Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Headline inflation has jumped to its highest level since 1982 and has gutted realized one-year returns in major assets classes. If higher inflation persists, at least two mechanisms represent an ongoing risk to achieving expected real portfolio returns: Inflation will erode nominal returns and it will inflict a tax drag on assets.

Nominal versus real returns

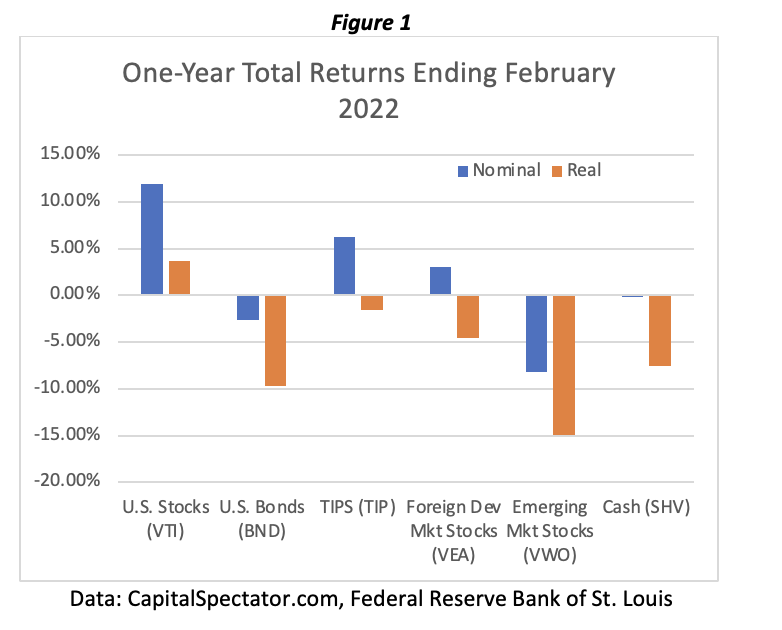

Capital Spectator compiles returns for representative ETFs; through February, inflation cut the one-year return of U.S. stocks by two thirds, bonds lost 9.7% of their value in real terms, and cash is worth 7.5% less than a year earlier (Figure 1).

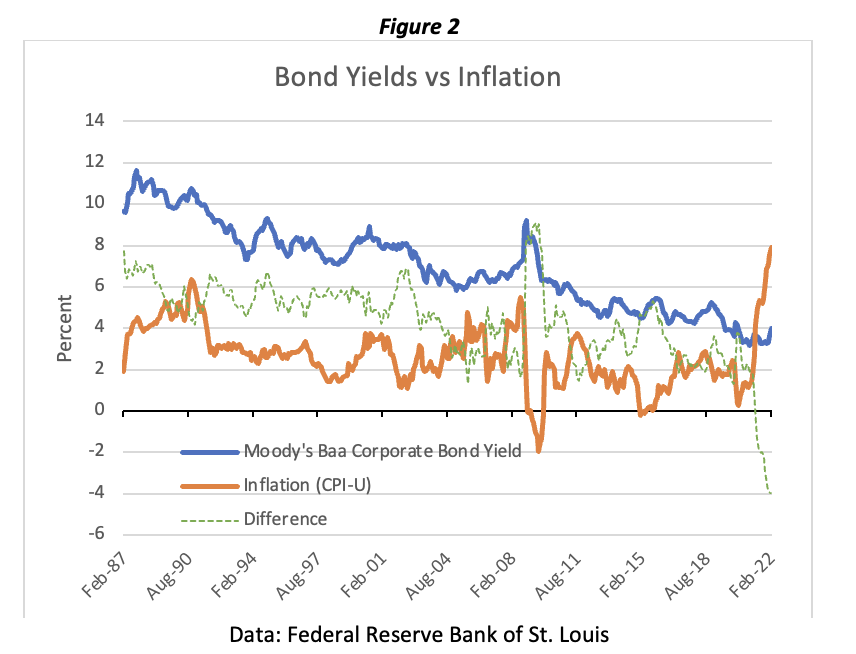

Planning is often based on expected real returns. Inflation is included as a static or mildly varying assumption. The theory is that persistent inflation will be reflected in nominal returns. One look at bond yields, which represent expected returns, reveals that this is not the case today (Figure 2).

Planning is often based on expected real returns. Inflation is included as a static or mildly varying assumption. The theory is that persistent inflation will be reflected in nominal returns. One look at bond yields, which represent expected returns, reveals that this is not the case today (Figure 2).

The damage to cash and bond positions from the recent spike in inflation has been done. The loss of purchasing power will take years to make up even if yields increase to reflect higher inflation in the future.

The inflation tax drag

Suppose the relationship between real and nominal returns recovers and remains perfectly stable. Even then higher inflation will eat into real returns.

Here is an extreme example. Assume $10,000 is invested earning a real return of 5% with no inflation and a 15% tax rate. After one year, the value is $10,500, or $10,425 after tax. The after-tax real return is 4.25%

Now assume the real return is still 5% but inflation is 50%. The portfolio increases to $15,750 or $14,887.50 after tax. The after-tax real return is minus 0.75%

Why is this? Because in dollars the inflation tax bill exceeds the real return.

What if we can defer paying tax and let those dollars compound? After 10 years, the real after-tax annual return is still minus 0.75%. But if tax is collected at the end instead, the real after-tax return is 4.38%.

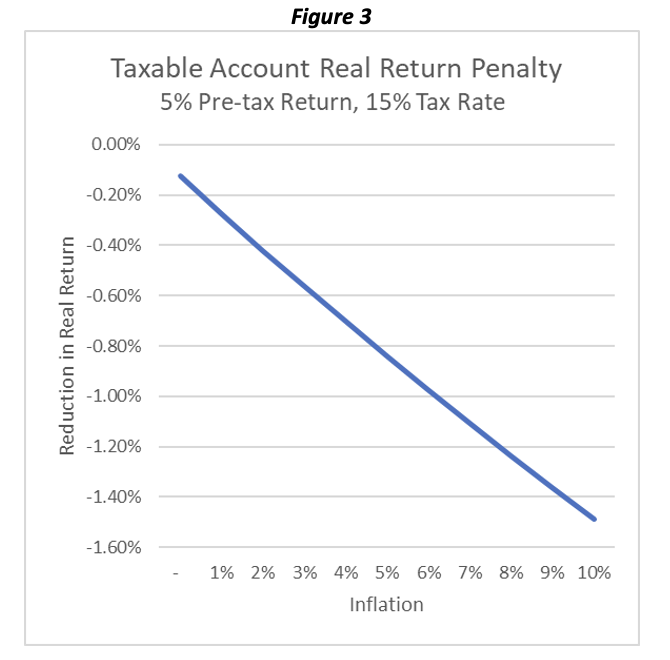

We’re obviously not at 50% inflation, but even at the current 8% rate the bite that the tax on inflation could take out of real returns is meaningful. Figure 3 shows the difference in real return over 10 years between a taxable investment and a tax-deferred investment at different levels of inflation. In each case, the pre-tax real return is 5% and tax rate is 15%, taxed either annually or at the end.

In a 1%-2% inflation environment, the tax penalty is present, but relatively modest. But an increase to 8% inflation reduces the after-tax real rate of return by 1%. Twenty percent of the real dollar return is lost to the inflation tax. Higher tax rates further increase the penalty.

Implications

The spike in inflation vividly illustrates the risk of holding cash. Cash is not a “risk-free” asset. As economist John Cochrane and others have pointed out, for long-term investors the risk-free asset is an inflation-indexed perpetuity. Framing risk as the likelihood of achieving a certain consumption stream can be helpful in a high-inflation environment.

More subtly, protecting real returns against the inflation tax has implications for tax planning and asset location, including:

- It increases the economic benefit of all tax-deferred accounts.

- It makes after-tax contributions to retirement accounts more attractive.

- It’s important to the Roth versus traditional decision (see previous article here).

- It increases the value of other tax-deferred investments, including annuities.

- It supports holding TIPS, especially in tax-deferred accounts to avoid annual taxation of the inflation adjustment.

Peter Hofmann, CFA, is with Fieldmark Advisors, a registered investment advisor based in North Salem, N.Y.

Planning is often based on expected real returns. Inflation is included as a static or mildly varying assumption. The theory is that persistent inflation will be reflected in nominal returns. One look at bond yields, which represent expected returns, reveals that this is not the case today (Figure 2).

Planning is often based on expected real returns. Inflation is included as a static or mildly varying assumption. The theory is that persistent inflation will be reflected in nominal returns. One look at bond yields, which represent expected returns, reveals that this is not the case today (Figure 2). The damage to cash and bond positions from the recent spike in inflation has been done. The loss of purchasing power will take years to make up even if yields increase to reflect higher inflation in the future.

The damage to cash and bond positions from the recent spike in inflation has been done. The loss of purchasing power will take years to make up even if yields increase to reflect higher inflation in the future. In a 1%-2% inflation environment, the tax penalty is present, but relatively modest. But an increase to 8% inflation reduces the after-tax real rate of return by 1%. Twenty percent of the real dollar return is lost to the inflation tax. Higher tax rates further increase the penalty.

In a 1%-2% inflation environment, the tax penalty is present, but relatively modest. But an increase to 8% inflation reduces the after-tax real rate of return by 1%. Twenty percent of the real dollar return is lost to the inflation tax. Higher tax rates further increase the penalty.