Don’t be fooled by the Commerce Department report Thursday showing the U.S. economy grew at a faster-than-expected annualized rate of 6.9% in the fourth quarter. Look under the hood of the gross domestic product report and it’s clear that there’s a big inventory cycle unfolding in the economy as consumer demand wanes following a large buildup in the supply of goods. So now, the negative economic consequences of unloading unwanted inventories are about to begin.

Spurred by warnings of potential shortages during the holiday season, retail sales jumped an unusually large 1.8% in October from September. Stores rushed to secure goods, with the combined inventories of Walmart Inc. and Target Corp. surging to $72.4 billion in the quarter ending Oct. 31 from $64.6 billion a year earlier. Nevertheless, consumers finished most of their buying by Thanksgiving. Shoppers in stores and online between Black Friday and Cyber Monday totaled 180 million, according to the National Retail Federation, down from 186.4 million in 2020, which was below the pre-pandemic 189.6 million in 2019.

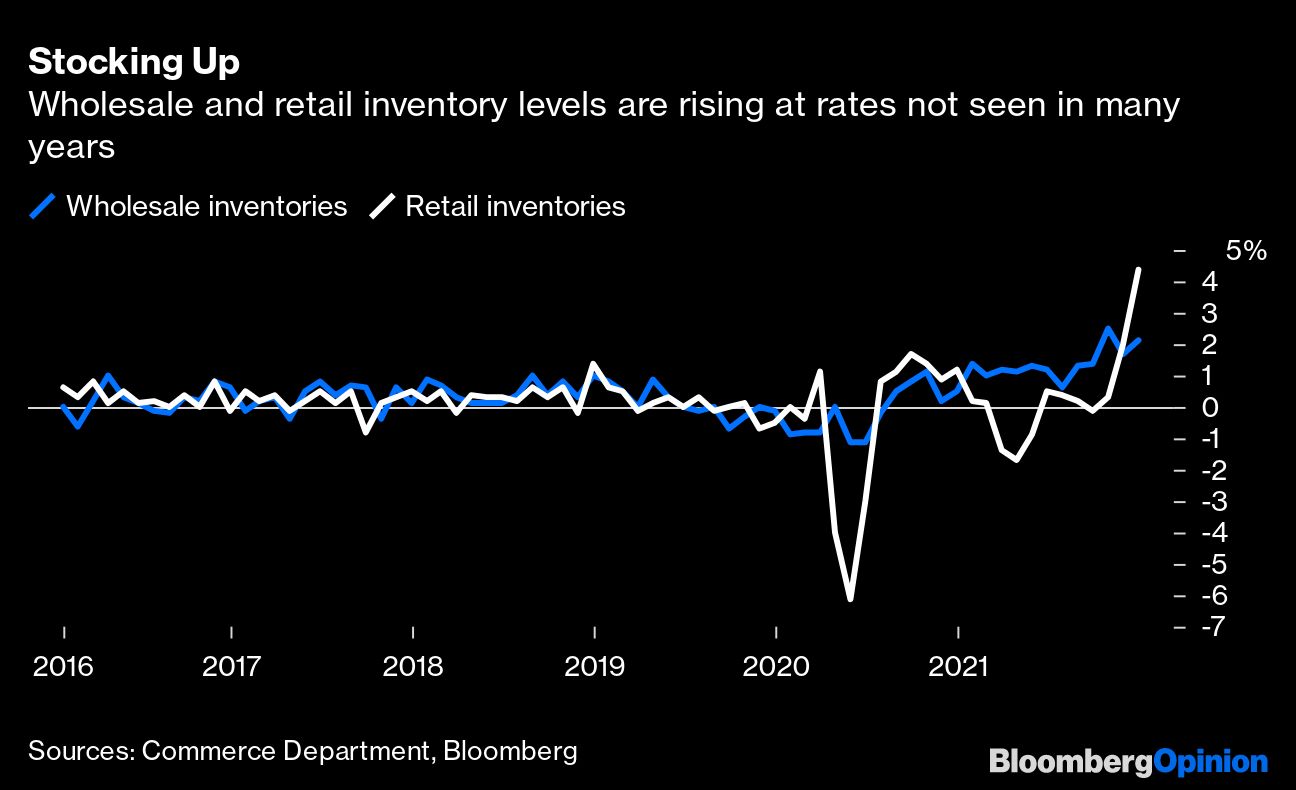

Total retail sales rose only 0.2% in November, below the 0.8% rise in the consumer price index, which means real spending fell by 0.6%. Then came December, with total retail sales plunging 1.9% from November, or 2.4% adjusted for inflation. So it’s no surprise that inventories are bloated. Wholesale inventories climbed 2.1% in December from November and jumped 18.3% from a year earlier. Those excess goods hadn’t yet passed through to retailers, but their inventories already rose 4.4% in December from November.

The building of inventories has been the mainstay of economic growth. In the third quarter of 2021, it accounted for 2.2 percentage points of the 2.3% annualized increase in real GDP from the second quarter. So the rest of the economy rose at just a 0.1% annual rate. In the fourth quarter, the jump in inventories equaled 4.9 percentage points of the 6.9% annualized rate of growth. Without the inventory-building, the economy grew at only a 2.0% annual rate. That’s equal to my forecast of maximum U.S. growth this year but just half the International Monetary Fund’s forecast of 4%.

Getting rid of those excess inventories will have negative effects on the economy that are mirror images of the positive effects of building them. So be prepared for declines in economic activity in coming quarters. Meanwhile, those container ships full of goods from Asia that are moored off the ports of Long Beach and Los Angeles will get unloaded and the goods moved inland. The Maritime Exchange of Southern California and the Pacific Merchant Shipping Association report that the number of idling ships in mid-December was 101, up from nine in mid-June.

Economic weakness will also come from the likely deflation of the single-family housing bubble. Demand for single-family abodes has been driven by cheap and available mortgage money, the pandemic-driven payments that households received in April 2020, January 2021 and March 2021 and by the flight from cramped city apartments to single-family houses in suburban and rural locations.

But the Federal Reserve will be raising interest rates as soon as March and 30-year fixed mortgage rates have already climbed from 2.8% in February 2021 to 3.7% in anticipation. Barring a recession, no further stimulus payments to households are likely as President Joe Biden’s Build Back Better legislation flounders amidst pre-November election political maneuvering in Washington. The stampede to the suburbs appears to have peaked and some, especially Millennials, are returning to city apartments. The University of Michigan’s survey of consumer buying conditions for houses has tumbled from a 140 index reading in 2020 to 83 recently.

On the supply side, homebuilders’ confidence is leaping. The National Association of Home Builders’ Market Index has jumped from 10 in 2009 to 83. Numbers above 50 indicate favorable conditions. And the months’ supply of new houses has risen from 3.5 in October 2020 to 6.5.

Despite these signs of a weakening economy, the Fed is embarking on a credit-tightening binge. It not only plans to raise rates, but also end its purchases of U.S. Treasury and mortgage-backed securities in March. The central bank is also considering reductions in its almost $9 trillion of assets sitting on its balance sheet. The Fed believes that labor markets are strong enough to withstand its plans to curb inflation.

Policymakers never plan to tighten credit to the point that a recession unfolds, but in the last 14 instances, 13 led to business downturns. The only soft landing came in the early 1990s. The coming tightening will probably make it 14 out of 15.

My forecast is obviously negative for stocks, especially those caught up in a speculative fever as well as growth stocks and other equities whose current prices are only justified by robust future earnings at low discounting rates. If a recession unfolds, it will be helpful to the dollar and Treasury bonds, which would benefit from their safe-haven status, declining credit demand and the later shift by the Fed from credit restraint to ease after it realizes that, once again, it has killed the economic expansion.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Gary Shilling