Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Income investors have long been attracted to master limited partnerships (MLPs) for their generous, tax-advantaged yields. With the Alerian MLP Index (AMZ) yielding 7.5% as of January 21 and other income investments offering yields well below historical averages, investors are revisiting MLPs as they look to enhance portfolio income. Inflation concerns are also causing investors to consider the MLP space, given that these investments offer real-asset exposure and typically have contracts with built-in inflation adjustments.

But what’s the best way to gain exposure to this space, especially if you don’t want a K-1 at tax time? To reap the potential tax benefits of MLP investing and to make sure the allocation is meeting an investor’s needs, it’s important to understand the nuances of MLP investing.

Despite the tax advantages provided by MLPs, some investors have been reluctant to allocate to the space because they do not want to receive a K-1 for filing taxes. A direct investment in an individual MLP will come with a K-1, but several investment products provide MLP exposure and a form 1099 instead.

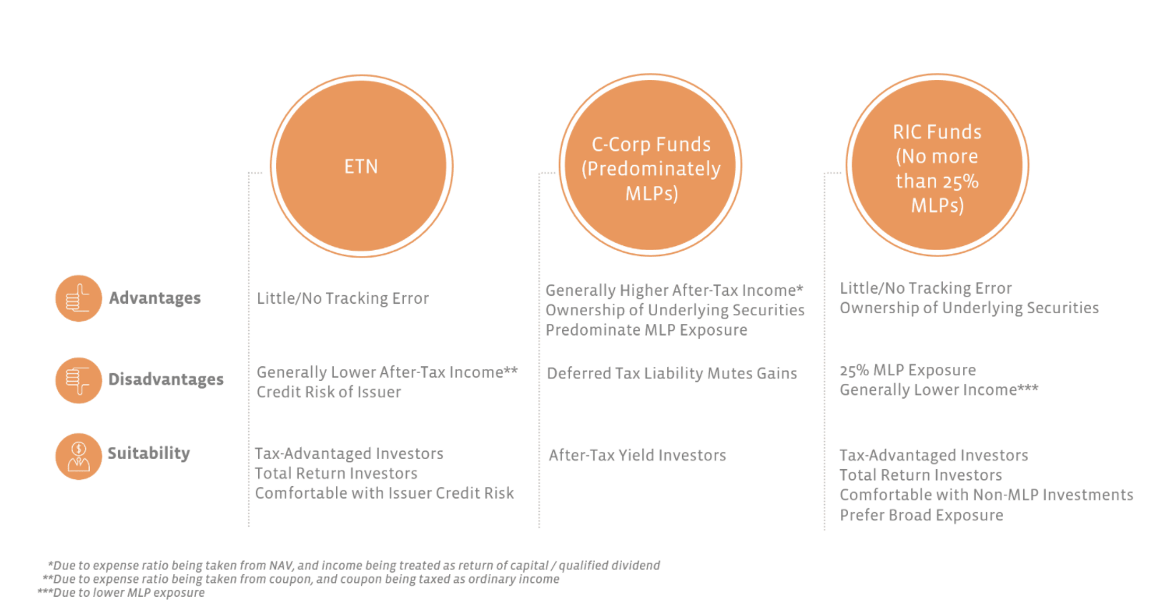

Picking the right investment product depends on investor preferences and the type of account. The following graphic displays some key considerations for each product:

Source: Alerian

MLP investing in tax-exempt accounts

The primary tax advantage of investing in MLPs is the potential for tax-deferred income. An investor can own a tax-advantaged investment in a tax-advantaged account, but that approach tends to be suboptimal. It’s a bit like wearing both a belt and suspenders. Investors are typically better off owning investments that take advantage of the special tax treatment of the account. Additionally, unrelated business taxable income (UBTI) could be generated by owning an individual MLP in a tax-exempt account.

For investors who want MLP exposure in a tax-exempt account, it’s ideal to invest in an MLP exchange-traded note (ETN). ETNs are the unsecured debt obligations of an issuer, which agrees to pay a return on an index. The key advantage of ETNs is that they provide little to no tracking error. Because coupon payments from an ETN are taxed at ordinary income rates, ETNs are better suited for tax-exempt accounts.

However, investors should be aware of the drawbacks of ETNs. Relative to an exchange-traded fund (ETF) tracking the same index, the income from an ETN will be lower because the fee is taken out of the coupon. Additionally, ETNs expose investors to the credit risk of the issuing bank. Notably, MLP ETFs and ETNs will not generate UBTI in tax-exempt accounts.

MLP investing in taxable accounts

For an investor using a taxable account who does not mind K-1s – or related fees charged by his or her accountant – owning MLPs directly is the most tax-efficient way to gain exposure to this space. For investors who do not want a K-1 or do not want to select individual MLPs, investment products are available, including ETFs, that provide both diversified MLP exposure and a form 1099 at tax time.

There are two types of MLP ETFs – C-corp ETFs and RIC-compliant ETFs. Any fund – whether an ETF or mutual fund or closed-end fund – that owns more than 25% MLPs will be taxed as a corporation. Accordingly, C-corp ETFs predominantly own MLPs.

C-corp ETFs are best suited for investors seeking tax-advantaged income

The main advantage of C-corp ETFs is that they retain many of the tax advantages of their underlying holdings and provide a generous yield. Typically, a significant portion of the distributions from a C-corp ETF are considered a tax-deferred return of capital. Return of capital distributions reduce the investor’s basis in the ETF, and taxes are not paid on that portion of the distribution until the investor sells his or her position. Because C-corp ETFs are taxed as corporations, the performance of the ETF may lag the performance of its underlying holdings due to tax drag. C-corp ETFs are best suited for taxable investors that want to maximize tax-advantaged yield.

RIC-compliant ETFs are best suited for investors seeking total return

RIC-compliant ETFs cannot own more than 25% MLPs. This allows these funds to maintain their pass-through structure and avoid fund-level taxation. As a result, performance better tracks the underlying portfolio. Typically, RIC-compliant funds will own up to 25% MLPs, and the other 75% will consist of midstream corporations, utilities, energy companies, or other income-oriented equities. Investors should make sure the other 75% of the portfolio aligns with their objectives.

Because MLP exposure is limited, RIC-compliant funds typically have lower yields than C-corp funds, and the portion of tax-deferred income is lower. Given the lower yield but little tracking error, RIC-compliant funds tend to be best suited for total-return investors that want exposure beyond MLPs. Relative to a C-corp ETF, a RIC-compliant ETF is better suited to tax-advantaged accounts.

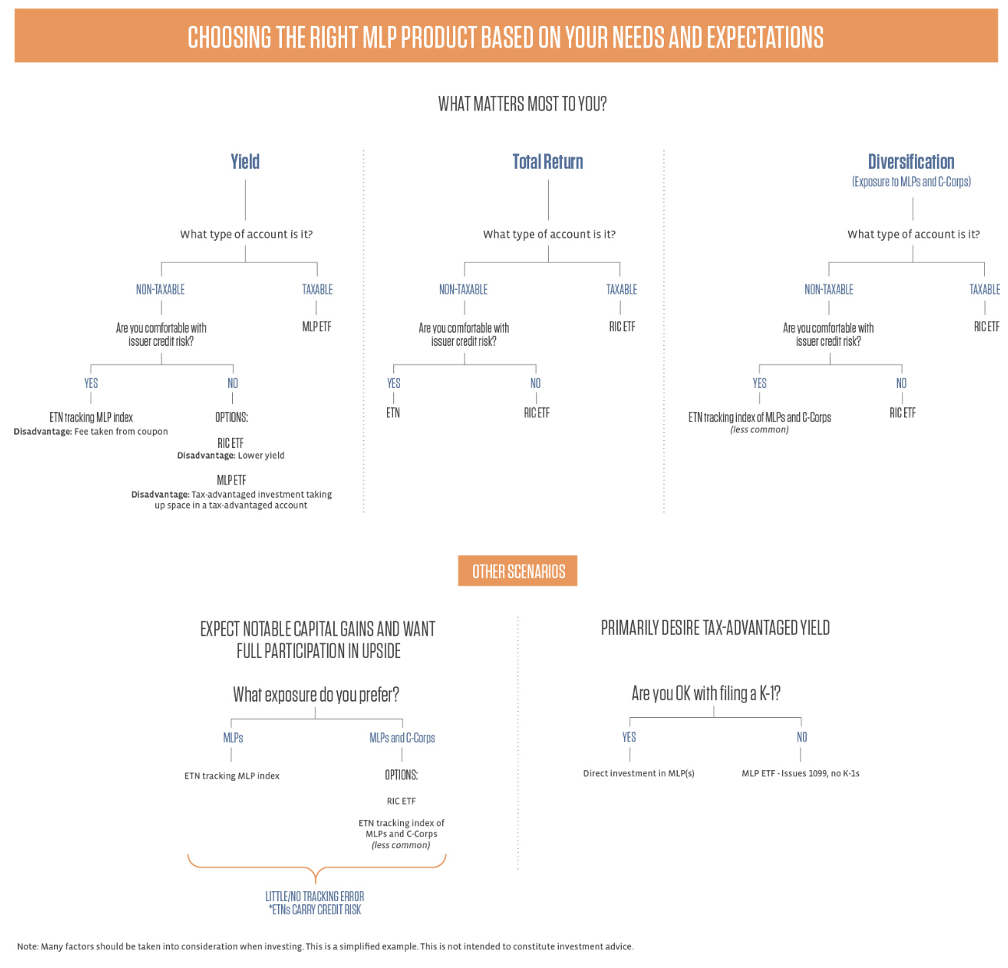

Map the pros and cons to pick the best MLP product for an investor’s needs

Understanding the pros and cons of different MLP product options is crucial to effectively allocating to this space and achieving the desired portfolio objective. The graphic below summarizes these considerations. With yield difficult to find and inflation a concern, the income and real-asset exposure provided by MLPs can enhance portfolios, but investors will want to make sure they are allocating to the space in a way that is optimal for their situation.

Source: Alerian

Stacey Morris, CFA is the director of research at Alerian, which equips investors to make informed decisions about master limited partnerships (MLPs). Alerian is not an investment advisor, and Alerian and its affiliates make no representations regarding the advisability of investing in any investment fund or other vehicle. This article should not be construed to provide investment, tax or legal advice.