Well, that was quick. In just more than a week, US Federal Reserve Chair Jerome Powell has gone from expressing confidence that policy makers will be able to avoid pushing the economy into a recession while rapidly raising interest rates to control inflation to remarking, as he did on Thursday, that a downturn is out of the central bank’s control.

At a press conference on May 4, after the Fed raised its target rate for overnight loans between banks by half a percentage point in the biggest increase since 2000, Powell told reporters that “it’s a strong economy” and nothing suggests “it’s close to or vulnerable to a recession.” Contrast that with comments he made Thursday in an interview with Marketplace public radio, where he said, “The question whether we can execute a soft landing or not, it may actually depend on factors that we don’t control.” The factors Powell cited included geopolitical events (the war in Ukraine) and supply chain bottlenecks (China’s Covid-19 lockdowns).

Pointing out this seemingly less confident tone by Powell in such a short period — and on the day the Senate confirmed him in a bipartisan 80-19 vote to another four-year term — isn’t a criticism of him or his colleagues, who are often derided as being behind the curve when it comes to steering the economy through difficult times. Rather, it underscores just how rapidly the economy is deteriorating.

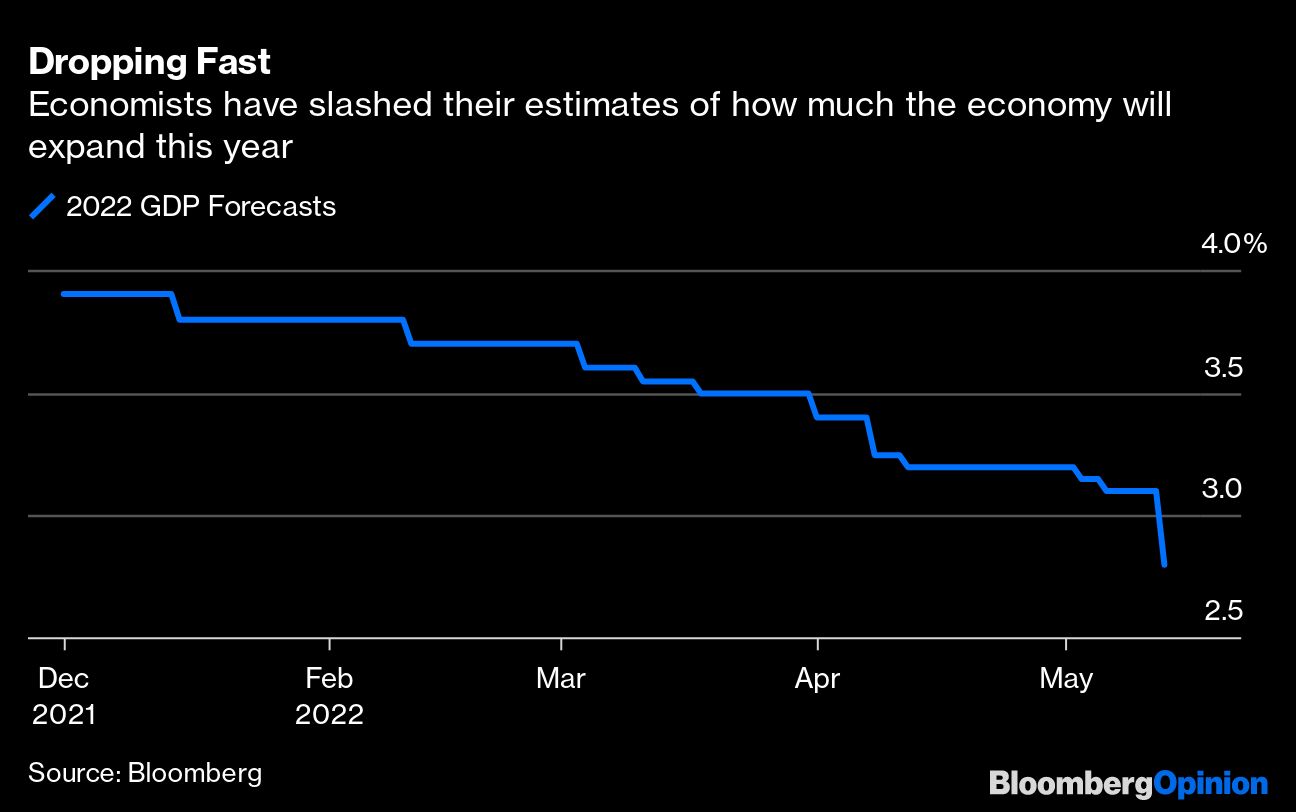

As we know, the economy unexpectedly shrank in the first quarter at an annualized rate of 1.4%. It was the first contraction since the early days of the pandemic in 2020. Economists are increasingly convinced that the slowdown wasn’t an anomaly. Bloomberg News’s monthly survey of more than 70 economists released Friday showed that they slashed their forecasts for the annual increase in gross domestic product to 2.7% from 3.3% in April’s poll and 3.6% in March. It was 3.9% heading into 2022. It doesn’t take a mathematician to conclude that the trend isn’t the economy’s friend.

If that wasn’t concerning enough, economists also put the odds of a recession happening within one year at 30%. If that seems manageable and not such a risk, consider that it’s almost double the average of 17% between the end of 2009 and the start of 2020. On-the-ground data only confirms the weakening. The US freight industry is suffering; Cass Information Systems Inc. said this week that transport volumes slowed for a second consecutive month in April, dropping a seasonally adjusted 3.5% from March. “After a nearly two-year cycle of surging freight volumes, the freight cycle has downshifted with a thud,” Cass said in a statement.

There’s no reason to believe the drop in shipments will rebound soon, if the consumer is any guide. On Friday, the University of Michigan said its US consumer sentiment index fell in May to the lowest since 2011. Nearly half of respondents don’t expect their incomes to keep pace with inflation over the next 12 months. This is as clear a sign as any that consumer spending, which accounts for about two-thirds of the economy, will soften, according to Bloomberg Economics:

The tally comes ahead of retail-sales data for April, which we expect will show a decline in discretionary spending as inflation diverts purchases toward necessities such as food and gas. As surging prices squeeze real wages, Americans are cutting unnecessary purchases and relying heavily on credit cards.

Nevertheless, despite the weakness in the economy and the financial markets, where investors have suffered trillions of dollars of losses on stocks, bonds and crypto this year, Powell and his fellow policy makers reiterated the need for at least two more interest rate increases of half a percentage point each — likely at the next two policy meetings in June and July — if they hope to start bringing inflation back toward their 2% target from the current 8.3% level. “Unless there are some big surprises, I expect it to be appropriate to raise the policy rate another 50 basis points at each of our next two meetings,” Federal Reserve Bank of Cleveland President Loretta Mester said Friday.

It’s not all bad news. Consumers and businesses are perhaps in their best financial shape ever, which should help them better weather a recession. Consumers have spent the years since the financial crisis deleveraging and are sitting on $4.06 trillion of savings, up from $1.16 trillion at the end of 2019, according to the Fed. The previous high for this metric before the pandemic was $1.41 trillion. Goldman Sachs Group Inc. said in a report this week that corporate “balance sheets nevertheless remain in one of their strongest positions of the past twenty years.” The firm said it still expects a minuscule default rate of just 1.9%, even in a recession, well below the long-term average of 4%.

So, as my Bloomberg Opinion colleague Allison Schrager explained this week, there’s every reason to believe the next downturn will be mild, and perhaps barely noticeable, unlike the painful recessions of 2001 and 2008-09. There’s also reason to believe that the Fed might not need to continue boosting rates throughout this year and perhaps into 2023. “No matter what you may think given some of his musings over the prior couple of months, Powell is a dove through and through,” Tom Porcelli, the chief US economist for RBC Capital Markets, wrote in a research note this week. “Job losses (even if just one month’s worth) and inflation that has slowed quite a bit, guess what that likely means for the Fed? The hiking cycle would be over.”

Recessions bring uncertainty, retrenchment and layoffs. They also often lead to political upheaval. Although it’s quite possible that next one may be barely noticeable, it’s increasingly looking, as Powell suggested, as if a recession will be unavoidable.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.