The S&P 500 Index officially fell into a correction on Tuesday, tumbling 10% from its record high on Jan. 3. The benchmark for U.S. stocks extended its decline on Wednesday, dropping as much as 1.8%. The word “correction” implies something was “wrong” with stocks. It’s true that the outlook for equities has dimmed with inflation raging, the Federal Reserve preparing to tighten monetary policy, fiscal stimulus having ended, oil flirting with $100 a barrel and global geopolitical tensions worsening between the U.S. and Russia over Ukraine. But none of that means the next stop is a bear market, defined by a 20% plunge from the last record high.

The first thing to know about corrections is that they are common. There have been 33 of them since 1950 for the S&P 500, and it has been almost two years since the last one, according to LPL Financial. Historically, corrections have been a good time to buy, with equities rising about 90% of the time over each of the following 12 and 24 months, LPL found. Returns averaged 24.8% one year after a bear market and 37.4% two years later.

There’s no guarantee history will repeat, but it’s notable that the weakness in equities comes amid some strong fundamental performance for companies. With earnings season wrapping up, 78% of the S&P 500’s members beat Wall Street’s revenue estimates for the fourth quarter, above the 68% average over the past five years, according to DataTrek Research. Earnings beat estimates by 8.5%, in line with the five-year average of 8.6%. At 12.5%, profit margins were better than pre-pandemic averages of 10% to 11%, the firm said.

As for the outlook, DataTrek finds that analysts are generally cautious for this quarter, expecting earnings per share of $51.85 for the S&P 500, lower than the record $55.16 for the final three months of 2021. But further out, earnings are forecast to rebound strongly, to $55.44 a share for the second quarter, $58.39 in the third and $59.72 in the fourth. Of course, it’s only February and a lot could go wrong between now and the end of the year, but the S&P 500 price-earnings ratio has moved back below 20 for the first time since before the pandemic.

Here’s the thing about analysts’ estimates: All through the pandemic they have been unduly cautious, underestimating the earnings power of corporate America. And there’s no reason to believe that they have changed their ways. This makes it more likely that upside surprises to earnings are likely to continue, but it will take some time for investors to believe that. “We’d take the over on what analysts are looking for in Q1 or Q2, but this year’s dreadful market action says it’s too early to lean on that belief,” Nicholas Colas, the co-founder of DataTrek, wrote in a research note to clients.

It’s also notable that Wall Street strategists, who are usually the first to buckle when things go against them, have been hesitant to cut their S&P 500 year-end estimates. The latest monthly survey by Bloomberg News for February shows that the median year-end estimate is 5,000, little changed from the 5,040 forecast in January and 5,000 in December.

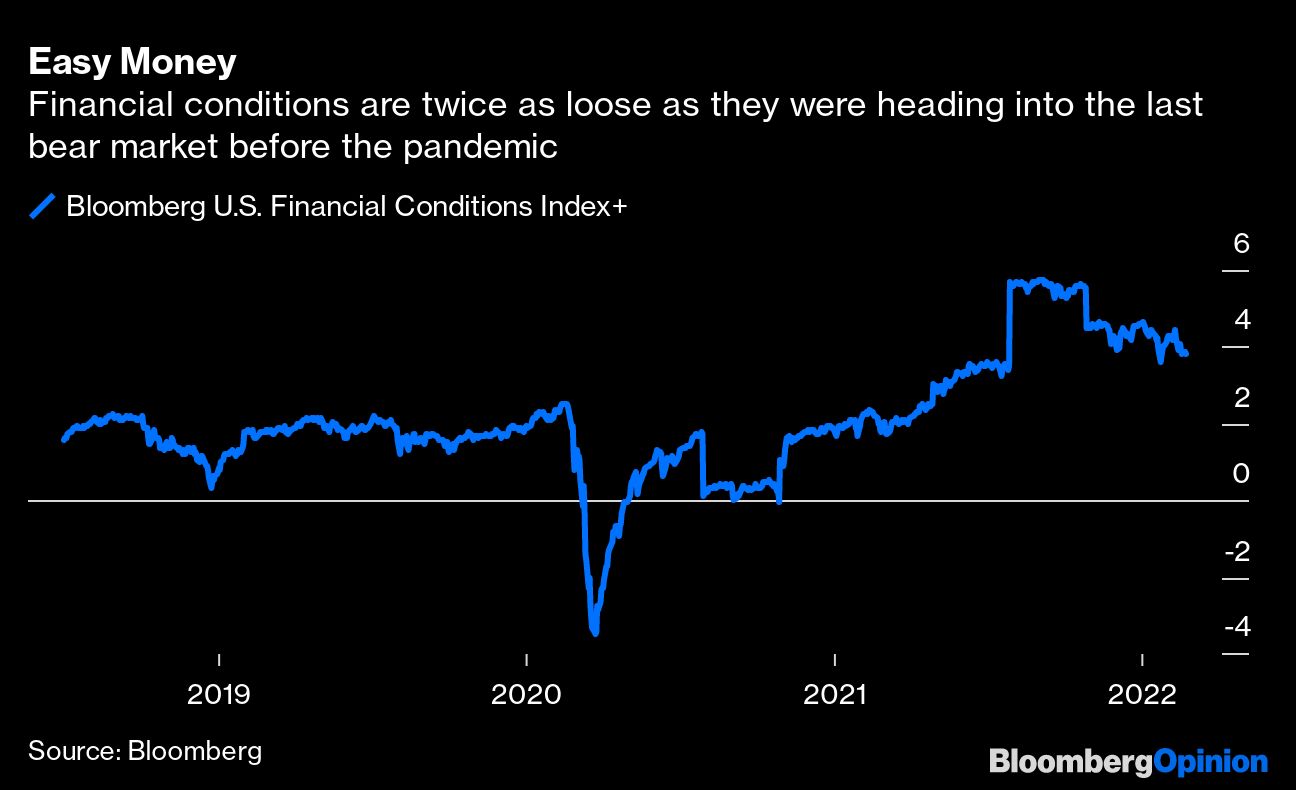

One worrying sign would be if financial conditions were tight, but they’re not. The Bloomberg U.S. Financial Conditions Index+ is about double where it was entering the last bear market before the pandemic, which extended over the fourth quarter of 2018. It’s also encouraging that on the day after stocks entered a bear market the market for high-yield bonds was beginning to revive in a positive sign for risk appetite. In a sampling of offerings, social media company Twitter Inc. was seeking to raise $1 billion in the debt markets, and BellRing Brands, a protein-shake maker, began marketing $840 million of notes, according to Bloomberg News.

Given the run that stocks have had, more than doubling from the pandemic-era low in March 2020 to early in January, you can’t fault investors for selling first and asking questions later. But this correction should be welcomed because it shows that after a prolonged period when it seemed stocks only rose, investors are no longer on the same side, which is a healthy sign. Plus, as the LPL data show, corrections are nothing to fear.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Robert Burgess