Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Each April, we are moved by hope – it is financial literacy month. To help close the growing savings gap, we strongly feel financial literacy and better knowledge of retirement and financial planning fundamentals are critical to securing more stable financial futures. Individuals are being called upon to secure their own financial wellness.

Recent research shows much work remains to be done. For example, a 2021 survey by the Insured Retirement Institute (IRI) found that only 44% of Americans will have enough income to retire. It’s difficult to navigate confidently toward your retirement if you do not know the terms and rules of the road.

The rapidly changing nature of financial literacy is best summarized by Investopedia’s recent financial literacy survey. It found that more millennials own cryptocurrencies than stocks (some 38% own crypto, just ahead of the 37% who own stocks). Moreover, 28% of millennials say they are planning to rely on their cryptocurrencies to support them in retirement versus relying only on “savings.” The cryptocurrency figure was about the same as the percentage who planned to rely on stocks.

While we will reserve our opinion on whether cryptocurrencies are any better than public equities as the backbone of investment strategies, these survey results highlight investor distrust in traditional financial strategies and institutions.

The 2022 Ariel-Schwab Black Investor Survey found Black investors specifically lack trust in the stock market and financial institutions. Black Americans increasingly turn to newer types of assets that are less likely to be associated with they believe is structural discrimination, the study found. Correspondingly, Black Americans are less engaged with traditional forms of investing, such as employer-sponsored retirement plans, creating yet another serious savings issue.

These are just a few examples of the widening trust, knowledge, and savings gaps unfolding before our eyes. This April and beyond, it’s vital we step up efforts to promote investor education and basic financial literacy.

Impact before profit

We strive to help individuals, couples, and families gain confidence with their investment plans by empowering advisors with the tools necessary to make investment objectives more achievable. While targeting specific risk-and-return objectives is part of the planning process, just being able to sleep at night is often a client requirement. Part of creating a positive impact is helping people understand the basics of retirement planning and giving the everyday Americans confidence to “stay invested.” It is imperative to make individuals more confident about their financial future by working to instill good saving and investing habits. Consider that 51% of Americans have less than three months’ worth of emergency savings, according to Bankrate.com. That means some 125 million U.S. adults are under-saved.

Sobering evidence shows that financial anxiety is a real threat. New research reveals that stress related to money makes people 20 times more likely to attempt suicide. Moreover, 16% of suicides are directly related to financial problems.

Simply enduring a negative wealth shock can have deadly impacts. Researchers from Northwestern University and the University of Michigan found that individuals who lost 75% of their wealth over a two-year period were 50% more likely to die over the next two decades. Financial literacy and higher confidence not only improve lives, but they can save lives, too.

These are real challenges and they hit home for far too many families. We are mindful of these unfortunate realities each day. It’s part of what drives us to improve the financial lives of all people, regardless of wallet size.

We are financial “teachers”, not just advisors

With so many account types, investment funds, tax laws, and changing rules, figuring out what’s what is trickier than ever. Moreover, personal situations are constantly evolving – from getting married to buying a house to having kids to planning for retirement. Anything that can help simplify these variables while also protecting what people have worked so hard to earn is invaluable.

This can often begin with explaining the “why” behind investments and risk management strategies. Rather than focusing solely on the “how,” we know that when investors better appreciate the why behind investment decisions, they can commit to financial plans with more confidence, even in the face of great uncertainty.

We strongly support elevating financial knowledge through transparent and easy-to-understand protective investment products, but also with resources to help investors and savers understand why they own something.

Reduce risk, relieve anxiety

A clear understanding of what’s in a retirement account builds confidence and relieves financial anxiety as people near retirement. Knowing how inflation could erode a portfolio or that a 50% stock market decline may not derail a retirement plan are major upshots of protective investments such as annuities and structured notes. Annuities specifically can provide lifetime guaranteed income to offset the hard-to-quantify risk of the stock market.

Annuities for downside protection

Speaking of risks, the sequence-of-returns risk is another challenging topic to explain to pre-retirees. The notion that a quick market drop at the start of one’s retirement can be much more devastating than one later in life does not make intuitive sense – common knowledge suggests that an individual should take on more stock market risk earlier in life and less as they get older. The “100 minus your age” rule of thumb is tossed about as a guideline of how much equity exposure someone should have, but that heuristic has been proven to be flawed. Part of becoming financially literate is recognizing major risks so that they can be responsibly managed.

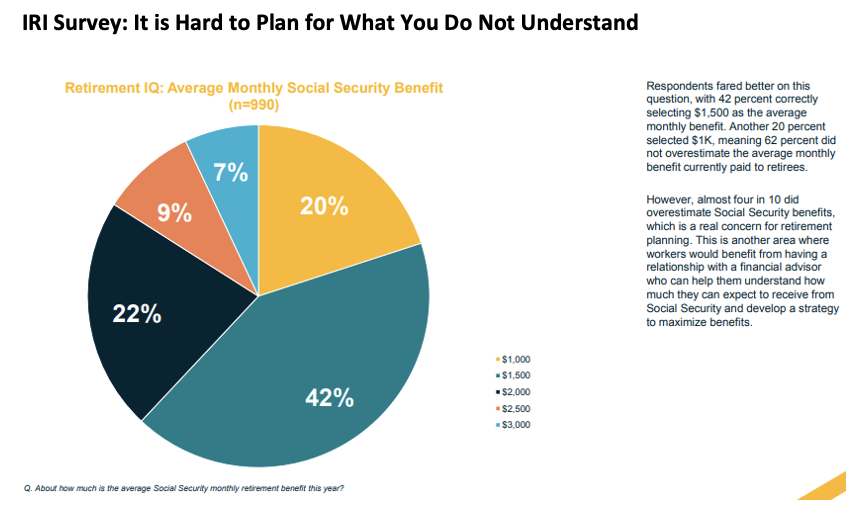

Lifetime-income solutions not only help mitigate sequence-of-returns risk, but they can also help meet retirement-income goals that Social Security alone might not meet. The IRI survey, mentioned earlier, also found that people do not have much knowledge of what their future Social Security benefit will be. Four in 10 respondents overestimated their average benefit. The risk is that some people will simply not have enough income in retirement to keep pace with their overall cost of living. Annuities (and structured notes) can be used to augment Social Security so that there is no shortfall come retirement age.

IRI Survey: It is Hard to Plan for What You Do Not Understand

The so-called “safe withdrawal rate” has come under fire recently. It used to be that a retiree could pull 4% per year from their retirement savings, then live comfortably on that amount without drawing down a portfolio. Amid today’s historically low interest rates and high stock market valuations, it is increasingly likely that the old way of thinking will not suffice. Research from IRI uncovered that fewer than three in 10 of those surveyed could accurately calculate how much they could withdraw each month from a diversified portfolio. Annuities and structured notes can help pinpoint a more precise monthly income figure so that retirees do not run the risk of running out of money.

Conclusion

We need to equip households with the resources to better understand sound risk management techniques, products, and solutions. Not only should we offer transparent and competitively priced protective investments, but we must simplify the process. Our goal is to make a positive impact on people’s financial lives so they have confidence in the future with minimal financial stress.

Biju Kulathakal is the co-founder and CEO of Halo Investing where he leads the organizational strategy and team. He was one of the early co-founders of Redbox. In addition, he was a founder and the past chairman and CEO of Trading Block Holdings, an online brokerage firm specializing in option traders.

Jason Barsema is the co-founder and president of Halo Investing, where he leads the team and product vision. With over a decade of experience managing structured notes, he built the Halo platform to provide all investors access to this incredible investment product. Jason previously was a partner on a large private banking team at Credit Suisse, where he managed portfolios for ultra-high net worth individuals and institutions.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.