Savers are about to learn one painful and one surprising lesson about interest rates and banks.

First, just because the Federal Reserve is raising rates doesn’t mean the rate investors earn on their cash will rise as much — if at all. In fact, the financial repression in the form of zero rates suffered for more than a dozen years by those who are ultra conservative with their savings isn’t going away soon. Second, banks don’t want your money. Understanding these dynamics why will go a long way toward explaining why the stock market and other riskier assets may prove resilient to the tighter monetary policy that is coming as the Fed seeks to bring down the highest rates of inflation in 40 years.

First, a bit of history. In response to the financial crisis in 2008 and to pull the economy out of recession, the Fed reduced its benchmark rate to near zero, and banks naturally followed suit. But making access to credit easier and cheaper was only part of the strategy. The central bank also wanted to create the “wealth effect,” hoping people would take money out of savings and money market accounts and put it into riskier assets such as stocks, sparking rallies that would make people feel richer.

Although not an official Fed policy, policy makers over the years have talked about how rising prices for stocks and other assets tend to boost consumer spending and the overall economy. Former Fed Chairman Alan Greenspan told Bloomberg News in 2009 that “all of the statistical evidence indicates that the level of household wealth is a major factor in consumer expenditures.” This gave rise to the concept of “TINA,” which stands for “there is no alternative.” In other words, savers had no choice but to put their money into stocks if they hoped to earn any type of return. And it largely worked, especially for higher-net-worth households, as the S&P 500 Index staged a historic rally, generating a total return — price appreciation plus dividends — of 614% since early 2009, or 16.2% a year.

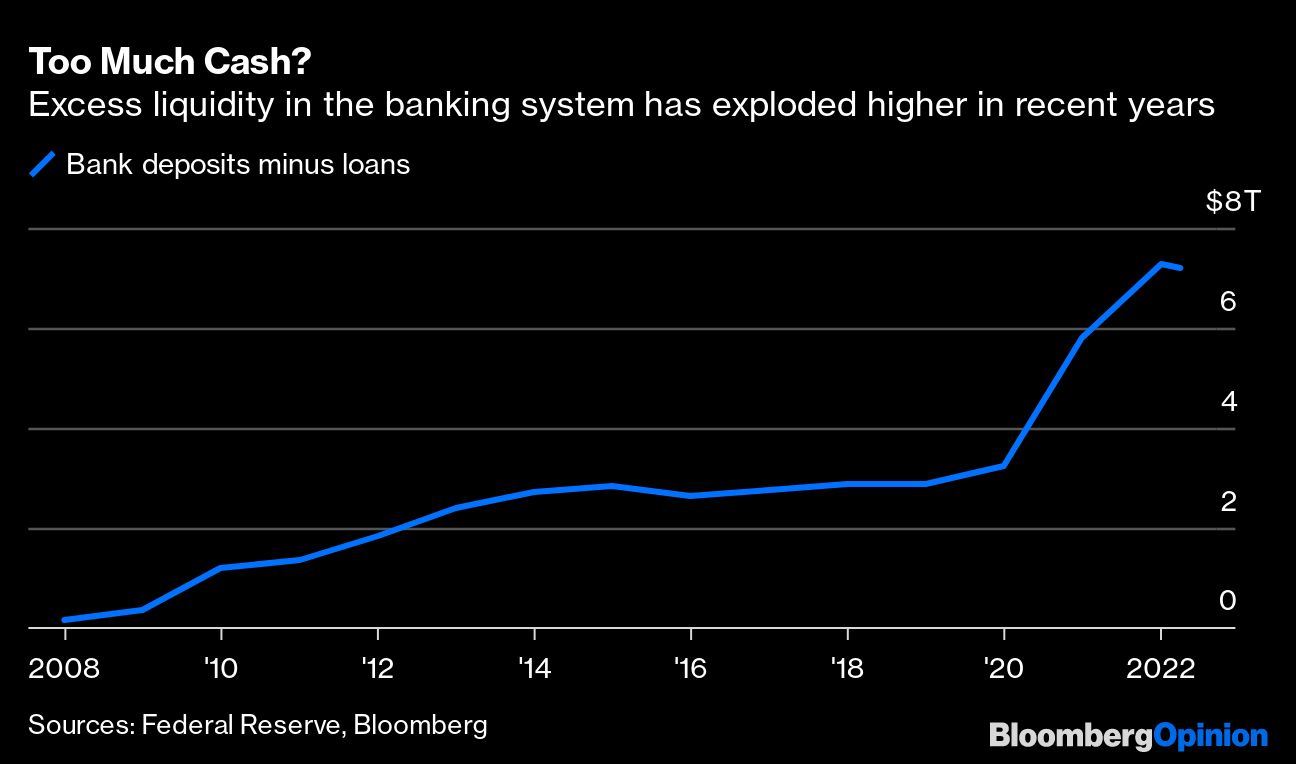

The problem for savers now is that the Fed also took the added step of pumping money directly into the financial system by buying bonds in the secondary market through a program known as quantitative easing. The Fed’s balance sheet assets have risen from less than $1 trillion in 2008 to about $9 trillion now, more than doubling in size since the start of the pandemic alone as the central bank accelerated the purchases to help support the functioning of the financial system. At the same time, the government pumped trillions of dollars directly into the pockets of consumers and the coffers of businesses to help them weather the lockdowns.