Michael McAleer and Jack Van Dyke are investment consultants for personalized solutions in Russell Investments’ advisor and intermediary solutions business. Mike and Jack are responsible for promotion and distribution efforts on the East and West Coast, respectively, of Russell Investments’ Personalized Managed Accounts (PMA) program, a suite of advisor-sold customized separately managed accounts (SMAs).

Michael McAleer and Jack Van Dyke are investment consultants for personalized solutions in Russell Investments’ advisor and intermediary solutions business. Mike and Jack are responsible for promotion and distribution efforts on the East and West Coast, respectively, of Russell Investments’ Personalized Managed Accounts (PMA) program, a suite of advisor-sold customized separately managed accounts (SMAs).

I spoke to Mike and Jack on September 9, 2022.

Russell Investments introduced PMA in 2021. Why did you enter this space?

Mike: Investors increasingly want more control and customization of their portfolios. Just as coffee drinkers appreciate having a choice of beans, sweeteners, flavors and intensity to suit their tastes, investors are looking for ways to express their preferences in their portfolios. Our PMA program gives them the opportunity to do that.

With five decades of experience providing institutional investment solutions, along with our industry-leading manager research and tax-management capabilities, Russell Investments was poised to create a suite of complementary PMA solutions. These customizable SMAs help our partners and advisors offer their clients a customized way to meet desired outcomes.

Our PMA program gives advisors and their clients access to an investing approach that leverages Russell Investments’ extensive investment manager research, selection and monitoring process. This process is our trademark, forming the cornerstone of our advice to global institutional investors for more than 50 years.

Our PMA program leverages the best that Russell Investments has to offer. It features a dedicated team of portfolio managers, quantitative research analysts and service teams, centralized trading and implementation, as well as automated year-round tax management capabilities, including tax-loss harvesting, wash-sale minimization, tax-smart turnover and holding-period management. Ultimately, these customized SMAs will help clients meet their desired outcomes by minimizing the impact of taxes and transaction costs while maintaining tracking error to a target portfolio. We leverage technology to help investors achieve growth and optimal after-tax outcomes.

The program is a distinctive suite of solutions for financial advisors and their clients that can be customized to each investor’s unique and specific needs.

Your firm recently added two direct indexed options for an expanded suite of eight SMAs. Can you talk a little bit about what you are now offering?

Mike: Yes! We’re excited about the recent expansion of our PMA program to add exposure to international and core equity.

Our PMA program now features:

- Two personalized core equity SMA solutions: Core Equity and Direct Indexed Core Equity (new)

- Three personalized active SMA strategies: Large Cap, Small/Mid Cap, and International

- Three personalized passive SMA strategies: Direct Indexed Large Cap, Direct Indexed All Cap, and Direct Indexed International (new)

In addition to Russell Investments' offering of three active SMAs and three direct indexing SMAs within our PMA structure, we also offer two core-equity solutions. One is a combination of active and direct indexed strategies. Another combines two direct indexed strategies into a single SMA. The benefit of these single-sleeve portfolios is that an investor can purchase a single strategy and then pair it with other asset classes such as fixed income to round out their risk profile.

We like to describe PMA as a supercharged SMA: It provides for direct ownership of securities, allowing investors to choose individualized portfolios, while also adding custom overlay, exclusion services (such as tax-managed overlay services and values-based exclusions and overlay options) and personalized transition management.

Because of the flexibility of these solutions and the scalability that makes them available to a larger portion of the investing population, we believe advisors will find these products could be a good fit for a broad range of client types and circumstances.

How does PMA allow you to customize the investor experience?

Jack: Every investor’s needs and preferences are unique. As an investor’s wealth grows, so do their expectations and the complexity of their investments. The level of personalization and customization required to meet each client’s distinct goals can quickly send a practice into disarray. This is where PMA comes in.

Our PMA solutions allow significant customization to help mitigate some of an investor’s major concerns:

Tax management. We find the most common issue investors are looking to solve is managing the tax liability associated with their investment portfolio. We have a heritage in this space with a range of mutual funds that focus on maximizing after-tax returns, and we continue to see growing interest in tax management. Recent market volatility, along with potential changes coming out of Washington, DC, have led many investors to think more about the tax implications of their investments than they have in the past.

Whether an active or passive strategy, using a tax overlay in making trading decisions allows a manager to potentially reduce the tax burden of a portfolio and improve after-tax outcomes. Taking into account tax-lot details, purchase dates and costs, which are unique to each individual investor, is critical for effective tax management.

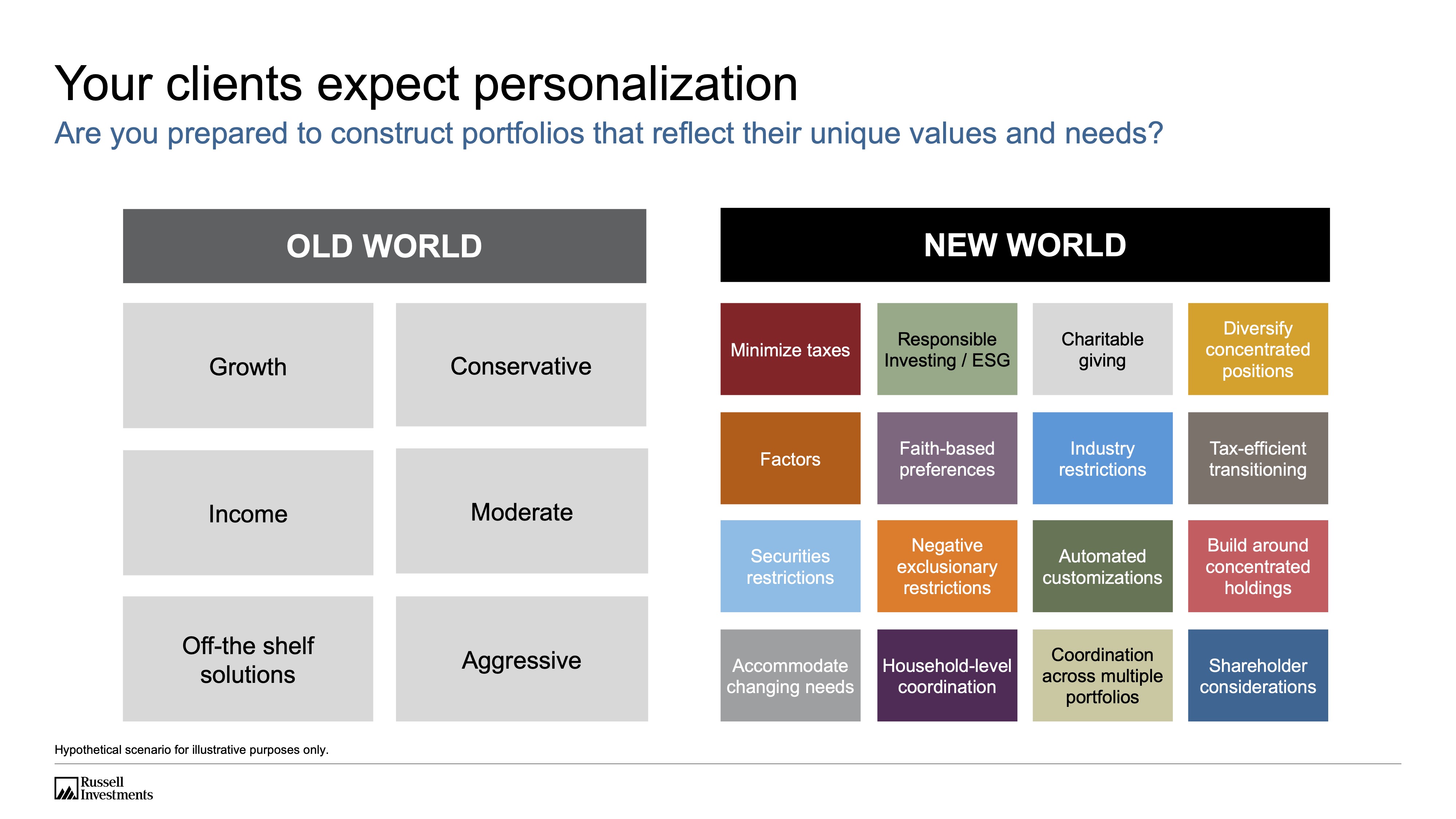

Values-based exclusions. Many clients want or need a level of customization that mutual funds can’t offer. They may want to embrace a preference screen such as environmental, social and governance (ESG) criteria or socially responsible investing (SRI). Or their need could be as simple as an exclusionary restriction of a single security for a whole host of reasons.

PMA can offer a wide-ranging set of exclusions that provide customization options to ensure an investor’s portfolio is aligned with their personal set of values or preferences.

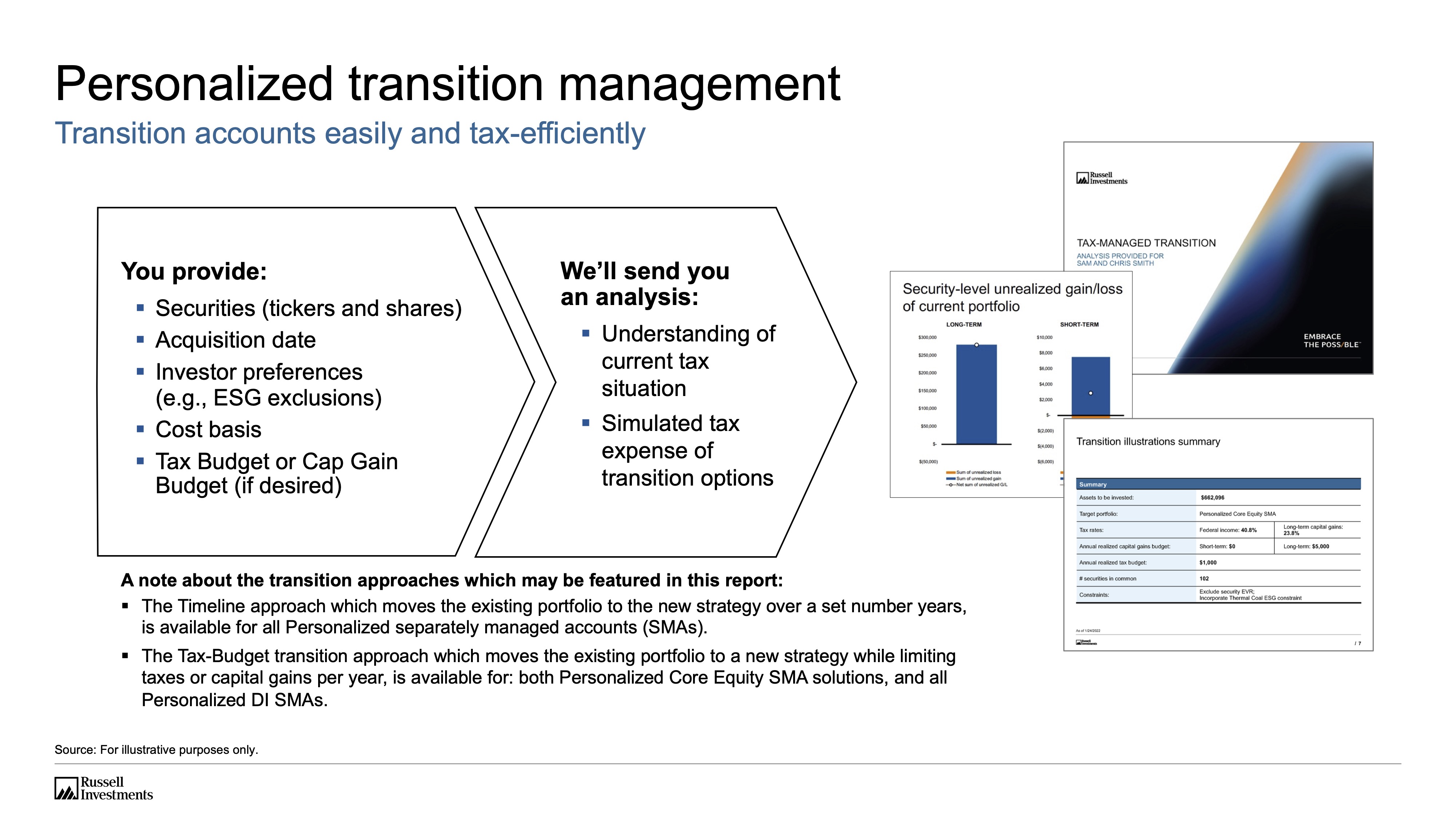

Optimal transition planning. Transitioning to a target portfolio is not as easy as simply selling legacy holdings and buying new holdings—especially when taxes are a consideration. Careful transition planning can help investors move assets between strategies while minimizing the resulting tax liability. An immediate transition, such as selling all legacy holdings while buying a new portfolio, can often leave an investor saddled with heavy tax liabilities and worse off on an after-tax basis. By designing a transition plan to move between strategies over a set number of years or with a specific tax budget in mind, an investor can have a better after-tax outcome over the course of the transition. This is critical as it avoids the counterproductive exercise of paying taxes to move into a tax-managed solution.

Diversifying concentrated stock positions. More than ever, employees are being compensated in company equity and are looking to diversify their entire portfolio, not just a single sleeve of it. It is common for executives or long-term employees to have stock positions from their employers, received as stock options or grants over the years. Often these positions will have a low-cost basis and represent concentrated holdings based on the size of the overall portfolio. PMA can provide options to customize an investor's portfolio, by selling in a tax-friendly manner and avoiding adding holdings in similar companies. This helps balance the portfolio’s overall risk and after-tax return.

Restricting stock positions. Individual investors can also elect to restrict purchases or holdings in individual stocks or industries. An investor may have various reasons for restricting certain investments: they may have similar large holdings in other portfolios, restrictions from purchasing stock of a company they work for or of a competitor firm, or individual preferences they want expressed in their portfolio.

How do these exclusions and restrictions due to personal values or other concerns impact investment outcomes?

Jack: As specific companies get removed from the target portfolio due to values-based exclusions, an account's performance will be affected. This is the outcome our clients would expect. As an example, if an investor chooses not to invest in tobacco stocks and tobacco companies underperform the benchmark, our client outcomes will be better off by having eliminated that exposure from the portfolio.

The ability to tax-manage a portfolio still exists in the presence of values-based or other restrictions. Except for any initial liquidations, an investor should not anticipate a material change to their tax liabilities if they choose to include an account restriction. In some cases, such as wanting to support green energy, many investors see increased investment risk associated with high carbon emissions or with companies involved in other controversial industries. Their expectation when adding restrictions to these industries is that these risks will be removed.

A separately managed account offers direct ownership of securities. What are the benefits of direct ownership?

Jack: The largest benefit from direct ownership is that you own the tax gains or losses generated from those securities. This allows you to determine when to take taxable income or harvest losses as opposed to being beholden to when the mutual fund manager decides.

In a commingled fund, everything is shared across all investors: Fees, tax liabilities, investment risks. In many ways, this can be a good thing, as economies of scale enable individual investors to access high-quality investment solutions. Commingled funds limit any personalized investment objectives.

Let’s take tax liability as an example. In a mutual fund, any capital gains realized throughout the year are aggregated into a taxable distribution at the end of the year, regardless of whether those gains were generated through rebalancing or trading due to the redemption activity of other investors. In this scenario, an individual investor may owe taxes as a result of trading decisions that may have been made without their individual investment situation in mind.

In direct-share ownership, by contrast, taxes at the end of the year are based on the trades made directly in the individual’s account: All securities bought and sold can be optimized to the investor’s unique situation.

Mike: In the past, if you wanted to exclude certain securities for whatever reason, there was no option to do so using mutual funds or ETFs. You had to find a product that came as close as possible to suiting your needs. This also led to more complexity for advisors as they had to determine which products best suited their clients. Therefore, advisors would ask prospects or clients questions such as, “Are you looking for growth?” or, “Are you looking for income?” or, “What is your risk tolerance?” The questions generally had to stop there.

With direct ownership, the questions are more like: “What industry do you work in—so that I know which areas of the market you already have exposure to? Do you have equity in your company we should build around? Do you have beliefs, either faith-based or strong personal preferences, that may lean you toward or away from specific types of companies or industries that I should be mindful of while designing and constructing a portfolio for you?” These questions bring a much more personal feel to investing. Direct ownership can allow for these circumstances and preferences, in addition to positioning for the traditional growth, income, and risk-tolerance questions. Additionally, advisors can also utilize the same product for multiple clients with differing needs – making their job easier.

Individual investors today have a wide range of direct ownership investment solutions to choose from, including concentrated, active strategies that might buy dozens of stocks, or diversified, passive strategies that will buy several hundred individual stocks.

Russell Investments supports active management. Yet in your PMA program you’ve expanded the passive direct indexing SMAs. Why?

Jack: Active management and direct Indexing each have their own benefits and objectives and can complement each other. The objective of the active strategies within PMAs is to outperform a respective index, after-tax. The role of the direct indexing strategies is to track a specified index while providing net losses that can be used to offset gains in another part of a client’s overall portfolio. This is possible because indexes generally have no or very little turnover.

In contrast, with active management, turnover is inevitable. Money managers buy and sell securities to take advantage of market mispricing. When there is turnover in a portfolio, gains and losses are realized; even when those gains and losses are managed to limit taxes, it can be challenging to eliminate all taxes, particularly in strong bull markets. Having both direct indexing and active strategies gives advisors optionality for different client needs.

Given their complementary characteristics, an optimal approach is to combine direct indexing with active management in a single portfolio. This provides the most efficient tax vehicle. Residual gains from the active strategy can be offset with losses from direct indexing, while allowing the investor to choose the desired asset allocation for the developed equity portion of their portfolio. Everyone’s situation is different, so advisors and clients need to find what works best for their goals, circumstances and preferences. This is what our PMA solution is designed to facilitate.

This is a different approach from most other firms in the SMA space, which generally utilize passive vehicles. What are the advantages of active management in this space?

Jack: There are several potential benefits an investor can expect from an active SMA relative to passive. For starters, active strategies will typically hold fewer names than passive strategies, which allows for lower account minimums. For investors looking to create a diversified total portfolio, which can include international and small-cap components, a lower minimum for each asset class helps those investors without multi-million-dollar portfolios still achieve an optimal asset allocation using direct-ownership strategies. Additionally, by leveraging stock selection insights from some of the best institutional money managers in the asset management industry, as Russell Investments does, active SMAs provide the opportunity to outperform a passive alternative over time through skillful stock selection.

When realigning a client’s taxable portfolio to a new investment strategy, many advisors are concerned about the tax cost to switch. How does Russell Investments address this?

Mike: There are several transition options available to advisors and clients. We have a team of analysts who can run robust, individualized scenario analyses to help advisors and their clients understand the pros and cons of each option.

One is a tax-budget approach where the client indicates a tax or capital gain threshold they are willing to take on, including zero. Then there is a timeline-based transition, where clients can select to move the portfolio to the target portfolio over a three- or five-year period to spread out and hopefully limit the taxes incurred. The trade-offs are control of timing versus control of taxes. Individuals who select the budget approach have complete control of taxes, but the time it takes to transition is very market-dependent. The people who select the timeline-based approach have control over how long it takes to get into their targeted portfolio, but the taxes incurred are market-dependent. In both cases, we do our best to work within the parameters we have to bring about the best tax and timing outcome we can for the investor.

Russell Investments has numerous tools to run a scenario analysis that considers actual holdings and any unrealized gain or loss in a client’s portfolio. An advisor simply sends over a list of holdings along with the original purchase date and cost basis. Russell Investments will take care of the rest. We build different transition scenarios across time horizons and with fixed-tax budgets, providing a summary back to the advisor. The advisor will see what tax impact each scenario would incur over time, along with the estimated tracking error from the target portfolio. The transition analysis outcome has proven useful to help advisors guide their clients to make informed decisions, with clarity into the tax and tracking error impact from moving between investment strategies.

Lastly, what differentiates Russell Investments’ PMA from its peers?

Mike: Our PMA program provides advisors with the ability to deliver customized portfolios that are unique to each client and at an attractive, all-inclusive price. As new overlays and customization options are introduced, they’re included at no additional cost.

This provides advisors and their clients with the flexibility to tailor each solution to their individual needs. That could include:

- Maximizing after-tax wealth

- Aligning values-based preferences with investments

- Diversifying a concentrated stock position

- Limiting purchases in stocks or industries already owned

- Developing an optimal tax-efficient transition plan

In addition, Russell Investments has been honored to receive the 2022 WealthManagement.com Industry Award (the “Wealthies”). The Personalized Managed Accounts program was selected as the winner in the Separate Accounts category. According to WealthManagement.com, a panel of independent judges made up of top names in the industry chose the winners of this year’s Industry awards, which recognize those firms and individuals who are bringing innovations to market that make a real difference to the daily activities of financial advisors.

In closing, mutual funds are an acceptable option for most investors who don’t need tax management or customization. But tax-managed mutual funds step it up for investors with non-qualified assets where taxes are an important consideration. SMAs can be a great option for many investors with specific needs. With PMA, advisors can offer investors a higher level of customization and comprehensive tax management, while also targeting a specific outcome.

Robert Huebscher is the founder and CEO of Advisor Perspectives.