Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Interest rate manipulation has been achieved through massive money printing that is causing inflation. To control inflation, bond manipulation must stop. When the manipulation ends, bond prices will plummet, and stock prices will follow.

The Federal Reserve has been manipulating interest rates for 13 years since 2009. Investors have become accustomed to negative real yields in their bond investments, which yield 1% when inflation is 7%.

In theory, investors are not supposed to invest in assets with known real losses. But other central banks are manipulating their bond prices, so the usual alternatives are not viable. The manipulation is causing inflation because it requires money printing to buoy bond prices – the Fed overpays in order to keep prices high and yields low.

Now attention is being redirected from price manipulation to fighting inflation.

A pretend fight – think professional wrestling

Cowboy wisdom advises, “When you find yourself in a hole, you need to stop digging.” So it is with bond price manipulation driven by quantitative easing (QE) and zero-interest rate policy (ZIRP). The Fed is causing inflation, and it needs to stop.

But the Fed isn’t coming to the rescue to control inflation. It’s backing off of the major cause for inflation, namely the printing of $13 trillion, which is more than our 10 most expensive wars combined.

The end of ZIRP brings an end to bubbles in stock and bond markets. Importantly, bond yields should return to their natural, unmanipulated, levels.

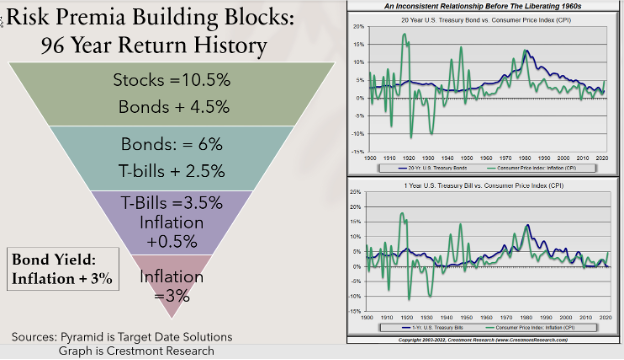

Unmanipulated bond yields

In normal, unmanipulated situations, investors price assets to be compensated for the risk they take with what is called a “risk premium.” History provides a clue to what these premiums should be, as shown in the following:

Bond yields should be inflation plus 3%, so 5% in a 2% inflation environment or 10% in the current 7% environment.

The impact of rising interest rates on bond prices

Bond durations average 6, so each 1% increase in bond yield drives down prices by 6%, or 6 times that increase. A 4% increase to 5% causes a 24% loss in bond prices. A 9% increase to 10% causes a 54% loss.

The Fed will taper over a prolonged period of time, gradually reducing its manipulation, and the Fed could jump back in as it did in 2018 if markets decline too rapidly. But jumping back in will rekindle inflation. The Fed is left with no good options.

Conclusion

The Fed needs and wants to be in control, but it is not. Quite the contrary, unprecedented money printing is causing inflation that will accelerate if the Fed does not stop its printing. It has announced that it will taper bond purchases and increase interest rates. The part about increasing interest rates will happen naturally when the taper starts.

No one knows what the consequence of QE and money printing will ultimately be, but it can’t be pretty. Investors should not rely on Fed speak. Rather, they need to protect against imminent market crashes and runaway inflation. Yes, this is a warning.

Recent stock market volatility, with markets swinging more than 2% up and down every day, revealed that investors – both bulls and bears – are on the brink of panic.

Ron Surz is CEO of Target Date Solutions, Age Sage, and GlidePath Wealth Management, and co-host of the Baby Boomer Investing Show that you can binge watch on Patreon. He authored the Book Baby Boomer Investing in the Perilous Decade of the 2020s.

Please watch and support our Baby Boomer Investing Show and visit our Baby Boomer Libraries, our Target Date Fund blog, and our GlidePath blog

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.