Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Since the onset of the pandemic in March 2020, Washington has announced six freezes on student loan debt. The latest moratorium was announced by President Biden in early April, when interest and payments were deferred until September 1, 2022.

Especially at the beginning of the pandemic, when everything about the economy was disoriented, deferral of student loan interest and payments was welcome news to many of my clients and their children. Biden campaigned on the promise to forgive up to $10,000 in student debt per borrower, and since taking office he has canceled more than $16 billion in federal education debt, though most of the benefits have gone to borrowers with total and permanent disabilities, those who attended now-defunct institutions, and public-service workers.

While pushing back the start date for interest accrual and payments has been a relief to many, the fact is that September 1 is coming, and it is unlikely that the political tightrope act will allow an infinite number of additional delays. In other words, many of my clients or their kids will face repaying those loans. And given the inflationary environment and related rising interest rates, some of them will need to make careful choices about prioritizing their payback plans.

For one thing, the rising costs for everything from gasoline to milk means that borrowers will have less disposable income from which to make payments. Even if they were making their payments with relative ease prior to the moratorium, the dollars in their accounts won’t stretch as far now as they did then. Especially since wages have generally not kept pace with inflation, the prospect of loans with rising interest rates is not pleasant to contemplate.

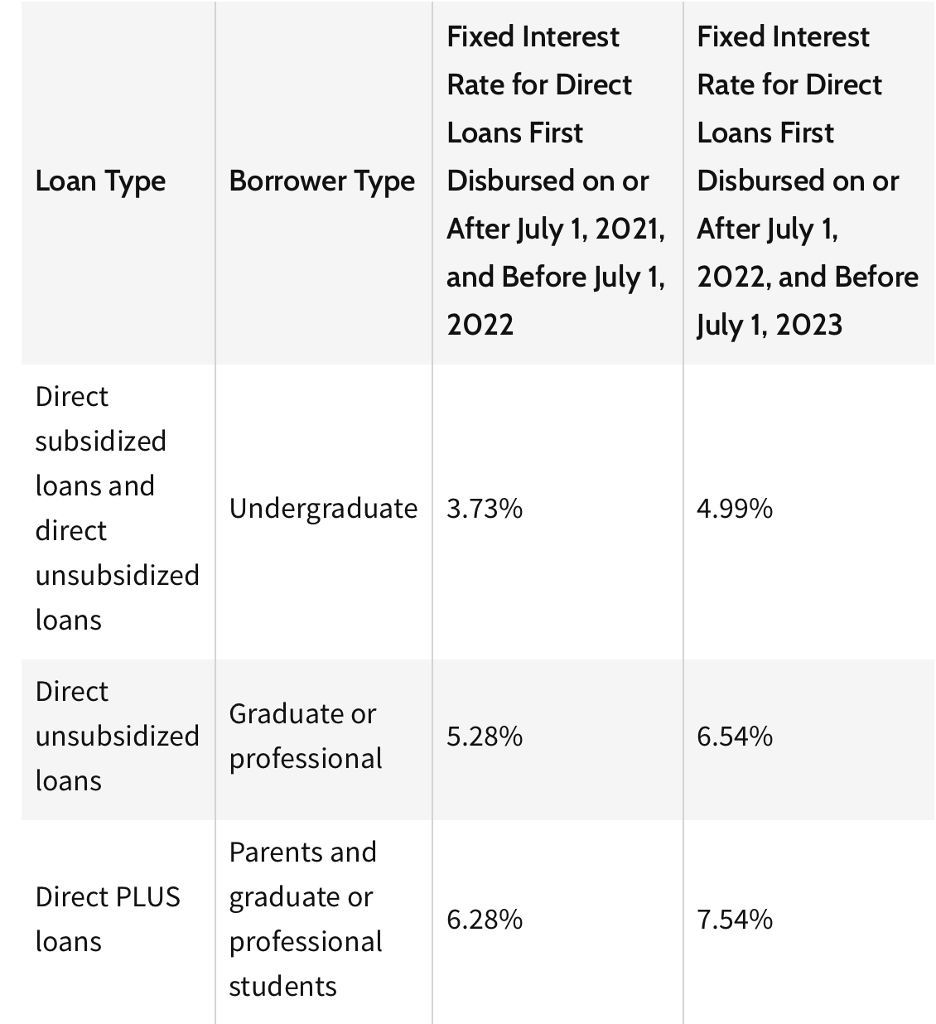

The effect of rising interest rates on student loans is easy to discern. Direct federal loans for undergraduate students went from an interest rate of 3.73% for loans granted between July 1, 2021 and July 1, 2022 to a rate of 4.99% for loans to be granted after July 1, 2022 and before July 1, 2023. Rates for graduate student and parent loans rose by a similar amount, but started at a higher point, as shown in the following table.

SOURCE: U.S. Department of Education, Federal Student Aid

Setting priorities

How can we guide our clients and their children as they negotiate repaying educational debt in this economic and interest-rate landscape? Talk to them about strategies for knocking out that debt as efficiently as possible – and there are several strategies that can work, depending on the individual situation. In fact, some of these will sound similar to conversations you may have had about how to get rid of credit card and other consumer debt. Here are some basics to cover with your clients.

-

Federal versus private loans. Federal student loans are backed by the government and include direct subsidized or unsubsidized loans that may be made either to the student or to their parents. They generally feature lower interest rates than private loans. Also, the interest rate for federal loans is fixed, whereas some private lenders offer adjustable-rate loans. Obviously, an adjustable-rate loan in a rising interest rate environment is not going to be as favorable for the borrower. Make sure your clients understand exactly what type of loan they have. Generally speaking, if they have adjustable-rate loans, the sooner they can either pay them off or refinance to get more favorable terms, the better for them. For this reason, paying off or otherwise disposing of private loans first can save borrowers a significant amount in interest payments.

-

Highest interest rate first. The logic here is obvious. Just as with credit card debt, knocking out the student loan with the highest interest rate is going to improve not only cash flow but also the balance sheet.

-

Smallest loan first. For some clients or their kids, getting a quick win produces the momentum to carry them all the way through. Once that first loan is paid off, encourage them to add the amount of that payment to what they’re paying on the next-smallest loan. This is the well-known “snowball method,” and for certain borrowers, it can work just as effectively with student loans as with other types of debt.

Gathering the data, reviewing the options

As you begin helping clients build their student loan repayment strategy, help them gather all the necessary information to obtain a good overview of where they stand. They’ll need to know the details of

- Each lender or loan servicer (whether federal or private);

- Loan balance;

- Interest rate (and whether variable or fixed); and

- Monthly payment.

In most cases, they will have several different loans, possibly with different lenders or servicers, so get all the information in one place. With everything laid out clearly, you and your clients will be able to evaluate which strategy is the best fit for the client’s situation.

For some younger borrowers, it could make sense to switch from a standard 10-year repayment schedule to an income-driven repayment (IDR) plan. These plans, only available with federal loans, allow for payment amounts adjusted for the borrower’s income level and can be a good way for borrowers with limited incomes (such as recent graduates just getting started in their careers) to keep their loans in good standing. The downside of IDRs, of course, is that they extend the life of the loan, resulting in more interest paid.

However you work with your clients or their children on student loans, the most important thing is to help them think proactively about their student debt and how it will be affected by inflation and higher interest rates. Our job as fiduciaries is to put our informed perspective at the service of our clients. By helping them look ahead and make a plan that works for them, we’re increasing their odds of success with their longer-range financial strategies.

Kimberly Foss, CFP®, CPWA®, CFT-I™ candidate, is president and founder of Empyrion Wealth Management, an RIA with offices in Roseville, CA, and New York City. Her book, Wealthy By Design, is a New York Times bestseller. She has been a commentator for NBC, ABC, Fox News and The Wall Street Journal. You can reach her at [email protected]

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.