Monetary policy has driven U.S. stock prices to excessive valuations, according to Jeffrey Gundlach. But they remain cheap relative to bonds.

Monetary policy has driven U.S. stock prices to excessive valuations, according to Jeffrey Gundlach. But they remain cheap relative to bonds.

Gundlach is the founder and chief investment officer of Los Angeles-based DoubleLine Capital, a leading provider of fixed-income mutual funds and ETFs. He spoke to investors via a conference call on January 11. Slides from that presentation are available here. This webinar was his annual forecast for the global markets and economies for 2022, and its title was, “I Feel Young Again.”

The title related to the late 1970s, when Gundlach was in the third grade, inflation was high and real rates were negative. The difference, of course, is that rates are much lower now than then.

Before we look at Gundlach’s 2022 predictions, let’s see how well his forecast from last year, which I reported on here, held up:

- U.S. equities will underperform the rest of the world – U.S. equities, based on the S&P 500 ETF SPY, returned 28.6%. The rest of the world, based on the MSCI all-world ex-U.S. ETF ACWX, returned 7.46%. Incorrect.

- Inflation will rise – Inflation, as measured by growth of the CPI-U index, was 1.4% in 2020 and 6.8% for the first 11 months of 2021. Correct.

- Volatility will be higher – Volatility, as measured by the average VIX closing price, was 29.25 in 2020 and 19.67 in 2021. Incorrect.

- The dollar will weaken – The dollar, as measured by the DXY, was at 89.93 at the close of 2020 and at 95.97 at the close of 2021. Incorrect (although, in fairness, Gundlach has always stated that the weakening of the dollar is a long-term, not short-term prediction.)

- He was “neutral” on gold – Gold, based on the ETF GLD, returned -4.15% in 2021. Correct.

- The yield curve will steepen – The yield curve, based on the spread between two- and 10-year Treasury bonds, was 80 basis points at the end of 2020 and 79 basis points at the end of 2021. Rates overall were high, however, as Gundlach predicted. Tie.

- Bank loans were his number one recommendation and they earned 5.2%. Correct.

- He was bullish on commodities, and those did well, led by oil, which returned 59.7% based on the WTI index. Correct.

That is four correct, three incorrect and one tie.

Stratospheric equity valuations

Numerous metrics for the equity market signal overvaluation, according to Gundlach

Long-term real returns for the S&P 500 have followed an orderly, cyclical pattern for the last 100 years. Those returns are now at the peak of a cycle and at the highest level since the dot-com peak.

The Nasdaq has outperformed the S&P 500 by a greater degree than it did leading up to the dot-com peak. But that outperformance stopped over the last 18 months, which Gundlach interpreted as a warning signal. The Nasdaq “breadth” has collapsed, in that the percent of its stocks above their 200-day moving average is less than half compared to the start of 2021.

Since 2010, U.S. stocks have strongly outperformed the rest of the world (by a factor of three). That has left European stocks priced cheaply, according to Gundlach.

The U.S. is “really, really expensive.” The P/E ratio of the rest of the world is at its lowest point relative to the U.S. in the last 15 years.

He expects European stocks to outperform the U.S.

Emerging markets are another story, though. They are below their peak prior to before the global financial crisis and are “not in store for robust returns,” he said, and he doesn’t expect profits from them in the short term. But emerging markets will outperform the U.S. in a down market. Emerging markets will be a great trade on a multi-year view, but they have to “prove themselves first,” he said.

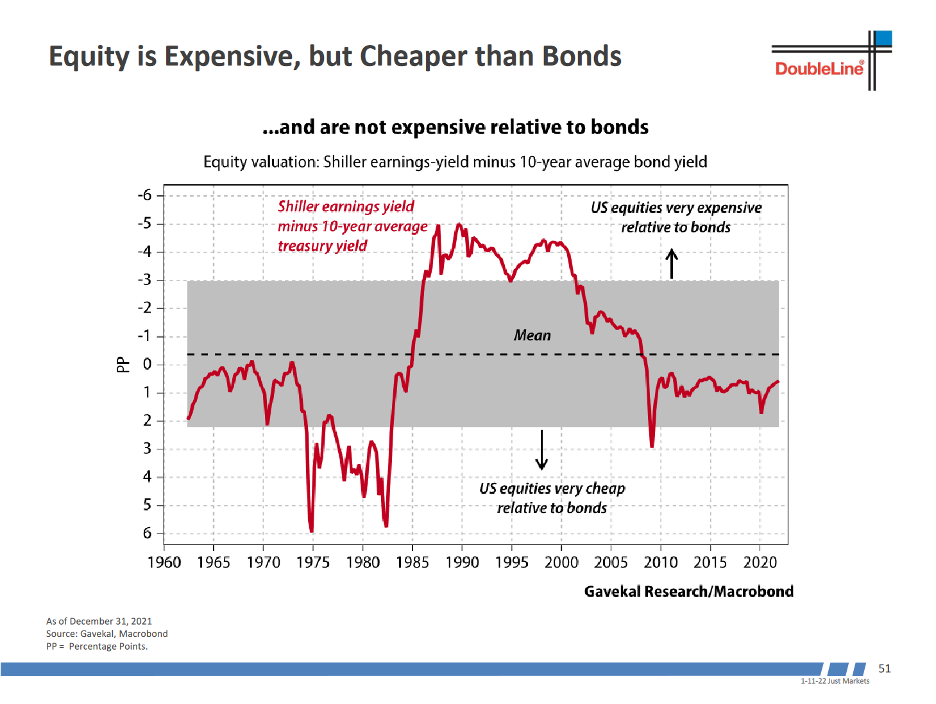

To support his view that equities are attractive relative to bonds. Gundlach cited the chart below:

The red line shows the Shiller “earnings yield” (which is the inverse of the Shiller CAPE ratio) minus the 10-year Treasury yield. That line is below its mean, which implies that investors should expect historically low returns from bonds relative to stocks in the future.

What makes bonds alarmingly unattractive are negative real rates. As I discuss below, the real Fed funds rate is -6.7%.

Gundlach expressed concerns about rising rates when he spoke about Fed policy. He said Fed Chairperson Jerome Powell is getting more hawkish about the need to raise rates, especially since he “pivoted” in November (when Powell stopped referring to inflation as “transitory”).

Powell is talking about repeating the “playbook” from late 2018, Gundlach said, which includes higher rates and tighter monetary policy (i.e., quantitative tightening).

Powell will do “almost whatever it takes” to control inflation, he said.

But the bond market is not sending an inflationary fear signal yet. Inflation expectations, based on U.S. five- and 30-year TIPS breakeven rates, have not risen.

The economic backdrop behind Inflationary fears

The central debate among economists has been whether inflation will be temporary or long-lasting. Gundlach said that in 2021 he was hawkish on inflation, but not hawkish enough.

He expects a core 5% and headline 7% CPI-U inflation for the full 2022 year.

Inflation will remain elevated in the first half of 2022, and after that, it will depend on Fed policy, Gundlach said. It will be higher than most people think, and he noted that many economists are forecasting CPI-U inflation of 2.25% by third quarter, which he called “wishful thinking.”

Inflation, according to Gundlach, is driven at least in part by monetary policy that has fueled consumer spending.

U.S. equity prices have gone “vertical” since a bear market in 2018. Spending on goods since then closely resembles the pattern of rising stock prices, as does the increase in the Fed’s balance sheet. Spending on consumer goods grew by approximately the same amount in two years post-COVID as it had in the prior 10 years.

“It is undeniable that the economy has been supported by quantitative easing (QE),” he said. “When that goes away, so do the tailwinds.”

But he did not predict a recession.

Government transfers have fueled the economic expansion since 2020, he said, but we are now back on trend. That is even though a substantial portion of GDP was “ginned out of the sky,” he said, driven by government-issued debt. Some of that support will stop later this year, he said, providing a headwind to economic growth.

But consumer sentiment has failed to recover based on the University of Michigan sentiment survey. It is at 70.6, a recessionary level, the lowest it has been since the short pandemic recession in early 2020. This is driven by the fact that consumers believe it is a bad time to buy a car or a house, he said.

Used car prices are up 46.6% over the last year, leading some consumers to buy out car leases and “flip” their autos to a new owner. Home prices are up by as much as 25% for the last 12 months, he said, and this is off a high starting point from a year ago. With mortgages at 3.25% and inflation running more than 6%, home financing is quite cheap, Gundlach said.

The supply of single-family homes has declined steadily since the end of 1999, when it was 12 months. It is now at two months, which will keep the housing market from having any stress, assuming mortgage rates don’t increase. Houses have remained affordable, since wage growth is outpacing mortgage rates.

Container ships waiting to be unloaded are up ten-fold since mid-2021, but have started to come down, which signals abating inflation. Shipping rates are still elevated, though, he said. Import prices up 12% and export up 18% year-over-year; both of those values are “off the charts” and are at or near their highest levels in 30 years, which supports an inflationary outlook.

Jobs have become harder to fill and wages are rising. Previously, Gundlach has said that younger workers were benefiting from those wage increases. But in the last few months, he said that has “blended up” and extended to the other age-based cohorts.

Further support for wage-based inflation came from a Gallup that asked whether it is a good time to find a quality job; it had its highest reading in 20 years. Another poll showed that 58% of people are considering changing careers, particularly among healthcare workers and teachers.

Asset class forecasts

Gundlach offered a few forecasts for asset classes.

He reiterated that he is bearish on the dollar over the long term, “over at least a couple of years.” He is neutral in the short term. The dollar is broadly correlated with the twin deficits (trade and budget), he said. The budget deficit has started to contract over the last six months, which is a signal of waning government support for the economy.

The dollar has also followed the slope of the 2- to 10-year yield curve. The worst, most crowded trade last year was that the yield curve would continue to steepen in March of 2021, he said. That turned out to be the wrong view.

If that slope decreases to less than 50, it would be recessionary.

He is neutral on gold. On a multi-year view, though, he is bullish, corresponding to his bearish view on the dollar.

The real Fed funds rate is -6.7%, which is an “incredible” stimulus for borrowing. The shadow Fed funds rate, which incorporates the effect of QE, is 8.7%, which means that QE has brought the effective real Fed fund rate down by another 200 basis points.

But as tapering continues, he said, that effect will wane.

The Fed funds rate typically tracks wage growth and the dollar, but those patterns have diverged over the last few months, which Gundlach took as a sign that the Fed may be “asleep at the wheel.”

The copper-gold ratio has tracked 10-year yields but opened a gap starting in early 2020. Gundlach said that is due to foreign investor demand for 10-year bonds. Those investors favor U.S. debt over negative-yielding bonds in their domestic markets.

The scariest recessionary signal is from the five- to 30-year yield-curve spread, which has contracted by 50 basis points since Q3 of last year, as the five-year yield has risen. Short term, one- and two-year, rates have risen by 40 to 93 basis points over that period. Indeed, Gundlach said that the two-year Treasury yield leads to tightening and loosening cycles, and is a de facto replacement for the Fed.

Gundlach said that the Fed could get to 1.5% on the Fed funds rate, which might happen in the next 12 to 18 months. But that would trigger a recession.

He closed his presentation by noting that the U.S. banking sector has remained much healthier than those of Europe and Japan over the last several decades, because we have not pursued policies of negative rates.

“Thankfully the Fed has not talked about negative rates,” he said. “But who knows? When the next problem comes, the order of magnitude of the stimulus will follow the pattern we’ve been living in for decades, in that it gets ever bigger and more emboldened.”

“When the next recession comes, I think the U.S. is going to have a challenge on its hands about what to do with the Fed funds rate, particularly if it has to reverse course after raising rates to only 1.5% or so, which may very well be the case.”

Robert Huebscher is the editor and publisher of Advisor Perspectives.

Read more articles by Robert Huebscher

Monetary policy has driven U.S. stock prices to excessive valuations, according to Jeffrey Gundlach. But they remain cheap relative to bonds.

Monetary policy has driven U.S. stock prices to excessive valuations, according to Jeffrey Gundlach. But they remain cheap relative to bonds. The red line shows the Shiller “earnings yield” (which is the inverse of the Shiller CAPE ratio) minus the 10-year Treasury yield. That line is below its mean, which implies that investors should expect historically low returns from bonds relative to stocks in the future.

The red line shows the Shiller “earnings yield” (which is the inverse of the Shiller CAPE ratio) minus the 10-year Treasury yield. That line is below its mean, which implies that investors should expect historically low returns from bonds relative to stocks in the future.