19 Reasons to Run Like the Wind from Direct Indexing!

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The arguments for direct indexing are more off-center than Louis Rukeyser’s side-part.

I don’t care how many PhDs are going to argue against me; direct indexing is Wall Street’s attempt at squeezing more fees out of the American public using advisors as the pawns.

Don’t fall for it – here are 19 reasons you should run as fast as you can!

Why this product originated

You thought I was going to launch into some diatribe about the history of indexing and the altruistic intentions of John Bogle.

Right?

Wrong.

As Scott Salaske of Firstmetric says, direct indexing has nothing to do with indexing.

Trade commissions gone + low fees from indexing = Wall Street needs to come up with a new way to suck money out of investors.

And from whence direct indexing is born.

😣

Fiduciaries are the target

Direct indexing is the fee-only fiduciary version of whole-life insurance.

The growth trend is low-cost indexing by fee-only advisors, and so Wall Street has to figure out how to use the allure of the idea of the index fund to charm all those independent, fiduciary-touting IARs.

You realize that, right?

You realize that, right?

Don’t be charmed!

The snake charmers define direct indexing as a strategy that replicates the construction of an index using a separately managed account, supposedly to tax loss harvest, get a client out of a concentrated position or make it a more personalized strategy.

Here are 19 reasons direct indexing isn’t what the people selling it want you to believe:

1. The whole goal is to get the investor stuck

After you realize the initial tax alpha by selling the losing stocks in the portfolio, it gets harder and harder to squeeze losses out of stocks. The portfolio becomes a collection of low-cost basis stocks.

To avoid an arduous portfolio unwinding, clients have to:

- Stay with the strategy (and keep paying the fees) to avoid realizing further capital gains on stock sales.

- Leave the stocks to charity – requiring an advisor to work with you on a DAF for 0.60%+ platform fees (or more) + investment fees. Ah, much better.

- Hold the stocks until you die and your heirs inherit them with stepped-up basis (something to look forward to).

- Stay with the advisor because you can’t manage any of this alone.

All of this sounds like what Rick Ferri calls “complexity for the sake of job security.” And the financial services industry has been particularly adept at creating complexity and making sure the investor is good and stuck, good and locked in, so that to escape will be costly.

This is no better than a variable annuity! In fact, a variable annuity is one product, but direct indexing reaches even further – it takes over the whole portfolio.

Open your eyes. Any product that gets your client stuck is not a good one. I don’t care what the benefits may be; you were hired to create more options, not fewer for your clients.

Don’t do this to your clients!

2. Trading one capital gain for another

Tax-loss harvesting is the main selling point everyone is cheering about. It’s trading one gain for another gain, though, because in the long-term you will create gains in far more securities. You’re buying 500 of them and they’re inevitably going to increase in value over time.

You're just kicking the tax can down the road, because you will pay taxes on the appreciated shares you bought to replace the original shares.

And what if capital gains tax brackets or rates change? I know, you insist that it’s never going to happen, so you can stuff people’s dough into those tax-deferred products you sell!

However capital-gains rates are the lowest they’ve been since 1941.

3. Tax loss harvesting is not a viable long-term investment strategy

Buying a bunch of stocks and hoping some of them go down enough for you to cut them just in time is not the purpose of investing.

Since when was the point of investing to lose money so you could get a tax loss? What’s that line that you all say on your websites about long-term wealth accumulation?

It’s gambling. There’s no guarantee the market will move against you, opening up a window for you to execute tax-loss harvesting. What happened to that line all of you say about, “We never chase short-term returns?”

But chasing short-term losses is okay (lol).

Huh?

4. What’s wrong with paying taxes?

You don’t go broke from paying taxes; you go broke by not planning for them.

Does anyone see this “avoid taxes at all costs” scenario as selfish? Taxes pay for the military, the firefighters, the police, and the teachers. Don’t you want the ambulance to come when you get sick?

Why can’t you just see it as your civic obligation?

Every dollar you save in taxes will be paid by another American – most likely someone who cannot afford to engage in tax-loss harvesting.

I can see basic tax planning… but this? Do we have to twist ourselves into pretzels to avoid every single penny of tax possible?

5. You may accidentally convert qualified dividends to non-qualified

Tax harvesting too rapidly can cause dividends to lose qualified status. Please see page 2 of the instructions for Form 1099-DIV (rev January 2022.)

And guess what that does to your tax bill if you mess up?

6. It’s a “greatest hit parade” of compiled, non-transparent fees

Fees, fees everywhere and not a drop to drink. Here are some examples of the lack of transparency and confusion that has earned us a stinking reputation.

Disclosed in an incomplete fashion

From the website of one direct indexing provider:

First $500K: 0.25%

Over $500K up to $2M: 0.20%

Assets over $2M: 0.15%

Seems clear enough, right…but what about all these fees?

Odd-lot differentials could be huge in some cases

Trades effected with broker-dealers other than affiliates

Mark-ups or mark-downs by broker-dealers

Transfer taxes

Exchange fees

Regulatory fees

Handling charges

Electronic fund and wire transfer fees

Other charges applicable to a managed account

And of course, the advisor is going to tack on their fee for doing this, and if they don’t charge for it, they’ll make up for it in other ways.

Kickback in disguise?

In another company’s ADV (fees were not even disclosed on the website, I had to go to the ADV to find them):

PROVIDER may also offer discounted pricing to Intermediaries paying the Management Fee on behalf of the Client.

Okay, so let me get this straight.

The advisor bumps up their advisory fee in the amount of 25 bps or whatever the indexing provider is charging them, and then gets a lower fee charged by the provider.

And even if they don’t… isn’t this like a kickback/payment for order flow?

But how many clients are going to catch that? The advisors are all going to tell their clients it’s free and they’re going to think their advisor is just swell.

Vague enough for you?

Another example of murky fee language:

You pay a fee to PROVIDER based on a percentage of the assets we manage on your behalf. The more assets you have with PROVIDER, the more you will pay in fees. As a result, we have an incentive to encourage you to increase the amount of assets we manage. We generally charge clients on a quarterly basis.

But what are the fees???

When I get to the ADV, I see why they had to beat around the bush so much. The fees on all the equity portfolios are 35 bp or more, as high as 60 bp in some cases.

7. The economics don’t make sense

Which one of these makes the most sense to you?

- I can hire an advisor to run a separately managed account for me at 1.25% a year. It won’t have 500 (eventually low-cost basis) stocks in it. I pay $12,500 on a $1 million portfolio.

- I can hire a fee-only advisor for 75 basis points. They invest in a simple ETF portfolio and provide in-depth planning. The asset-weighted average expense ratio is 0.18% for index equity ETFs. I’m at 93 bp annually (or even lower if I’m holding fixed income). I pay $10,800 on a $1 million portfolio.

- I can hire a fee-only advisor for 75 basis points. The advisor puts me on a platform charging an extra 20 basis points. However, due to the increased operational workload, the advisor tacks on an additional 15 basis points. I’m paying 1.1%, plus now I own a 500-stock portfolio that my accountant has to sort through every February, leading her to double her fee. All of this assumes no surprises from any of the incidental fees mentioned in #6.

8. It’s harmful to smaller portfolios

Once again, the financial industry is preying on the smaller investors.

What scares me is that some of these platforms are targeting investors with as little as $2,000 to their name, made possible by fractional shares.

Let’s say I had $10,000 and I were invested in a direct indexing strategy following the S&P. Well, given that the weighting of Embecta (EMBC) is 0.000005, I’d be holding 0.0015 shares. That makes no sense; EMBC probably would get sampled out, along with a lot of other stocks for the same reason. Now just for reasons of small weighting, I’ve got a huge tracking error.

If the economics aren’t great for a $1 million portfolio, they are abhorrent for a small portfolio.

Advisors, don’t pitch small clients this – leave them alone!

9. The terminology is misleading

The word “indexing” has the connotation of simplicity and low-cost. Now the industry has taken this word and morphed it into something that is a bastardization of its true meaning.

Even if it were indexing, after you start selling stocks to get the tax losses, it’s not an index fund anymore. It’s not going to be like an enhanced index with 1% tracking error – it’s going to be way higher than that, probably above 4% which, according to Zephr, is what categorizes an active manager.

Instead of “direct index,” they should just call it “overly diversified SMA.”

10. It increases workload for everyone involved

Let’s say in a direct indexing scenario I own 505 stocks (for ticker-related reasons there are 505 issues in the S&P 500 index fund, not 500 as you would think) instead of owning SPY.

What are the differences in how my account is serviced, operationally?

- I get a shareholder report for every corporate action that occurs, which I have to manage.

- I have to vote proxies on every stock when they have their annual meetings.

- With 500 stocks, you don’t think your phone is going to ring every time Cramer makes some explosive statement?

- If I’m an executive with access to inside information, changes in my work status now become more sensitive, requiring more immediate communication with advisor, custodians, etc.

Who is going to go through the 300-page 1099 and make sure that all the gains you’re being charged for are reconciled properly with your financial statements?

Who has time for this?

Think about the impact on accountants. Last year, my custodian made a $40,000 mistake on my 1099-DIV. It took my CPA four phone calls to get it straightened out. What’s the IRS going to do about these errors? We’ve just made their job 500 times harder!

And what do you think is going to be the result of this increased burden?

Yup.

Higher fees!

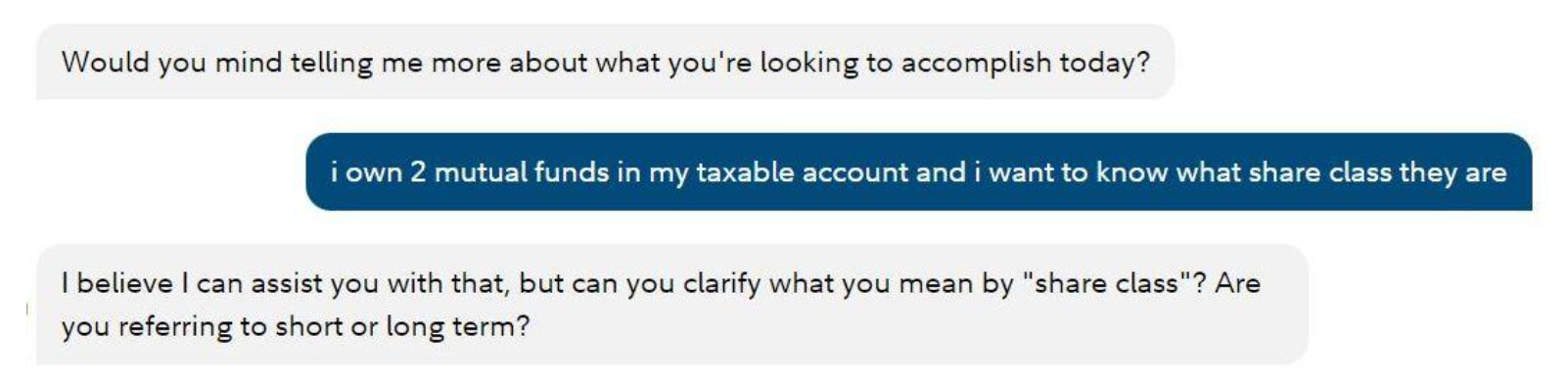

11. The custodians can’t handle this

In case you haven’t noticed, the customer service at the custodians has gone down the drain.

Example:

Yes, in case you read it quickly, the customer service representative at the custodian needed me to tell them what a share class is.

Harrowing.

And you think they’re ready to go through this, times 500, for every client they have? It serves them right for pushing this to get the order flow. (What! You mean my trades aren’t really free?)

😉

12. It’s yet another product (sigh)

When are we as a profession going to get away from this shiny object syndrome?

As much as advisors love to pound the fiduciary drum, very few are willing to question it when Wall Street tosses out a new toy (direct indexing, interval funds, crypto, etc.).

Then a hypnotic snake trance takes hold.

Why can’t the focus be getting to know the client in a deeper way, communicating better in annual reviews and meetings, increasing the impact of your financial planning on their lives?

Tell me, where are the advisors who focus on advice, not products?

Oh yeah – they’re called advice-only, and if you’re down with the movement you can join our LinkedIn group.

13. It’s problematic for decentralized accounts

You may not be able to realize the losses your tax harvesting has effectuated if you don’t know what else is going on with money held elsewhere (remember the wash sale rule?). This is problematic in cases where you are splitting the portfolio with another advisor or the client is managing part themselves.

14. Not great for retired people

Retired people won’t be accumulating and adding new money to (supposedly) generate tax losses.

And are you going to sell 500 stocks in accordance with the “index” weightings when these retired people need to take RMDs or money to live on?

15. Outsized downside potential

No client is going to fire you because you didn’t tax-loss harvest this way. There are other ways to protect a concentrated position.

Think about this rationally.

Nothing bad happens if you don’t do this; but a lot of bad could happen if you do. Why take a risk on an unproven strategy in which there are so many elements you can’t control?

16. Exaggerated benefit to executives with concentrated positions

Then there’s this pitch that you need to do this for your clients who own a ton of company stock.

And did you ever consider this scenario: You create the “Humpty Dumpty Portfolio” and then the client’s compliance department calls to them that instead of having an exclusion on their own company stock, they can’t buy the entire sector? What if the client is a healthcare executive, when healthcare is 13% of the S&P?

Why don’t you:

- Create a portfolio using sector ETFs (instead of their underlying stock).

- Use a cashless equity collar (long the long-dated put, short the long-dated call).

17. Analytical clients are going to bludgeon you over this

Even if the indexing provider assumes responsibility for managing the stocks, the client is still going to come for you if they have questions.

Does anyone work with engineers? They’re going to call you whenever Cramer says something ludicrous about a stock they own. And what are they going to say when they get their 300-page 1099 and/or year-end tax statement?

Better up your cell phone minutes because your phone is going to be blowing up all day and night.

18. We all know that ESG doesn’t work the way product manufacturers promise

I wish we could all stop pushing the idea that direct indexing is great for impact or ESG investors. Look, ESG is the adult version of the tooth fairy. We all know it’s not what everyone wants you to believe it is.

If someone says they want a personalized portfolio that supports renewable energy, why don’t you try telling them the truth about ESG, and then see if they still want to pay the fees for this? Or even better, steer them clear of ESG entirely. Then with the money saved from the fees they would have paid, they can make a yearly donation to their favorite renewable energy non-profit.

19. Do clients want this anyways?

Who came up with this idea – us or them?

How about listening to the client for a change? Our profession would be so different if decisions were based on what clients told us they needed.

If you want to add value to your clients, call them on the phone and say something like this:

How is your business going? It’s 9% inflation – is that having an impact on anything?

(Better option) What are three things I can do better as your financial advisor?

Resist the charm

If you are unable to break the snake dance trance and still insist on moving forward with direct indexing:

Question the vendors and ask the hard questions until you get total clarity in writing.

Map out all the scenarios.

Know how all the numbers and fees work in all possible cases.

Don’t leave anything to assumption.

Ask yourself, “If my client were to understand the implications of owning all these stocks, with complete and total clarity regarding all aspects of their servicing and the related fees (all layers, not just one), would he or she be happier than they are now?”

Assume this will not work for the majority of your clients (because it won’t).

And most of all, don’t let the snake charmers turn you against your own clients.

Just like you said in the fiduciary oath you took.

Sara’s upshot

As much as I’d love to believe all the virtue-signaling that the next generation of financial advisors put forth with vigor and consistency, their affinity for this nonsense product leads me to question:

Where are the advocates?

And where is our integrity?

Come out from hiding wherever you are and join me in the resistance movement – in your practice, in the social media feed, and in the Zoom calls. The change is already happening; every day we gain more and more territory.

It’s a new era in this profession where for the first time the focus will be progress, not products, led by the rare few who are defined by their values. And stand for something.

If you want to join me in making history, join the resistance:

Advice Only, Flat, and Hourly Fee Advisor Newsletter

Register for June 7th webinar here.

Sara Grillo, CFA, is a marketing consultant who helps investment management, financial planning, and RIA firms fight the tendency to scatter meaningless clichés on their prospects and bore them as a result. Prior to launching her own firm, she was a financial advisor.

Sources

Conversation with Scott Salaske, CEO of Firstmetric, April 20th, 2022.

Luscombe, JD, LLM, CPA. (March 9, 2022). Historical Capital Gains Rates. https://www.wolterskluwer.com/en/expert-insights/whole-ball-of-tax-historical-capital-gains-rates. Retrieved on April 26th, 2022.

S&P Dow Jones Indices. S&P 500. https://www.spglobal.com/spdji/en/indices/equity/sp-500/#overview. Retrieved on April 26th, 2022.

Slickcharts. S&P 500 Companies by Weight https://www.slickcharts.com/sp500 Retrieved on April 26th, 2022.

Zephyr. Informa Investment Solutions. https://www.styleadvisor.com/resources/statfacts/tracking-error

Investment Company Institute. 2021 Investment Company Fact Book. https://www.ici.org/system/files/2021-05/2021_factbook.pdf

IRS. Instructions for Form 1099-DIV. Qualified Dividends. https://www.irs.gov/pub/irs-pdf/i1099div.pdf

Sara Grillo does not hold positions in any of the securities mentioned in this article.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All