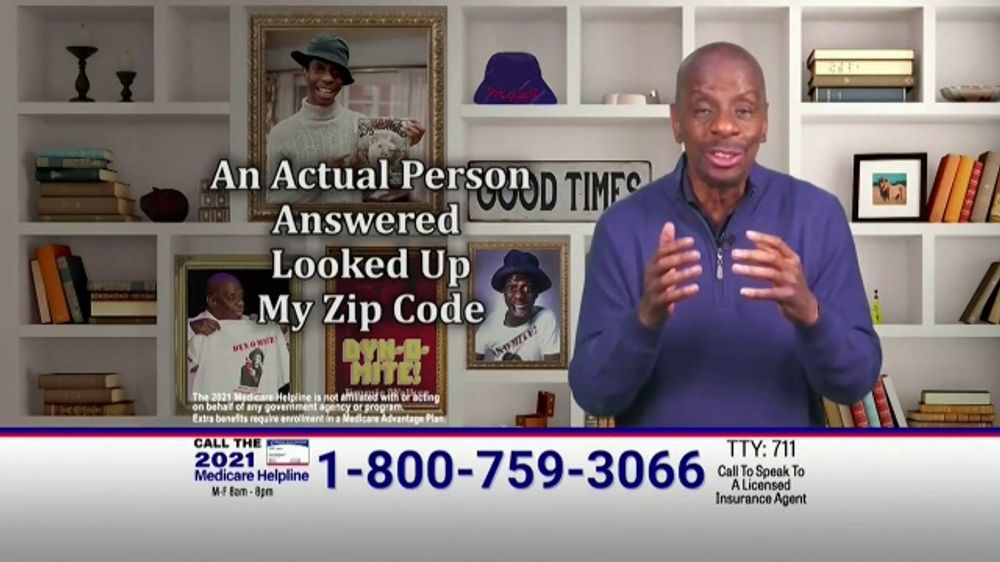

Enter JJ Walker

My husband started Medicare on October 1. I put his Medigap plan in place, added his drug plan, and he complained that he didn’t have any dental coverage when he went to the dentist a week later. The usual in my world! No surprise at all.

What surprised me was when he walked in the other day and asked, “Do you know who JJ Walker is?” (Last year it was Joe Namath, now it’s JJ.)

Oh boy. “You aren’t serious, right? Why do you ask?”

Jeff: “I heard him on TV saying that you can get $100 a month added back to your Social Security. I took down the phone number.”

Jeff the guinea pig

Perfect, since he wrote the phone number down, I had him call to see what happens next.

He called the call center and talked with “Cindy.” It was a comical conversation (for me) and I let him ask all the questions that a person new to Medicare would ask.

We taped the conversation and created a video that I sent out to my firm’s clients. They loved it. It was the most successful email that we’ve ever sent.

The entire concept circles around “there is no free lunch.” Unless you are enrolled in both Medicaid and Medicare, JJ Walker will not be sending you that $100.00.

My guess is that Cindy was hired for the season. She didn’t know that Medicare Part B premiums are based on income. She said it’s just not true - everybody pays the base rate.

She did her best to frame Medicare Advantage plans as good for a healthy 65-year old, which they can be. Just don’t get sick and want to change your plan. Ever.

Reality

Every single October 15, we have the same discussions over and over with our clients. “I just saw this on TV where I can get….. And …. And…. what are they talking about?”

And it’s true! You can leave your Medicare supplement plan (a.k.a. Medigap) plan behind and get a Medicare Advantage plan if you’d like. Your new plan will begin on 1/1/2022. You even have 12 months to “try it out” if you’d like. We don’t encourage people to buy the product based on using trial rights, however. It rarely works out well.

What will typically happen is that the person changes to Medicare Advantage, and then four years later a health event occurs and then they want their old Medigap plan back. There’s no guarantee that they’ll get it back. They’ll be medically underwritten and can be declined.

Here’s why this annual frenzy is so harmful.

The “frenzy” marketing infers to the public that you can just “change your plan whenever you want to.” Like crashing your car on Tuesday and upgrading your coverage on Wednesday thinking that’ll work.

Neither works.

The harm that comes with that thought process for the consumer is evidenced in this recent conversation I had with “Matt.”

Matt is turning 67 next spring. After two years on his Medicare Advantage plan (which has worked very well), he’s starting to feel the desire to “upgrade” his coverage, he said. After a few tests for this and a few tests for that, he said he’d feel better having more coverage going forward.

His friend who purchased a Medigap policy with us suggested that he call.

I asked him some basic questions about his health, and he divulged a condition that is a “no-go” on every Medigap application out there. He’s not getting approved. He was shocked that he couldn’t change because this was the time of year to do so.

I explained the process to him and then asked, “When you turned 65 and bought your current plan, how did you make the selection? Who did you call?”

He called 1-800-MEDICARE.

I’m not a fan of purchasing your coverage in that manner (calling Medicare or an insurance carrier directly). This is one of the reasons why.

Agents

There’s a lot of value in purchasing your coverage through a good agent and agency.

What most people don’t know about our industry is that when a person enrolls in a plan (either type), the agent is paid a first-year commission. Then, depending on the product and the carrier, we might get paid for a few more years, for 10 years, for lifetime if that person stays with the plan, etc. It varies quite a bit.

Now, the numbers aren’t huge, but we are paid fairly for our work.

When a person contacts the carrier directly to enroll, that carrier certainly doesn’t pay an agent and is happy to keep the compensation.

Three years later when the consumer needs help with something, they’ll call agencies like ours because their friend told them that we helped them as they transitioned to Medicare.

We do not take on that client. There is no way to become the “agent of record” and get paid. We can be the servicing agent, but not an agent that gets paid to service the account.

I’ve had some advisors balk that we “won’t’” help their client. All I’ll say is that we do plenty of free work, but we are not counselors nor do we work for Medicare, the government. And, the financial advisor who says that certainly does not do all of the counseling/advising to the client while allowing his competition to be paid on the AUM.

Finale

We’ve had hundreds of email responses from our JJ Walker video clip. This one jumped out at me:

Not sure what it says about us when advertisers think we'll trust old sit-com actors and concussed former football players with some of the most important decisions of our lives.

During this chaos-filled Medicare time, please steer your clients to get good help and make good Medicare decisions. Know that they are stressed even though they don’t bring this up to you.

You have a role in all their financial matters.

Reinforce the notion that you cannot just “change your plan” during the Annual Election Period.

Encourage them to read our blog here or listen to our Transition to Medicare podcast as we discuss how to have a successful election window as a consumer.

Medicare is an enormous piece of that puzzle. Please be part of the solution with us.

Joanne Giardini-Russell is a Medicare Nerd & the owner of Giardini Medicare, helping people throughout Michigan and AZ, CA, FL, IA, IL, IN, MI, MD, NC, OH, PA, SC, TX transition to Medicare successfully. Contact the team at [email protected] or by calling 248-871-7756.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All