On Tuesday, the day that government-reported inflation hit 8.5%, Jeffrey Gundlach said it may reach 10% this year.

Gundlach was a keynote speaker at the Exchange ETF conference in Miami. He is the founder and chairman of Los Angeles-based DoubleLine Capital.

“A year ago, inflation was thought to be transitory,” Gundlach said, “but the only thing transitory was the use of word ‘transitory.’”

“Maybe we will see 10% inflation.”

Inflation is a lot higher than what the government reports, according to Gundlach. Using the methodology in place under the Carter administration, it would be higher than the maximum it reached then, which was 14.6% in 1980.

“We would be at a 16 handle under the same methodology as under Jimmy Carter,” he said.

Nonetheless, he said inflation could fall in the months ahead, but not to 4% this year, as many are predicting. It depends on energy prices and, with $100/barrel of oil, we should not expect anything close to 4%.

Bonds are performing worse than stocks this year, he said, despite real yields being more negative than under Jimmy Carter.

Some core bond funds are down 12% year-to-date. “Who wants to be the ‘bond king’ these days?” he said. The stock market is wildly overvalued, according to Gundlach, but not as bad as bonds because of deeply negative real yields.

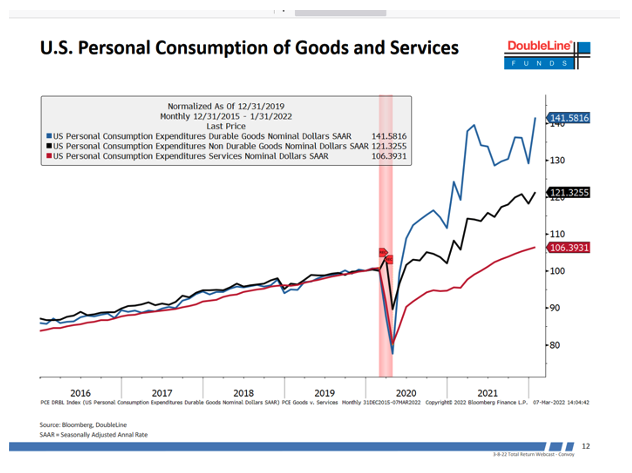

Gundlach said the most interesting economic chart (shown below) is that of personal consumption of goods and services. They were tracking identically from 2016 to 2020. Then the federal stimulus programs came, and durables spiked. Durable consumption has been pulled forward, while services have recovered to their trend.

Gundlach’s takeaway: Those who believe the 2022 economy will be the same as 2021 are “delusional,” because goods and services must normalize.

Labor force participation is down, he said, because many have discovered that “stealing is good.” In California, he said you can steal up to $950 of goods and not be prosecuted.

The biggest driver of inflation is wage growth. Wages paid to the youngest cohort of workers, age 16 to 24, have gone “vertical,” Gundlach said. Wages for other age cohorts were declining when the pandemic began, but six to eight months ago they started to rise and are now increasing sharply.

Wage growth is the highest in 25 years, but the Fed funds rate is barely greater than zero. The Fed has radically pivoted its rhetoric, he said. Its position was “QE forever” in December, using its tools (buying bonds and lowering the Fed funds rate). Now, the market predicts eight to nine hikes this year, which will push the Fed funds rate to about 2.25% by the end of this year.

Gundlach has been critical of federal spending and the resulting growth in the deficit, and he spoke harshly about the Fed. “The Fed has become increasingly worthless as it needs to support insane fiscal policies,” he said.

The yield curve has inverted prior to the last four recessions, and, he said, “we are on a recession watch now.” But the big risk is when the curve “dis-inverts,” going from an inverted to a normal, upward-sloping curve. The curve is now upward sloping by 27 basis points, based on the 2-10-year spread. “That is a cause for concern,” he said, “but I am not looking for a recession this year.”

“The yield curve suggests trouble ahead,” he said, “not in six to nine months, but in 2023.”

Gundlach said that he often can “see the picture” and has high conviction about an investment thesis, but “You must be patient. Once you know a crazy environment is in place, it can get crazier.”

The setup of the stock market fourth quarter of 2021 was very similar to the fourth quarter of 1999, at the peak of the dot-com era. But it took a while for the stock market to correct, and investors should not be complacent about stock prices.

The Nasdaq has outperformed S&P since 2002, he said, and its degree of outperformance now exceeds its peak during the dot-com era. “We should expect substantial underperformance for the Nasdaq 100 versus the S&P 500,” he said.

The S&P 500 outperformed Europe “massively” for 10 years until mid-2020, he said, but their performance has been equal since then. Gundlach’s highest conviction idea is that European equities will outperform the U.S.

The dollar will weaken when the next recession arrives because of rising budget deficits. The dollar will go below 70 on “Dixie” (DXY index). He recommended that investors gradually sell U.S. stocks and buy emerging market equities. The CAPE ratios for emerging-market stocks are less than half of U.S. stocks. Emerging markets are not riskier, though; at times, they have had higher CAPE ratios than U.S. stocks. He noted that emerging markets stocks have not risen in response to higher energy prices.

Emerging market equities will outperform U.S. stocks by more than 100%, he said.

Robert Huebscher is the founder and CEO of Advisor Perspectives.

Read more articles by Robert Huebscher