If you’re looking for a case-study in economic groupthink, try Googling the phrase “Fed behind the curve.” Informed opinion, it seems, has congealed behind a conventional wisdom that the U.S. Federal Reserve has been too slow to restrain accelerating inflation.

Such widespread confidence would seem to require unambiguous evidence. But where is it?

At least one eminent economist thinks the statistical case against the Fed is shaky. That would be Brad DeLong, the historian, professor of economics at the University of California at Berkeley and former deputy assistant Treasury secretary under President Bill Clinton.

In a critique last week of the conventional inflation wisdom after the Fed raised a key interest rate by a quarter of a percentage point, DeLong asked rhetorically: “So why is the conclusion not: ‘Policy is appropriate. The Fed is not behind the curve’?” He added, “This is, to me, a very genuine mystery.”

DeLong has also challenged the certainty that historical experience supports the prevailing conclusion. So has Paul Krugman, the economics Nobelist and New York Times columnist. Their argument deserves closer attention.

On March 16, the Fed lifted its target for the federal funds rate, or cost of overnight lending of reserves between commercial banks, for the first time in two years. The increase of 0.25 percentage point brought the rate to 0.5% as inflation, measured by the U.S. Personal Consumption Expenditure Core Price Index, continued climbing after hitting a 21st-century high of 5.2%, according to data compiled by Bloomberg.

Fed Chair Jerome Powell, who subsequently presaged another half-point increase, routinely explains central bank thinking as “data dependent,” by which he means that “policy is never on a preset course and will change as appropriate in response to incoming information.” That's what he told the National Association for Business Economics in October 2019.

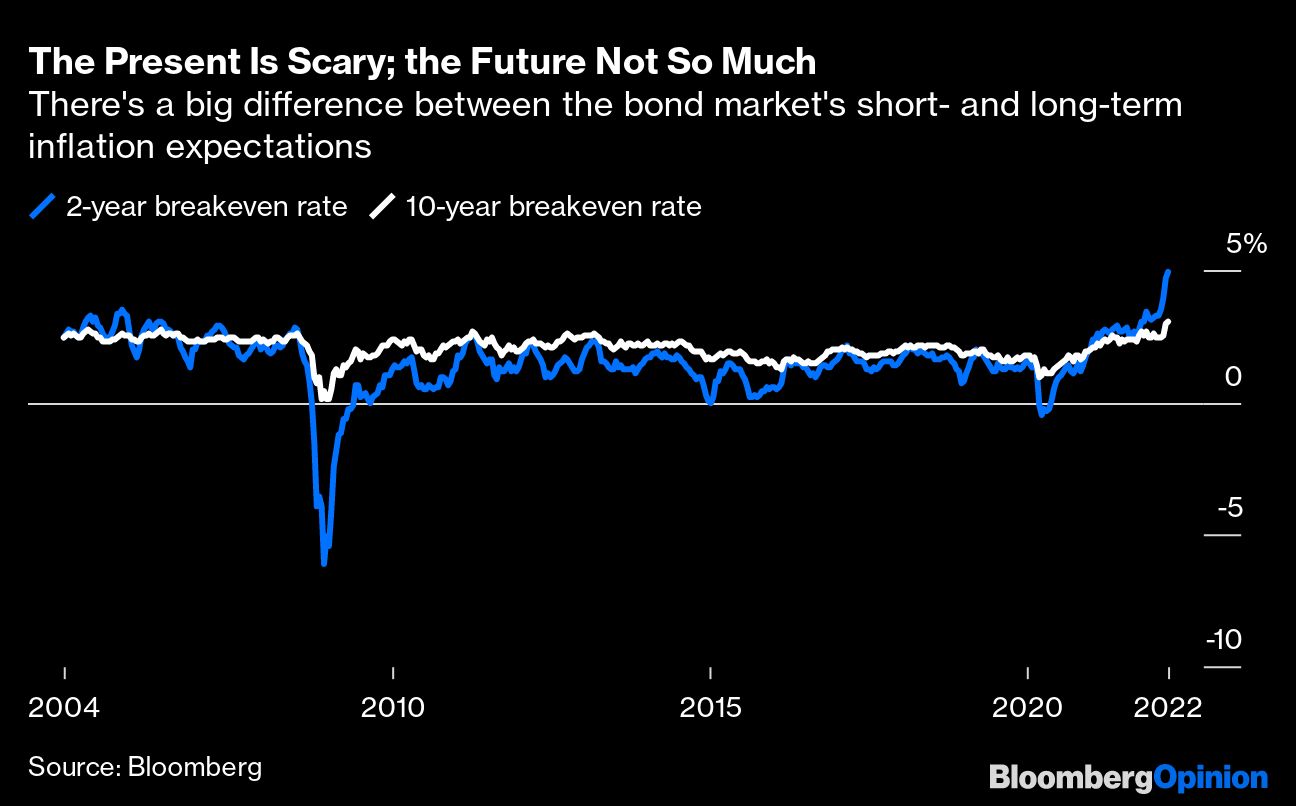

Much of that information is in the $30 trillion U.S. bond market, where the 30-year breakeven rate — the bet on what average annual inflation will be during the next 30 years — is 2.6%, or 0.5 percentage point less than the 21st-century high, according to data compiled by Bloomberg. Similarly, the 5-year-forward breakeven rate fell to 2.3% from 2.6% a year ago and is a full percentage point lower than the 2008 high.

In other words, the people who buy and sell Treasury securities around the world don't anticipate accelerating inflation in the long run. They're betting fortunes and reputations on the conviction that inflation will surge during the next two years and then abate precipitously at some point over the next eight years, reflected in the spread between the 2-year and 10-year breakeven rates.

Yet dozens of luminaries, including DoubleLine Capital co-founder Jeffrey Gundlach, Stanford University economics professor John Taylor and former Dallas Fed President Richard Fisher share the belief articulated by former Treasury Secretary Larry Summers that “the Fed has allowed itself to get far further behind the curve.”

DeLong thinks the bond-market participants are the better inflation barometer.

“Maybe there is an argument,” he wrote, that millions of people in the bond market “are weirdos who are disconnected from the inflation expectations embedded in the actors in the economy” whose “beliefs and expectations really matter because they drive decisions. Maybe there is an argument that we need to fear not bond market vigilantes, but rather other actors and agents, whose expectations of inflation have become substantially de-anchored and who are already taking steps that will produce a persistent inertial inflationary spiral.”

Those declaring that the Fed is behind the curve lobbed the same criticism at the European Central Bank after a record increase last year in the Euro area price index. They’re unmoved by the assurances of ECB President Christine Lagarde, who said last month, “In all scenarios, inflation is still expected to decrease progressively and settle at levels around our 2% inflation target in 2024.”

If central banks have actually lost control of the tools they use to stabilize economies, one might expect financial conditions to be roiled. That's not happening, even with the economic and market disruption caused by Russia's invasion of Ukraine and the ensuing global sanctions against President Vladimir Putin's war. The Bloomberg U.S. Financial Conditions Index, which quantifies the stresses facing the financial system by measuring the liquidity of money markets and the performance of bonds and stocks as well as their volatility, declined a modest two index points from its perch a year ago and still is only 0.5 point below the 30-year average. The higher the index, the less stressed the system will be.

Many of the Fed's detractors, led by Olivier Blanchard, former chief economist of the International Monetary Fund and a senior fellow at the Peterson Institute for International Economics, say the Fed should be studying the 15-percentage-point increase in interest rates between 1975 and 1981 for policy guidance now.

To which DeLong asks: “Why is the rate increase from 1975-1981 relevant? We have a target: inflation from five to 10 years out. We have an instrument: the current level and planned forward path for the Fed funds rate. We have a reading on whether we are on a glide path to target — the bond market's five-year, five-year-forward expected inflation rate. The reading says we are.”

He concluded with a rhetorical question: “Is there a better reading available as to whether we are on the glide path? If so, what is it?”

It’s not just a theoretical matter. If the Fed ignores bond market indicators and drives interest rates to unprecedented levels, as Blanchard recommends, recession is more likely to follow. If the 2008 financial crisis and ensuing Great Recession proved anything, DeLong wrote, “Errors in not raising interest rates quickly enough are errors from which we can recover,” but over-aggressive increases when rates are as low as they are today would be “errors from which we cannot reasonably recover.”

The better scenario is for the Fed to raise interest rates when market and financial conditions actually demonstrate that it truly is behind the curve. At that point, the Fed can announce a change in policy to shape expectations.

“But why,” DeLong wisely asks, “is today that day?”

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Matthew A. Winkler