Ignore the Fed at Your Own Peril

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Is all the attention to the Fed warranted, or is it a waste of time for advisors to monitor monetary policy developments?

The financial and investment news media has a myopic obsession with the Federal Reserve and monetary policy. Conjecture on potential interest rate moves has even been quantified with the CME’s Fed Watch Tool, which compiles the view on interest rates based upon Fed funds futures contract prices. Will it or won’t it raise rates? Will the increase be 75 basis points or 100 basis points? The financial markets seem to react to nuances in Fed Chairman Jay Powell’s remarks or those of regional Fed governors, leading up to or following Fed announcements.

Gerald Jensen, the co-founder and chief investment officer of Economics Index Associates, and I have been researching the association between Federal Reserve monetary policy and capital market returns for nearly three decades. In fact, along with Luis Garcia-Feijoo, Gerry and I published a book, Invest With the Fed, detailing our findings. Our peer-reviewed academic research identifies strong and persistent patterns in asset returns related to monetary policy. Understanding these patterns will help you enhance returns and better educate clients regarding risk and return expectations. You ignore the Fed at your own peril.

Are rising rates good or bad for investments?

Whenever the Fed is contemplating interest rate changes, talking heads debate the effect of rate changes on the value of equities. Some argue that a rate increase can be seen as affirmation that the Fed believes the economy is doing well and could not only withstand higher interest rates, but that higher interest rates are warranted. Others contend that rising rates are bad for stocks, as it increases firms’ cost of capital and newly issued bonds yield more, making stocks less attractive vis à vis bonds.

The way to resolve this debate is to look at the evidence. How have stocks and bonds performed in rising and falling interest rate environments?

Our research classifies monetary policy environments by looking at the direction of two widely reported interest rates that are either set or influenced by the Fed: the primary credit rate and the effective Fed funds rate. Using this classification scheme, we classified the monetary environment into three categories: expansive (easy money), restrictive (tight money) and indeterminate (mixed).

The evidence

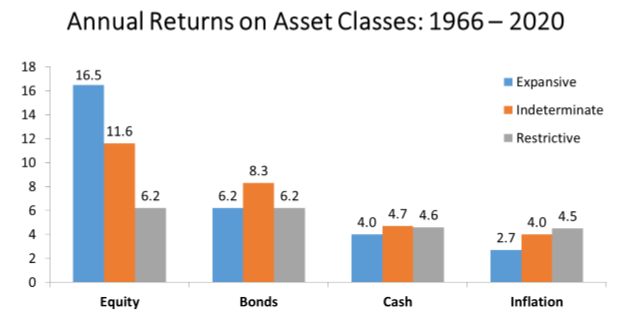

Over the 55-year period from 1966 through 2020, the returns to the stock market as proxied by the large capitalization S&P 500 index were dramatically different during expansive, restrictive, and indeterminate monetary policy periods as shown in the chart below.

The returns to the S&P 500 were 10.3% higher annually in expansive versus restrictive periods. The real return difference is even higher, as inflation was significantly higher in restrictive versus expansive periods. The real return to stocks was 13.8% in expansive periods and only 1.7% in restrictive periods. Clearly, the empirical evidence suggests that the debate between those suggesting rate hikes are good for stocks versus those arguing that rate hikes are bad for stocks is not a fair fight.

The returns to the S&P 500 were 10.3% higher annually in expansive versus restrictive periods. The real return difference is even higher, as inflation was significantly higher in restrictive versus expansive periods. The real return to stocks was 13.8% in expansive periods and only 1.7% in restrictive periods. Clearly, the empirical evidence suggests that the debate between those suggesting rate hikes are good for stocks versus those arguing that rate hikes are bad for stocks is not a fair fight.

Monetary conditions and style investing

Many advisors don’t invest in broad indices but adopt investment styles to suit client goals and objectives. Some prefer to invest in small firms while others opt for value or growth styles. We found there were significant monetary policy related return patterns to different investment styles.

The small-firm effect

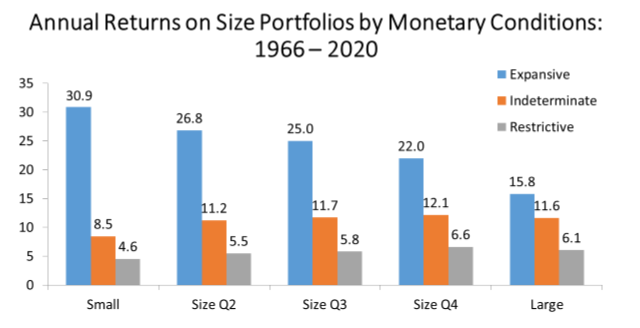

It is well-documented that over the long-term, small firms have experienced higher returns than large firms. Data published by Duff & Phelps shows that from 1926 through 2020, small-capitalization stocks returned 11.9% annually versus 10.1% for large stocks. This return differential came at a price, however, as the annual standard deviation of small cap returns was 31.3% versus 19.7% for large-cap stocks.

When you look at the small-firm effect through the lens of monetary policy, you find that the outperformance of small firms was highly concentrated in expansive monetary policy periods. The chart below shows the returns by monetary environment of returns to stocks in different size quintiles. The small-stock quintile represents the 20% smallest stocks by market capitalization and the large quintile represents the 20% largest stocks.

The chart shows significant outperformance of small versus large stocks in expansive monetary policy periods, while large stocks outperformed small stocks in indeterminate and restrictive monetary periods.

The chart shows significant outperformance of small versus large stocks in expansive monetary policy periods, while large stocks outperformed small stocks in indeterminate and restrictive monetary periods.

Value versus growth

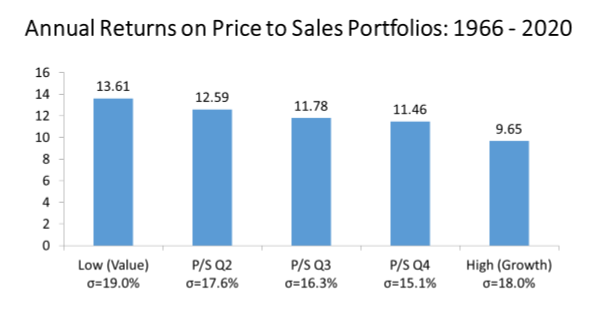

Advisors realize that there are many definitions of “value stocks”: Low price-to-earnings, low price-to-book, low price-to-cash flow, high dividend yield and low price-to-sales. A problem with studying returns to value versus growth stocks is that some of these measures are invalid for many firms. Specifically, all firms have a price, but many firms don’t have earnings, a positive book value, positive cash flow or pay dividends. One measure that can be utilized for all firms is price-to-sales. This is a blunt instrument, but there has been a strong relationship between price-to-sales and stock returns as evidenced by the chart below:

Stocks with low price-to-sales ratios (value stocks) outperformed stocks with high price-to-sales ratios (growth stocks) by a wide margin. And, that higher return came at only a slightly higher risk as measured by standard deviation. This suggests that investors have systematically overpaid for growth.

Stocks with low price-to-sales ratios (value stocks) outperformed stocks with high price-to-sales ratios (growth stocks) by a wide margin. And, that higher return came at only a slightly higher risk as measured by standard deviation. This suggests that investors have systematically overpaid for growth.

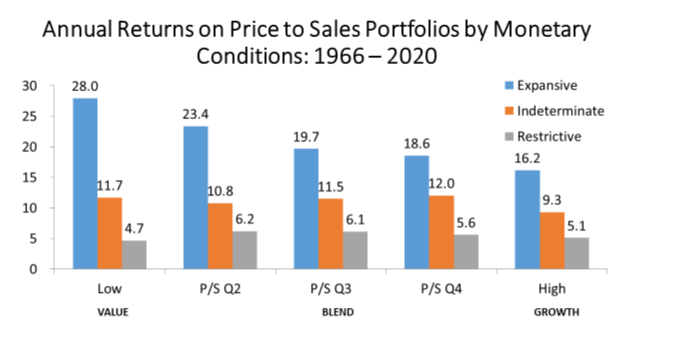

As one might expect, we also documented a systematic relationship between monetary policy and the return to value stocks (as measured by price-to-sales). Once again, you see that the value effect was concentrated in expansive monetary policy conditions, while there was no discernible value effect in restrictive monetary policy periods. And, counterintuitively, growth stocks slightly out-performed value stocks in times of tight money.

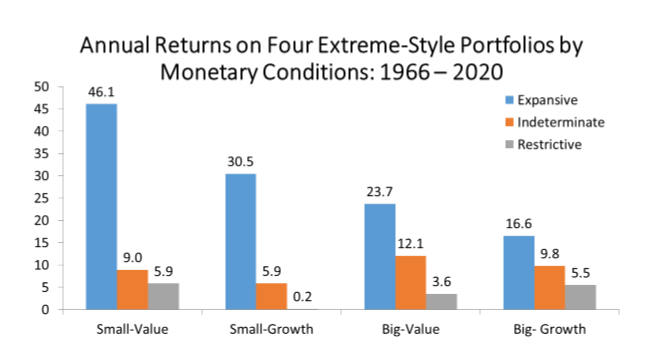

Combining size and value

Few advisors apply strategies of investing in large companies or only investing in growth stocks. Many employ strategies that are more refined and concentrate holdings in large-value stocks or small-growth companies. As the chart below shows, our research provides some interesting insights into the returns to multidimensional style strategies.

In expansive monetary environments, small-value stocks were the big winners. Returns were much more concentrated in indeterminate and restrictive monetary environments. Surprisingly, small-value stocks also had the highest returns in restrictive periods.

In expansive monetary environments, small-value stocks were the big winners. Returns were much more concentrated in indeterminate and restrictive monetary environments. Surprisingly, small-value stocks also had the highest returns in restrictive periods.

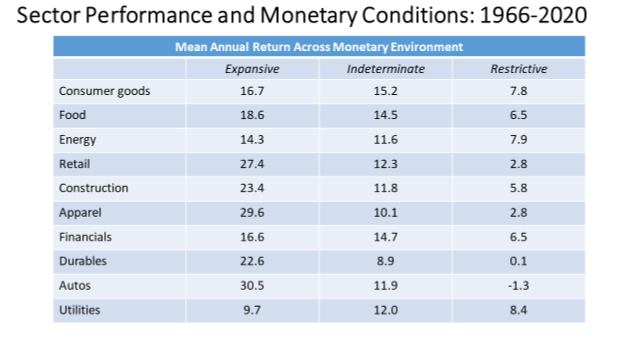

Is sector rotation the answer?

Many investors like to practice sector rotation when interest rates are changing. One of the mantras you often hear is that rates are rising, and you need to relocate to favor one sector and exit another sector. As seen below, the return to sectors varied dramatically across a sample of equity sectors.

Given that we are in a tight money environment, the research shows that it is wise to invest in defensive sectors whose firms are less dependent upon the business cycle. Food and beverages, household and personal care products, energy, and utilities are non cyclical or defensive in nature. People need to eat, brush their teeth, and heat their homes whether the economy is strong or weak. That doesn’t mean individuals won’t change their spending behavior. It is common for people to alter spending patterns within a sector; for instance, with a weaker economy they may shift from steak to hamburger or from shopping at Macy’s to shopping at Costco. And this exposes a weakness of sector rotation as not all firms that produce or sell non discretionary products are defensive to the same extent.

The bottom line on the Fed

One of the biggest findings of our research was that it is the direction in the movement of interest rates and not the level of interest rates that is highly associated with stock returns. Even though interest rates are still low by historical standards, equity prices respond to changes in interest rates and not the absolute level of rates.

You ignore the Fed at your own peril. To quote the late Marty Zweig, “Don’t fight the Fed.” Monitoring Federal Reserve monetary policy is essential for communicating with clients. If the Fed is pursuing a tight money policy, you may want to let clients know that over the near-term equity returns may be markedly lower. Conditioning client expectations during tight money environments may forestall some conversations on the reasons their portfolio value has stalled or is falling.

Robert R. Johnson, PhD, CFA, CAIA, is CEO and co-founder of Economic Index Associates, a NYC-based firm that creates investable indexes based upon Federal Reserve monetary policy. He is also a professor in the Heider College of Business at Creighton University. He was formerly president and CEO of The American College of Financial Services.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All