Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Popular opinion, as portrayed in the financial press, is that the Fed was way too late in responding to the threat of inflation. So, let’s turn back the statistics clock one year and review what was going on at that this time in 2021, just two months before the FOMC November announcement that it was going to end quantitative easing (QE) policies in late second quarter. This was also just three months before the FOMC’s December announcement that it was accelerating its plan to begin in late first quarter.

Let’s begin with a quick review of the two Fed mandates, in order of the importance that it uses to determine policy: First, and most importantly, is full employment, ideally around 4% unemployed. Second, and of somewhat less importance, is price stability, with inflation managed at approximately 2%. The Fed will address inflation if and only if the economy is strong enough to swallow the bitter pills required to tame inflation. Weak employment means a weak economy, and it would not force feed those pills. The Fed has the clear expectation that that dosage would cause more damage to employment, creating more economic weakness, than they would do good by bringing price inflation under control.

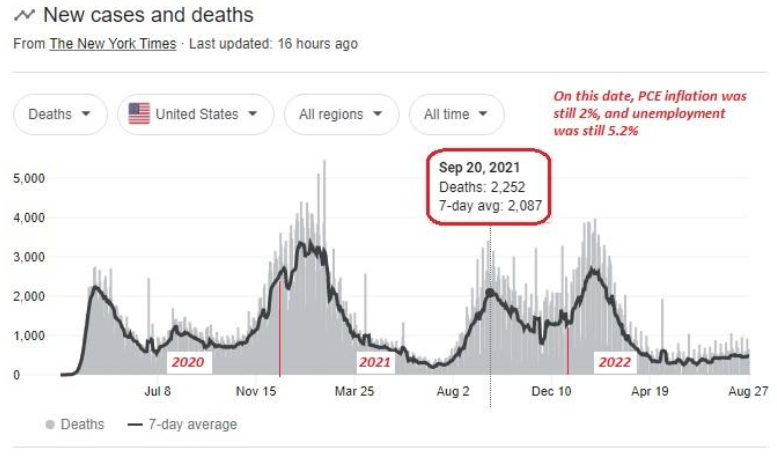

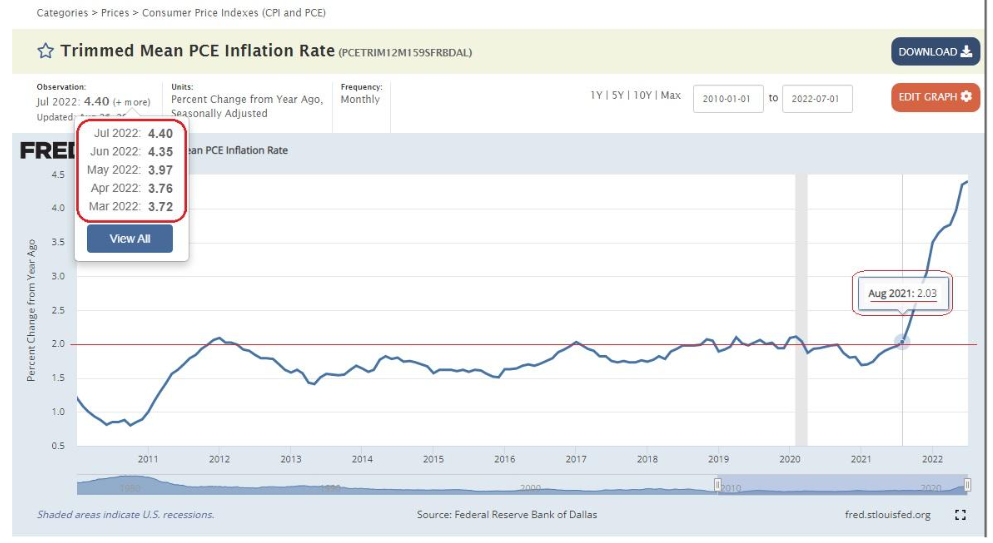

Let’s just look at what the Fed was dealing with in mid-September of 2021, with no clear vision of what would lay just ahead (see charts below):

- PCE inflation was still at 2%;

- Unemployment was still at 5.2%; and

- COVID-Delta was killing almost 15,000 Americans each week, with an increasing trend.

What do you think it should have prudently done, in the moment, to “address inflation”?

The only rational answer is: “nothing!”

The emotionally driven bashing of the Fed, which will soon reach widespread stridency, is unwarranted and unjustified. Near the end of the third quarter of last year, there was no way it could foresee subsequent events, including:

- Supply-chain bottlenecks;

- The next wave of COVID, Omicron, and its effects on U.S. labor supply and overseas supply chains; and

- Certainly not the energy shocks driven by Putin’s adventurism in Ukraine, which manifested itself in January and February 2022 (and into April), well after the Fed had already scripted and committed itself to its accelerated return to qualitative tightening (QT), set to begin in March of 2022.

The Fed is data-driven and tries not to prognosticate without being on solid grounds. Given that none of us can foresee unanticipated events, its rational approach is what we should now expect it to see through, hopefully engineering a resolution of minimal-to-moderate damage. Unemployment moving back above 4.5%, and trending towards 5%, will likely get it to moderate it QT approach, if inflation seems to be cooling down. We certainly are all hoping it won’t take a 9% Fed funds rate to make that happen. But a wavering of resoluteness and non-unanimity within the FOMC will surely do more long-term damage to oit effort. It seems to be realizing that, for now.

And yes, there will be other problems arising from this “solution,” such as greatly increased debt service costs to the U.S. Treasury. Most of the rest of the world with significant national debts will be facing similar issues, so the strength of the dollar will also help guide this QT process.

Richard Vesel is the founder of AdvancedProjections.com, where you can read more about this topic.

Read more articles by Rich Vesel

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The Fed is data-driven and tries not to prognosticate without being on solid grounds. Given that none of us can foresee

The Fed is data-driven and tries not to prognosticate without being on solid grounds. Given that none of us can foresee