Gundlach: Oil Could Hit $150 This Summer

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits The price of oil, as measured by the benchmark WTI index, could hit $150 this summer, according to Jeffrey Gundlach. That price may not be sustained, he said, “but the path of least resistance for oil prices is up.”

The price of oil, as measured by the benchmark WTI index, could hit $150 this summer, according to Jeffrey Gundlach. That price may not be sustained, he said, “but the path of least resistance for oil prices is up.”

Gundlach spoke to investors via a webcast, which he titled “It’s Not Unusual,” and the focus was on his flagship total-return fund (DBLTX). Slides from that webcast are available here. Gundlach is the founder and chairman of Los Angeles-based DoubleLine Capital.

The title is from a hit song sung by Tom Jones in the mid-1960s, which led to two appearances on the Ed Sullivan show. Gundlach chose it because, he said, “it is not unusual for markets to get unusual.”

But it would not be that unusual for WTI to hit $150/barrel. It peaked at $140 in 2008, during the great financial crisis. Adjusting for inflation, that would be greater than $150 today. WTI closed at $119.81/barrel on the day he spoke.

The real Fed funds rate is highly unusual, he said, at -749 basis points. The CPI has stopped rising year-over-year and will start to fall in the second half of this year. As it decreases and the Fed funds rate is hiked, the real Fed funds rate will increase.

The only asset class that is up this year is the Bloomberg commodity index, and it is up 38%. Bitcoin has been the worst performer, down more than 30%. Since the last Fed meeting in early May, volatility is down and yields are up modestly, he said.

Inflation was a prominent topic in his talk. He said it was largely fueled by excessive government spending, including an “outrageous increase” the deficit and stimulus programs.

Export and import prices are the best measure of inflation, because they are not subject to substitutions and changes in methodology, as is the case with the CPI and PCE. Based on today’s methodology, inflation during the Carter administration would be approximately 9.1%, in line with what we are experiencing now.

Year-over-year, export prices are up 18% and import prices are up 12%. Averaging those two, Gundlach said that inflation is around 14%.

“We expect inflation will fall later this year,” he said, “but there is a question whether it will fall after that.” He predicted that CPI inflation will average 6% over the course of 2022.

Commodities have been “on a tear” this year, he said, following a small pullback in the fourth quarter of last year. Commodities are in a secular uptrend, according to Gundlach. Food consumption at home is up 11% and up 7.2% away from home. The war in Ukraine is responsible, he said, at least for price increases in wheat and barley.

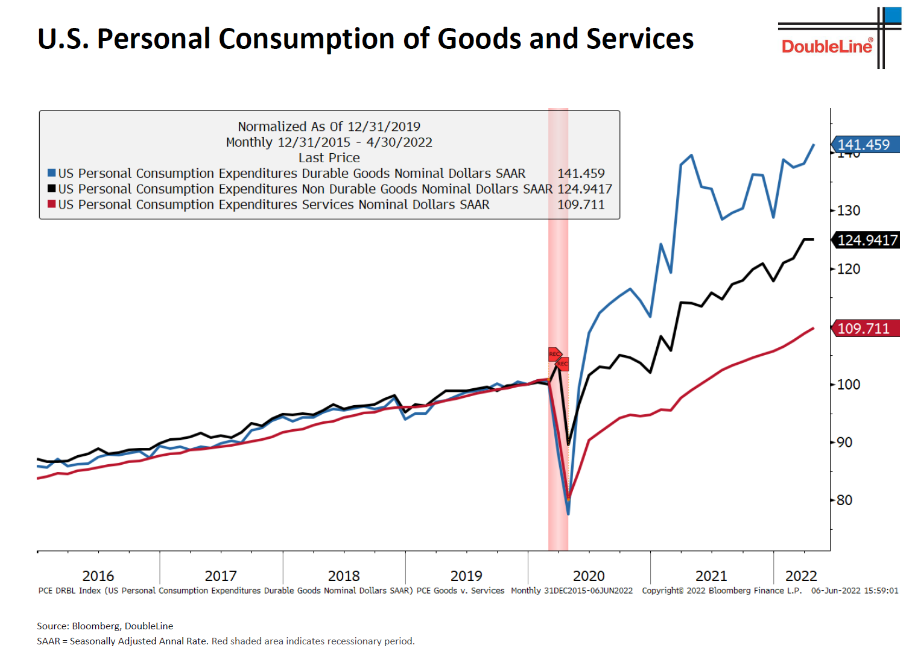

Below is what he called the “chart of the year.”

It breaks PCE index into durable and non-durable goods, and services. For four years prior to lockdown, all three were up consistently. With the lockdown, spending halted on all three. With the pandemic-related stimulus programs, durables exploded higher and are 25% above their trend.

“Durable goods spending has been brought forward and there will be years of slow spending to get back to trend,” he said. The same is true, to a lesser degree, of non-durable goods.

This explains why Gundlach expects sluggish economic growth. “It is difficult to see where earnings and growth will come from,” he said. “We will have headwinds for risk assets in the second half of this year.”

Consumer confidence is eroding, The University of Michigan survey is at levels consistent with a recession.

Home prices are up 37% over the last two years, and 30-year mortgage rates have doubled, from 2.75% to 5.5%. “It is not a good time to buy a house,” Gundlach said. Compared to pre-pandemic levels, monthly mortgage payments are up 68%. “One cannot expect the housing market to support economic gains,” he said. Affordability, as measured by the ratio of monthly payments to income, is at its highest level since the great financial crisis. One consolation is that mortgage rates are still less than CPI inflation.

Consumer revolving credit is “exploding to the upside,” he said, following a collapse during the lockdowns. He attributed the spike to pent-up demand for travel. “The consumer is dipping into debt,” he said, “which does not bode well.”

The gap between job openings and the number of people unemployed has never been wider, in part due to stimulus programs, he said. But it is mostly due to people dropping out of the labor force.

Commodities are a far better investment than stocks, Gundlach said. The commodity cycle will continue. Once the cycle turns, as it did early this year, commodities will outperform stocks by 800%.

The S&P faces strong headwinds from quantitative tightening (QT), rate hikes, and particularly rising real rates, he said.

Many long-term trends have reversed, inkling the outperformance of value versus growth, U.S. versus non-U.S. equities, the Nasdaq versus the S&P 500, and Europe versus the U.S. – even though the dollar has been strong. The U.S. is still outperforming emerging markets, he said, and will do so until dollar falls.

“That should happen because of the fiscal deficit,” he said.

If the dollar drops below 100 on the DXY, which is about 3% below its current level, “I will get very negative on it,” he said. He predicted that the dollar will ultimately go below 80.

This has been the worst year for the AGG index since 1980. Gundlach noted that some core bond funds are down 15%, while the AGG is down approximately 10%. The worst performers were high-duration bonds, including the investment-grade sector, which is down about 14% this year.

Gundlach said that agency mortgage-backed securities are very cheap, especially relative to investment-grade bonds. “At these valuations,” he said, “we are very bullish.” Mortgage-backed bonds are less likely to be refinanced in a rising-rate environment, which makes them less risky than other bonds. “This is a great time to buy mortgages,” he said.

The bond market is priced for a flat yield curve a year from now, he said, with short term rates up to 3% and very little change in 30-year rates.

“The market is priced wrong,” he said, “and the yield curve will not get to those levels.”

Gundlach was asked about recent comments by Jamie Dimon, CEO of JP Morgan, who warned investors to brace for an economic “hurricane,” and Elon Musk, who said he has a “super bad feeling” about the economy.

Recessions are inevitable, Gundlach said, and “it is just a matter of time.” A recession is “probably coming in 2023.”

The government’s response will be to slash rates and/or increase money printing, he said. “We will try those techniques one more time,” he said, “which is why I am negative on the dollar over the long term.”

Robert Huebscher is the founder and CEO of Advisor Perspectives.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All