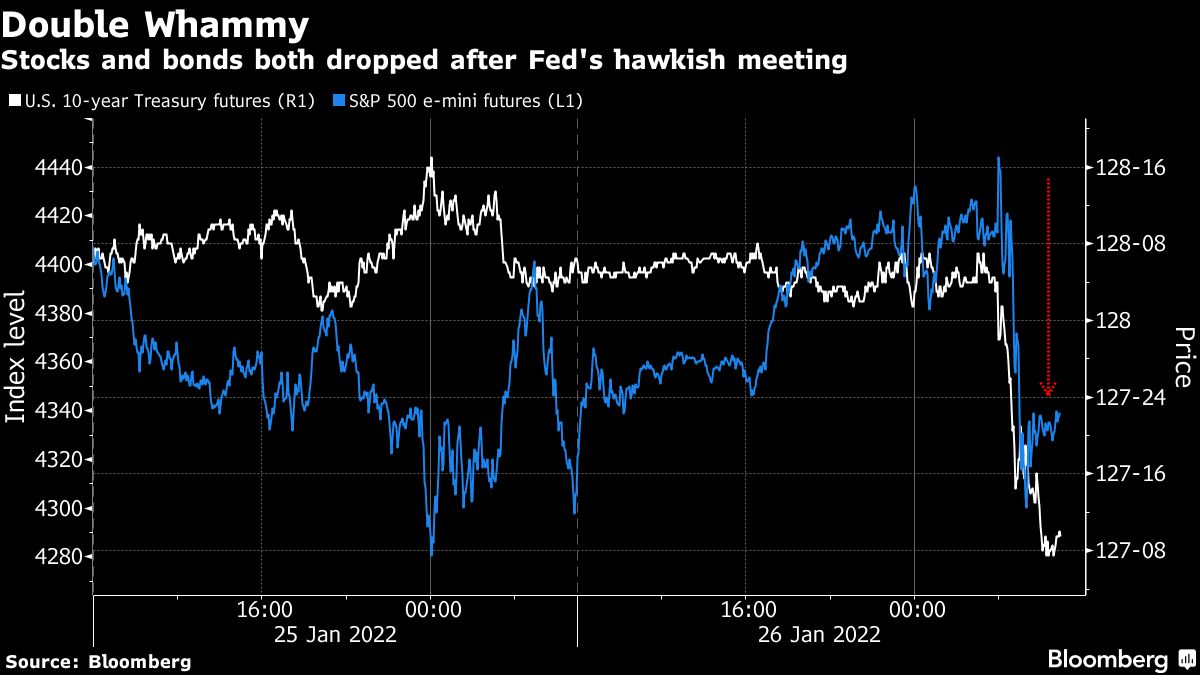

Strategists are mapping out their best trade ideas after Federal Reserve Chair Jerome Powell set the stage for raising interest rates to combat the highest inflation since 1982.

The hawkish comments are prompting investors to double down on their bet on value shares for this year, with Europe’s banking stocks surging on Thursday. The U.K.’s FTSE 100 index, which has a large exposure to value and cyclical shares, also gained, benefiting from the rotation out of expensive stocks and into cheaper markets.

Lenders, especially in Europe, are seen as the top winners from higher rates and bond yields. Some investors say they are also betting on emerging-market stocks and quality small-cap shares. Others are favoring the dollar and flatter yield curves, and plenty of traders see higher volatility as the new normal in stock markets, especially in high-priced tech shares. The Nasdaq futures erased losses of as much as 2.2% today, although Citigroup Inc. strategists said investors hold a record net short positioning in the tech-heavy index.

“Wishful thinking in the market was that the Fed would not sound more hawkish after the recent correction. This was not the case, in line with our view that more pain is needed before Fed put kicks in,” said Barclays Plc strategist Emmanuel Cau. “We stick to a preference for Value over Growth, and like China exposure. We think clients should focus on quality at reasonable price and avoid very expensive parts of the market.”

Here are selected comments on what’s next for global markets following the Fed:

Lower Strike Put

“The Fed’s latest update is net negative for risk assets, as it seems to show that the Fed has a lower strike put than we thought - in other words Powell would be comfortable to allow further market weakness and volatility without intervening,” said Altaf Kassam, EMEA head of investment strategy and research at State Street Global Advisors.

“Investors should continue to avoid developed markets government bonds as there is only downside there. We are rotating into defensive equities, long-dated U.S. Treasuries, commodities and VIX futures - Volatility will be here for a while.”

Focus on Profits

“Changing Fed expectations are exposing long duration assets with high valuations,” said Grace Peters, EMEA head of market strategy at JPMorgan Private Bank. “The types of companies that have suffered the most during this bout of weakness are ones that don’t have any profits now, but could have rapid growth and huge profits in the future.”

“Focusing on profitability should be increasingly valuable as interest rates continue to rise.”

Banks and Energy

“We still like value cyclical sectors particularly banks, energy and miners,” wrote Ankit Gheedia, head of European equity strategy at BNP Paribas. “Flatter curve means cyclicals underperform defensives so the risk is to expensive cyclical stocks.

“Fed’s hike for now means not much for earnings. Only thing is that earning season becomes even more relevant. Stocks that can deliver on growth to offset the impact of higher rates should still do well.”

Favor Value Shares

“We look for market interest rates and equities to stabilize on the Fed news,” said John Lynch, chief investment officer for Comerica Wealth Management. “Oversold conditions have been present in many respects, and we expect global cyclical recovery and gradually higher rates to be supportive of value, quality (profitable) small caps, and cyclical sectors including energy, financials, industrials and materials.”

“Inflation-adjusted (real) rates will likely remain negative in 2022, enabling equity investors to discount record profits, growing at slightly better than historically average rates, near historic lows. Profit growth in the range of 8.0% to 10.0% should guide the S&P 500’s march toward our fair value estimate of 5,000 for the index by year end.”

On the Defense

“We think the rotation into value stocks has for the most part run its course,” said Mathieu Racheter, head of equity strategy research at Julius Baer. “Future outperformance by value stocks are now much more dependent on the growth and interest rate outlook. With the latest developments, we think defensive names looks increasingly attractive. We also continue to like financials, especially banks, as a play on higher yields.”

Seek Shelter in Asia

“The better monetary backdrop in Asia could overall support Asian equities” even as the expensive loss-making growth stocks will remain “vulnerable as their valuations could be hit by higher rates,” Jian Shi Cortesi, a portfolio manager at GAM Investment Management in Zurich said in emailed comments. “The inflation pressure is lower in many Asia markets, and interest rate will not need to be hiked as much as in the U.S.”

Asia is the best place to invest in global equities given value styles are doing well, China is starting to turn around due to a policy pivot, and the dollar isn’t strengthening like last year, Mixo Das, a strategist at JPMorgan Chase & Co said in a television interview on Bloomberg. “Within Asia, if you just follow policy, China is definitely the place to be.”

Higher Yields, Flatter Curves

“Today’s Fed meeting reinforces our bias for higher U.S. yields, a flatter curve and stronger U.S. dollar. The statement and particularly Powell’s presser were quite hawkish: opening the door to 50-bp hikes and possibly hiking at every meeting,” Wells Fargo strategists including Mike Schumacher wrote in a note. “Given today’s hawkish surprise from the Fed, more curve flattening and USD strength seems in store in the near term.”

“Fed funds futures price 31bps for March. Fade it. In our opinion, this is too much tightening, too soon. Instead, position for the market to price more tightening through May.”

Dollar Bullish

“Rising Treasury yields make it hard to find an excuse to look anywhere but the dollar in FX markets,” said Simon Harvey, head of FX analysis at Monex Europe. “Despite being fairly noncommittal for the remainder of the press conference with regards to the timing, pace and impact of quantitative tightening, the damage has already been done in financial markets due to the commentary suggesting a steeper rate path relative to that of four rate hikes this year prior to the meeting in what was meant to be one of the plainer sailing Fed meetings.”

Brace for Volatility

“The stock market is especially vulnerable to higher rates and the removal of the tailwind that the Fed’s asset purchases have provided for the past two years,” Chris Zaccarelli, chief investment officer for Independent Advisor Alliance wrote in a note. “We believe the economy will stay out of recession and the bull market in stocks will continue this year, but we are concerned that the volatility we have already witnessed this month will increase in the months ahead and would exercises caution in the near term.”

Bet on Seven

“The January FOMC meeting reinforces our view that the Fed will likely need to hike more than the market is currently pricing,” wrote Ethan Harris, head of global economics at Bank of America Global Research. “This should push rates higher across the U.S. rates curve & in a bear flattening bias.”

“We still think the market will likely price six to seven hikes this year and encourage clients to position as such. We also expect the market will continue challenging the Fed towards a 50 basis point hike in March. If the market prices a 50 basis point hike in March we expect the Fed will follow it given their current ‘humble’ and ‘nimble’ approach to setting policy.”

China Haven

“I still see some room for China govenrment bonds to outperform given its haven asset quality,” said Peiqian Liu, economist at Natwest Markets. “In the very short term we may see CGB yields rebound as a knee-jerk reaction, but as the PBoC continues to ease monetary policy, bond yields will still trend lower in coming months. We think China will still face some capital outflow pressures as the yield differential with the US narrows, but the yuan will likely be more resilient in this round of Fed tightening as it has been well supported by strong trade surplus.”

Buy Emerging Markets

“Emerging-markets can still outperform especially with the backdrop of the commodities boom,” said Mark Galasiewski, chief Asia-Pacific analyst at Elliott Wave International. “I personally don’t consider 2% interest rates to be high, the boom will continue for a long time and EMs are going to be growing in this period. I like the AFK ETF, I like South East Asia and LatAm, I like Thai and Indonesia exporters.”

“This likely additional sell-off in Treasuries might well be combined with spreads tightening in EM,” said Jean-Charles Sambor, head of emerging markets fixed income at BNP Paribas Asset Management in London. “The world is gradually becoming a better place and EM high yield spreads are very cheap. We continue to have a contrarian view and think 2022 is gonna be the year of Asia HY spreads normalization.”

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.