Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Those nearing or in retirement are worried about what higher-than-expected inflation will mean. Here are a few things to consider to temper their anxiety.

Inflation doesn’t affect everyone in the same way

Inflation does its worst damage when household income is derived in large part from sources that are not adjusted for it. For example, if one has a pension or annuity that does not enjoy periodic cost-of-living adjustments, long-term high inflation will eat into purchasing power significantly. A $1,000/month pension that is not adjusted for inflation would buy just $539-worth of goods in 10 years if inflation averaged 6% throughout that decade.

However, Social Security, an income source that is adjusted annually for inflation, is foundational for today’s retirees. Benefits went up 5.9% in 2022, roughly in line with recent inflation trends. If Social Security provides a large part of a retiree’s income, these adjustments can go a long way toward counteracting the effects of inflation.

Furthermore, research shows that retirees tend to reduce their spending as they age. Though these spending patterns vary, a 1-2% reduction in annual inflation-adjusted spending is common. This natural slow-down in spending provides retirees with a useful cushion to rising prices.

Inflation may not affect as many retirees and as much as one might think. Individual situations will vary, of course, so staying alert is key if inflation remains elevated for many years.

Short-term inflation is a poor predictor of retirement experience

Along with Social Security, many retirees depend on withdrawals from investment accounts. While some might worry that, because of rising inflation, retirees will need to reduce spending and take less from their investment portfolios, such a quick reaction is premature. Historically, the year-over-year inflation rate has had zero predictive value with respect to the portfolio withdrawals an individual could have sustained over a multi-decade retirement.

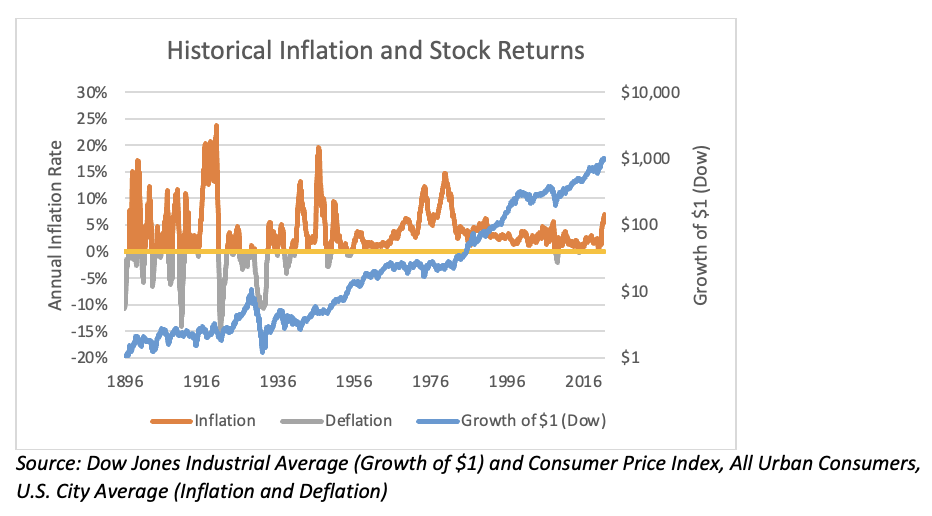

It’s not hard to find historical examples with every mix of inflation rate and achievable retirement withdrawal rate, but it is particularly easy to find examples of high inflation and high withdrawals. The last time the U.S. saw three or more months with inflation at or above 6% was the fourth quarter of 1990. Because of the high investment returns they would have experienced through the 1990s, those who began a 30-year retirement at that point could have withdrawn over $80,000/year, in today’s dollars, from a $1 million portfolio invested 60/40 in stocks and bonds. That’s among the highest possible withdrawal rates in the last 150 years. The U.S. experienced brief periods of high inflation in 1941-1943, 1946-1948 and 1951, but those who retired in those years would have been able to sustain portfolio withdrawals well above average.

If the current bout of inflation is short-lived, history says that it won’t harm retirees permanently.

Prolonged inflation and sideways markets – The worst combination

The worst historical situations for retirement income are found during prolonged periods of low inflation-adjusted returns. The years from 1963 to 1969 serve as the poster child for those prolonged poor sequences of returns. Inflation during this period ranged from 1.0% to 5.9% and averaged just 2.9% – fairly low, from a historical perspective. However, a period of prolonged high inflation did come in the next decade, from 1973-1982.

Though those retiring in the mid-1960s would not have known what the future held in store, the subsequent period of high inflation was enough to help flatten inflation-adjusted market returns for many years. For those who depend on portfolio withdrawals, periods of sideways returns are like wars of attrition against retirement income. They aren’t spectacular news items like a market crash. They take longer to play out – but have more long-term bite.

Fast and deep market losses on their own would typically not have impaired retirement income (if retirees resisted the temptation to sell and lock in losses). Following the 1929 market crash, deflation (a decrease in prices) cushioned the blow for a hypothetical retiree. In 1947, a spectacular spike in inflation to 20% was accompanied by a flat market, but those conditions didn’t last long. Those situations were exceptional, but they weren’t as harmful as the prolonged poor returns and inflation in the 1960s and 1970s.

Nobody knows whether current heightened inflation will last long or be paired with sideways markets. Because it is usually not prudent to take evasive action until there is something to evade, retirees will need to monitor returns and economic conditions patiently to know whether they need to adjust to keep their retirement income on track.

Justin Fitzpatrick, PhD, CFA, CFP; co-founder and chief innovation officer of Denver-based Income Lab, a provider of retirement income planning software for advisors.

Read more articles by Justin Fitzpatrick

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.