The Destruction Wreaked by Ultra-Low Interest Rates

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits“I returned, and saw under the sun, that the race is not to the swift, nor the battle to the strong,

neither yet bread to the wise, nor yet riches to men of understanding,

nor yet favour to men of skill; but time and chance happeneth to them all.”

–Koheleth1

Super-bubbles in the asset markets, the rise of populism, and inequality are among a host of societal problems caused by low interest rates, according to Edward Chancellor. He explains why in his provocative new book, The Price of Time.

My favorite of the many brilliant verses in the wisdom books of the Old Testament frames the problem faced by finance. Finance, said Roger Ibbotson, is the branch of economics that deals with time and uncertainty. While finance appears extraordinarily complicated, when simplified to its barest essentials it relies on two prices: of risk and of time.

We see countless attempts to discern the price of risk all. The equity risk premium is the price of business risk – yet we can’t measure it, only give wide estimates. Insurance premiums measure the price of mortality, medical, and property risk. Betting markets can price just about any risk.

But what is the price of time? In what sense does time have a price? Why is it, of all these prices, the only one you can look up each day in the newspaper? (The price of time is the interest rate, in case you haven’t guessed by now.) And what can we learn from an intensive study of that price, across history and the extent of the globe?

Chancellor, one of the finest writers ever to turn his attention to financial markets, tackles both the deep history of interest rates and the controversies surrounding them in The Price of Time. If an investor were allowed to have only a dozen investment-related books, this would be one of them. The others would include Peter Bernstein’s Against the Gods, Matt Ridley’s The Rational Optimist, and Nassim Taleb’s Fooled by Randomness.2

You can finish the list. My list is biased toward history and long-term thinking, and I’m sure Chancellor’s list would be too.

This article mixes an assessment of The Price of Time with a more general inquiry about interest rates, their role in the economy, why they’re so low, and whether they should be higher (Chancellor says “yes”).

This article mixes an assessment of The Price of Time with a more general inquiry about interest rates, their role in the economy, why they’re so low, and whether they should be higher (Chancellor says “yes”).

Purpose and structure of the book

“This book,” Chancellor writes,

was...inspired by a Bastiat-like conviction that ultra-low interest rates were contributing to many of our current woes, whether the collapse of productivity growth, unaffordable housing, rising inequality, the loss of market competition or financial fragility. Ultra-low rates also seemed to play some role in the resurgence of populism as Sumner’s Forgotten Man started to lose patience.

(Frédéric Bastiat was a nineteenth-century French economist and legislator who championed Adam Smith’s free-market ideas on the Continent. William Graham Sumner, a 19th-century Yale professor, coined the phrase “the forgotten man” to refer to the party called “C” in a political – not market – transaction where A and B decide what C will give to D. Nice fellows, those A and B.)

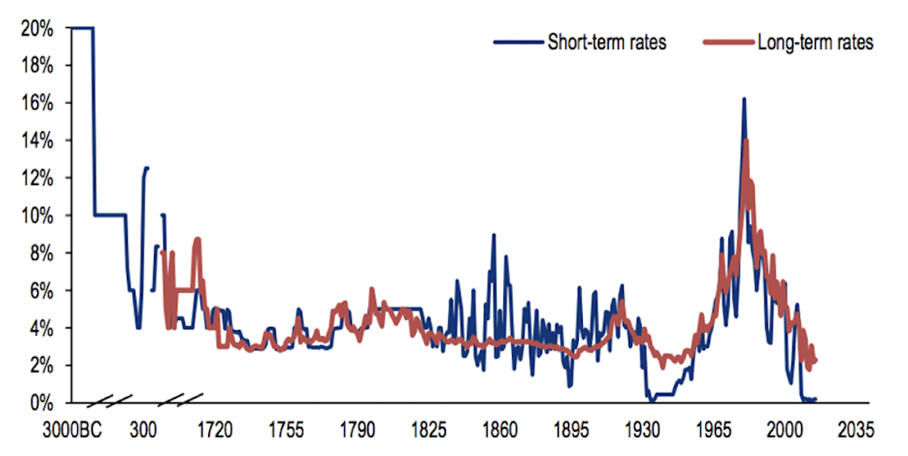

The Price of Time begins with a history of the interaction between interest rates and, well, everything else in the world. He writes, “We trace the origins of interest to the Ancient Near East...and follow its story through the Middle Ages to the birth of capitalism in Europe...” Exhibit 1 shows 5,000 years of interest rates on best credits (mostly sovereigns) – we really are experiencing the lowest rates in history! We describe how interest and capitalism are inseparable.”

Exhibit 1

5000 Years of Interest Rates

Source. Underlying sources: Bank of England; Global Financial Data; Homer, Sidney, and Richard Sylla, “A History of Interest Rates,” 4th ed., Hoboken, NJ: Wiley Finance.

Low interest rates have historically been observed in low-risk, mature societies and have thus usually been regarded as a good thing. The relationship flips around, however, when administered interest rates – in this case, achieved through the Fed’s open market operations – become so low as to discourage savings, promote wild speculation, and keep “zombie” enterprises alive that should die as part of the process that Joseph Schumpeter called “creative destruction.”

Part two explores these latter themes. Chancellor writes,

[W]e examine in greater detail [Claudio] Borio’s thesis that “low rates beget lower rates.” These chapters are arranged around the various functions of interest, namely its influence on the allocation of capital, the financing of companies, the capitalization of wealth, the level of savings, the distribution of wealth, the measurement of risk and the regulation of international capital flows.3

It’s a rich pageant of macroeconomic thought, told from Chancellor’s contrarian, some might say Victorian, point of view.

Why this book is controversial

Much thinking, and almost all practice, in monetary economics is the exact opposite of Bastiat’s and Chancellor’s. Low interest rates are widely thought to be an unalloyed good. Keynesian economists, who are in charge of most of the world’s central banks, advocate lowering interest rates when the economy slows, because (they argue) low borrowing costs encourage investment, for example by making big purchases by consumers and businesses more affordable. In emergencies, interest rates could be lowered – by central-bank open-market operations, not by free-market forces –to zero and beyond.

The effectiveness of this approach is still being evaluated, but the basic concept has guided monetary policy since the end of World War II. Since the global financial crisis of 2007-2009, however, central bankers acted as if it is always an emergency. Earlier this year, Stephen Sexauer and I wrote,

When you’re a fireman, you benefit from an abundance of fires. When you’re a central banker, you are unseen doing the work that keeps our money and banking systems up and running, except in economic emergencies. In emergencies... you become a rock star... [T]his does not make for good policy.4

Chancellor picks up on the fire theme. The Fed has been accused of creating, using super-easy money, a series of asset bubbles that then had to be corrected through a policy of tight money. The resulting seesaw is disruptive and expensive (the S&P 500 declined 49% in 2000-2002 and an incredible 57% in 2007-2009, comprising a “lost decade”). Chancellor agrees with this critique of the Fed. Noting that firemen have been known to set fires to guarantee their importance, he writes, “[O]ne is drawn to James Grant’s conclusion that the Fed’s ‘functional dual mandate has become that of arsonist and fireman.’” Ouch.

The “fall” of 20085

In the fall of 2008, two things happened in the monetary system. Central banks became the lenders of last resort when the bank runs started to occur – they lent against good assets and made a tidy profit doing so. In the U.S., the Fed’s balance sheet went from about $900 billion to $2 trillion as it purchased the panic-driven avalanche of assets out of money market funds and investment banks. The Fed made about $100 billion per year doing this.6 Within two years, those additional $1 trillion in assets left Fed and went back into the financial markets.

Second, in an attempt to actively support the economic recovery, the Fed and central banks worldwide purchased trillions upon trillions of dollars in government bonds (called quantitative easing, QE) to push short-term interest rates down to zero in the United States and negative numbers in Europe and Japan –and kept them there for 10 of the last 13 years. As shown in Exhibit 1, nothing like this had ever happened before, except briefly in the 1930s, in the 5,000 years of history documented by Sidney Homer and Richard Sylla in their masterpiece, A History of Interest Rates, on which Chancellor and the rest of us rely for our long-term historical information.

Near the end of this extended period of ultra-low and negative administered rates, a strange new philosophy called “modern monetary theory” (MMT) by its proponents, and inflationism by its opponents, took hold. MMT held that a sovereign government was limited on the creation of debt in its attempt to boost its GDP only by the extent to which inflation would arise, and that rates would remain low. For a short while, that’s what happened: massive fiscal deficits, extraordinary levels of government spending, and what Fed Chair Jerome Powell called “stubbornly” low interest rates. But, even after the 2020-2021 COVID pandemic with its supply shocks and massive $5 trillion fiscal helicopter drop of serial relief programs, we didn’t get much inflation.

In 2022, that changed quickly and dramatically. Now we are in an inflationary spasm that is causing savers (especially retirees) to panic and causing economists to reconsider their Keynesian and MMT dogma.

Chancellor vs. Bernanke

I’ve gone through all this background to show that Chancellor’s hard-money advocacy, powerfully supported in the second section of The Price of Time, is deeply contrarian. It is a swim upstream in the spring floods. Nobody wants to hear that the monetary policies of the last two-plus decades were no good and could lead to our eventual ruin.

That is what Chancellor is saying – and he goes farther.

He argues that, in our modern history, interest rates kept too low by a sovereign have always led to chaos, and potentially economic collapse. Eventually market forces, risk, and the natural price of time win out. Chancellor, channeling Friedrich Hayek, calls this “the new Road to Serfdom.”7

The Economist reviewed Ben Bernanke’s 21st Century Monetary Policy as well as Chancellor’s volume. Never afraid of controversy, it stated that while Chancellor is by far the more elegant writer and better debater, he is wrong and Bernanke is right:8

Mr. Bernanke’s framework is more compelling than Mr. Chancellor’s, as low or even negative interest rates can co-exist with humanity’s natural short-termism. Suppose someone has a wage income of 100 in their working life and zero in retirement. Though they may not target a 50/50 split, they will save to avoid penury. Lots of people building up a nest-egg – even one that is small relative to their working incomes – creates an imbalance that can, as a result of market forces, push rates lower than their discount rates. “Justice is violated when lenders receive little or nothing,” Mr. Chancellor writes. He might as well rage against a population pyramid.

The Economist concluded by saying that “when the time comes to appoint a central banker, choose someone like Mr. Bernanke.”9

This debate is not new. In 1900, L. Frank Baum, in a best-selling book, lampooned authorities who claimed the ability to control everything and fix whatever’s broken in the economy. Exhibit 2 is a scene from a later dramatization of his book.

Exhibit 2

Skeptical citizens try not to be fooled by a pompous central banker

Yes, The Wizard of Oz was a political screed for adults as well as a wonderful drama and allegory for children.10

A stellar group of academics weighs in

I might dismiss The Economist’s comments (except the one about the population pyramid, which is very clever) with a wave of the hand, attributing them to that magazine’s incorrigible establishmentarianism. Given its self-image as the voice of reason and responsibility, how could it come to any other conclusion?

It turns out that the Economist’s view has support in surprising places. At the request of the CFA Institute Research Foundation, I recently convened an 11-participant, all-day discussion on the equity risk premium, soon to be published by that organization as a book.11 The topic turned to negative interest rates, and Jeremy Siegel, the author of Stocks for the Long Run and possessor of a notably sunny disposition about the markets, said:

An insurance asset, as you know, will very often give you a negative return... When everything is priced in money, and the concern is about another financial crisis or a pandemic...or whatever, prices of goods and services and real assets decline, and bonds – nominal fixed assets – do extremely well. They take on a sharply negative beta, which gives them a tremendous hedging ability. I think trillions of dollars’ worth of demand are generated to hold that asset.

When an asset faces massive, unexpected demand, and the supply is relatively fixed in the short run as with bonds, the price rises and the yield falls. Negative interest rates.

The conversation went further into the rabbit hole:

Rajnish Mehra: If there is a famine tomorrow – if times are good today and times are really bad tomorrow – then I would give up a lot of stuff today to get something guaranteed tomorrow in a very, very bad state of the world where the marginal utility is very high. Then I will get negative rates. But that’s not a world I want to live in.

Laurence Siegel: That’s a declining economy. You can get negative rates in equilibrium in a declining economy, but not in any other state… We got...positive real rates from thousands of years in the past until 13 years ago. Which is the rule and which is the exception?

Jeremy Siegel: You can get a negative risk-free rate of interest in a growing economy. I’m not saying that it will happen. But it can be an equilibrium in a growing economy.

Roger Ibbotson: I agree with Jeremy because most of your investments involve risk and have positive payoffs. It is just the risk-free rates – the real risk-free rates – that are negative. I don’t see any reason why they couldn’t continue ... indefinitely.

When two of the three most distinguished finance professors in the world say that you can have negative real interest rates in equilibrium in a growing economy, we have to listen. (“In equilibrium” means that the negative real rate is a market-derived rate, a fair price for time, not a mistake imposed by authorities.)

A more immediate concern: Government budgets and nominal debt service

Governments and other economic agents owe a lot of money. All debt is floating-rate in the long run (because even the longest bonds mature and the issuer has to roll them over at the new rate). So, while higher interest rates might be desirable from a growth point of view, you can’t raise rates so much that they would bankrupt the government.12

Moreover, such a high rate will produce a large negative real rate if inflation continues at its current 9% pace! Clearly. we are constrained by the size of government debt. (Debt hawks, including Chancellor, have seen this coming for a long time.)

The Grumpy Economist gets the last word

Chancellor is not the only economist who thinks interest rates are too low to be consistent with robust growth. In his blog, “The Grumpy Economist,” John Cochrane, an impeccably pedigreed macroeconomist and financial economist who has written authoritative books on asset pricing and the fiscal theory of the price level, stated

All current macroeconomic theories start with the same basic story: when interest rates are higher, people consume less today, save, and then consume more in the future. Higher real interest rates mean higher consumption growth.13

For those who care about the future beyond the next few quarters, higher real interest rates are good. Rather than trying to maximize current consumption or production, as measured by quarterly GDP data, we should be trying to maximize wealth, which is (by simple accounting identities) the present value of all future consumption.

Too much doom and gloom?

Like any scholar of markets, Chancellor does not get everything right. For more than a decade he was an investment strategist with Jeremy Grantham’s prestigious asset management firm, GMO, and he’s been influenced by Grantham’s thinking (which is often a good thing – but not always). He approvingly quotes Grantham as having said, in 2011, that the “days of abundant resources and falling [real] prices [of natural resources] are over forever.”14

The CRB commodity price index responded by promptly falling in half, from 320 at the 2011 top to 162 at the 2016 bottom. More recently, commodities soared because of the COVID crisis and concomitant monetary stimulus but, notably, did not surpass the 2011 high – and, just this summer, the bellwether gasoline and copper prices plunged. Forever is a long time, and the long-term trend of real raw materials prices has been down.15

I’m as concerned about the impact of low interest rates and an unremitting easy-money policy as anyone. But the real economy has a way of shaking off burdens like these – in the horrific 1930s, real U.S. GDP grew 1% a year; in the stagflationary 1970s, an impressive 3.2% per year. We are in trouble but not enough to justify some of Chancellor’s chapter titles, which have a National Lampoon tinge: “A Big Fat Ugly Bubble,” “Your Mother Needs to Die” (about unfunded pension liabilities and inadequate retirement savings), and the clear winner – “The Mother and Father of All Evil” (rising interest rates according to Recep Tayyip Erdoğan). While Chancellor’s intent is to amuse, his underlying thoughts are serious.

The Price of Time is brilliant and provocative, but it’s just too one-sided – too much like the insightful but usually wrong doomsday forecasts that have peppered the financial pages since the pronouncements of Henry “Dr. Doom” Kaufman’s in the 1970s, David “Rosie” Rosenberg more recently, and Marc Faber all the time. Over the period Chancellor has been participating in markets – about 30 years, so let’s use 1990 as the starting date:

- Global real GDP has doubled (from $38 trillion to $80 trillion);16

- The percentage of the world’s population living in extreme poverty as defined by the World Bank has fallen from 36% to 9%; and

- The real (inflation-adjusted) S&P 500 with dividends is up 425%, or 5.2% per year.

There’s a species of Wall Street pundit known as the permabear.17 You know you’ve encountered one when they say, no matter when you ask them, that this is the moment that these favorable trends will turn around and run the other way forever.18

But the downdrafts never last forever. Chancellor should have been more careful not to sound the permabear alarm, because the information he presents does not justify it.

Conclusion

“...[I]nterest is a fundamental part of human society, a bridge between the present and the future,” wrote Kevin Coldiron, a Forbes columnist and retired fund manager.19 He continued,

Given the long list of potentially negative effects [of zero or negative rates] documented by Chancellor, prudence suggests we should avoid setting rates at [those levels], lest that bridge be weakened or washed away. After all, as Chancellor says in his book – capital consists of a stream of future income discounted to its present value using interest rates.

Let’s dig a little deeper. Interest is the way we balance the claims of the future against those of the present, an important task if ever there was one. The future is long (it might as well be infinitely long) and it has become fashionable to talk about what we, in the present, owe to the future including the very distant future.20 To begin to solve that riddle, we need a link between the present and the future. That function has been served by interest rates, which do double duty as discount rates, for some 5,000 years. If that link becomes corrupted through bad policy or for other reasons, as it has periodically in the past, we won’t be able to do much to help future generations. We will become focused only on our own welfare, and that’s not good.

“Without [positive real] interest, therefore, there can be no capital,” continues Coldiron. “Without capital, no capitalism.”

And we need capital and capitalism. Lots of it. For a long time to come.

Laurence B. Siegel is the Gary P. Brinson Director of Research at the CFA Institute Research Foundation, the author of Fewer, Richer, Greener: Prospects for Humanity in an Age of Abundance, and an independent consultant. His latest book, Unknown Knowns: On Economics, Investing, Progress, and Folly, contains many articles previously published in Advisor Perspectives and/or distributed by AJO Vista. He may be reached at [email protected]. His website is http://www.larrysiegel.org.

![]()

The author thanks Stephen C. Sexauer, CIO of the San Diego County Employees Retirement Association, and Kevin Coldiron, lecturer in finance at the University of California, Berkeley, Haas School of Business, for their helpful comments and assistance.

1Ecclesiastes 9:11, King James Version (1611). Koheleth means “the preacher” or “the teacher” and that is all we know of the identity of the author of Ecclesiastes (which is itself a rough Greek translation of the Hebrew word Koheleth). The Wisdom books were traditionally thought to be written by King Solomon, but probably were not.

2The Price of Time might not make my top 4, but only because of the narrowness of its subject matter. It’s as well written as the other three I mentioned. Bernstein’s Capital Ideas and Capital Ideas Evolving are more directly relevant to the practice of investment management, but Against the Gods (about risk) should be required reading for anyone who takes risk – and that’s all of us. Taleb’s book, likewise, should be required reading for anyone who deals with statistics and numbers – again, that’s all of us.

3Emphasis in the original. Borio is head of the Monetary and Economic Department of the Bank for International Settlements (Basel, Switzerland).

4Siegel, Laurence B., and Stephen C. Sexauer. 2022. “Debunking 7-1/2 Myths of Investing.” Journal of Investing, 30th Anniversary Special Issue, p. 97.

5Thanks to Edwin Burton (University of Virginia) for this inexcusable pun. The Fall of 2008 is the title of his book on the topic.

6The Fed followed closely, but not exactly, Walter Bagehot’s famous 1873 recommendation, summarized by Paul Tucker, for central banks to “to...lend early and freely (i.e., without limit), to solvent firms, against good collateral, and at ‘high rates’” to stave off financial panics. What the Fed did not do was to lend at high rates. (Bagehot was the editor of The Economist and a popular writer on finance; the recommendation is in his Lombard Street: A Description of the Money Market. Sir Paul Tucker is a British central banker.)

7Chancellor is referring to Hayek, Friedrich. 1944. The Road to Serfdom. Abingdon, UK: Routledge Press.

8“Bernanke v Chancellor,” The Economist, August 13, 2022.

9The case for low rates deserves a hearing too, but space constraints require me to punt. The references in this footnote will help. Although it’s a dull read, Bernanke’s 21st Century Monetary Policy is the go-to-source, the author having shepherded us through the most difficult economic circumstances in at least 40 years. Subsequent growth has been seriously subpar, which some blame on central bank policy, but that is not a satisfying explanation; other forces are at work. Tom Coleman’s and my summary of the case for low rates is in Siegel and Coleman (2015), pp. 6-7, https://larrysiegeldotorg.files.wordpress.com/2015/10/siegel_coleman_phooey-on-financial-repression.pdf.

10See https://en.wikipedia.org/wiki/Political_interpretations_of_The_Wonderful_Wizard_of_Oz, accessed on August 29, 2022.

11The book, Equity Risk Premium Forum, will soon be available online and in print at https://www.cfainstitute.org/en/research/foundation/publications. The participants were Rob Arnott, Cliff Asness, Mary Ida Compton, Elroy Dimson, Will Goetzmann, Roger Ibbotson, Antti Ilmanen, Marty Leibowitz, Rajnish Mehra, Tom Philips, and Jeremy Siegel. I was the organizer and moderator, and I will be co-editor (with Paul McCaffrey) of the book. Portions of the discussion are available at this time at https://blogs.cfainstitute.org/investor/tag/equity-risk-premium/; explore the blog back through time to read all the parts. The first blog post based this event was on April 8, 2022.

12https://www.atlantafed.org/cqer/research/taylor-rule?panel=1, “Alternative 1” default assumptions as of August 26, 2022. There is an extensive literature on this which I won’t get into, but it suffices to say that the Taylor-rule Fed funds rate of 6.83%, using the Atlanta Fed’s Taylor Rule calculator and its own default assumptions, is too high given the fiscal status of the U.S. government.

13“Three views of consumption and the slow economy,” blog post on Sunday, February 3, 2013, The Grumpy Economist, https://johnhcochrane.blogspot.com/2013/02/three-views-of-consumption-and-slow.html.

14Grantham, R. Jeremy. 2011. “Time to wake up: Days of abundant resources and falling prices are over forever.” Resilience, April 29, https://www.resilience.org/stories/2011-04-29/time-wake-days-abundant-resources-and-falling-prices-are-over-forever/.

15In January 2022, in “Generational Differences Are Less Important Than You Think,” https://larrysiegel.org/generational-differences-are-less-important-than-you-think/, I wrote, “the Thomson Reuters/CoreCommodity CRB Index, a reflection of resource scarcity, has been falling since 2008 and (linking indices) is lower in real terms than it was in 1913.” See https://www.jstor.org/stable/3872481 for the data. I have not updated the estimate to reflect the recent rise in that index.

16Global real GDP per capita has grown more slowly because the world’s population has increased.

17I was tempted to finger Chancellor’s former employer, Jeremy Grantham, as yet another permabear but he is way too nice and a personal friend, so I won’t call names. Grantham also points out that he got one very important market call right: small-cap stocks beat large caps by a massive amount from 1974 to 1982 (but 1974 was a long time ago).

18Faced with all the positive outcomes I enumerated, a determine permabear will say that those are the cause of the future negative outcomes he’s predicting. There is, of course, a possibility that that is correct.

19Coldiron now teaches at Haas Business School of UC Berkeley. We worked together when I was a consultant to Barclays Global Investors.

20See Cowen, Tyler M. 2018. Stubborn Attachments: A Vision for a Society of Free, Prosperous, and Responsible Individuals. South San Francisco, CA: Stripe Press; and MacAskill, William. 2022. What We Owe The Future. New York: Basic Books. The latter has been described as the most highly publicized-in-advance philosophy book of all time.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits