Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

A new wave of lawsuits alleges that Blackrock’s target-date funds (TDFs) have underperformed. These lawsuits open the door to a related and scandalous breach of fiduciary duty – excessive risk. Just as excessive fees were ubiquitous, so too is excessive risk in TDFs. It is manifesting as excessive losses, a harm last seen in 2008.

The retirement industry is abuzz about a new batch of lawsuits against plans that use Blackrock TDFs. Miller Shah LLP, representing the plaintiffs in a class-action suit, has charged a host of plan sponsors with breaching their fiduciary responsibilities by making low fees their sole selection criterion, regardless of performance and other considerations.

It alleges that Blackrock’s TDFs have underperformed, and that fiduciaries weren’t properly or adequately monitoring the accounts containing those funds. The low-fee requirement is ubiquitous because many plan sponsors have lost lawsuits for paying excessive fees.

The courts will decide the merits of these new lawsuits. The important consequence is that a new door has been opened for TDF lawsuits, a door that can and should address a serious crime, in the same manner that lawsuits successfully corrected excessive fees.

This new door is excessive risk. Most TDFs are taking excessive risk near their target-dates.

Underperformance in TDFs

The excessive-fees door had been the only one open for TDF lawsuits. This new door swings open performance-related lawsuits. Until now, low-risk TDFs underperformed, but that pendulum is swinging to high-risk funds underperforming with losses that exceed safer funds.

The difference now is that excessive risk is becoming painfully obvious. Excessive risk was rewarded until now, but that doesn’t make it right. The duty of care for a fiduciary is that they are responsible for harm to beneficiaries that should have been avoided. It’s like our duty to protect our young children, covering electrical outlets and installing cabinet latches.

Defaulted beneficiaries deserve and want to be protected as they near retirement.

Excessive risk redux

This isn’t the first time we’ve observed the excessive risk breach of the duty of care. In 2008, TDFs for those near retirement lost more than 30%, and it created a public outcry that should have brought lawsuits but did not. I wrote about the potential for lawsuits in target-date Fund 'Safe Harbors' Attract A Minefield Of Possible Litigation

At that time, I interviewed Tess Ferrara, a prominent ERISA attorney and asked her why there were no lawsuits, to which he replied:

Regarding fund companies: “Mutual funds are protected by a very narrow statute of limitations and those cases had to be filed back in 2009, no later than early 2010 to make it through…since no one had the right data to present to the teams who could afford to take this on effectively at that time, they were not filed and the mutual fund providers escaped the liability for their wrongdoing. We will need another 2008 to get them.”

Regarding plan fiduciaries: “Bottom line with fiduciaries, they believe any line of crap their providers tell them when it comes to DC plan monies. They simply do not vet these products effectively, some because they don’t know where to start, others because it’s not a priority. They should be sued for the adoption of the vehicles and could be successfully litigated against, but the apple is much smaller for the plan cases rather than the provider cases.”

This time is different because:

- The plaintiff’s bar is primed and ready to pursue wrongdoing. I am personally speaking to a few law firms about preparing for big losses in TDFs, possibly even bigger than 2008. The harm to beneficiaries could be disastrous.

- In 2008, TDFs held only $200 billion. Now there’s more than $3.5 trillion. The stakes are much higher.

- Our 78 million baby boomers were not in the risk zone in 2008. Most will spend this decade in the risk zone.

- TDF risk has increased, since 2008 because the performance horserace was being won by the riskiest. At one point, Fidelity proudly announced a risk increase to compete with the likes of T. Rowe Price.

- There are safety standards for TDFs that weren’t recognized in 2008, but are now, discussed below.

The new door has a safety standard

The new door for lawsuits is not underperformance per se. It’s excessive risk that is manifested in excessive investment losses. The definition of “excessive” can be found in surveys of beneficiaries and consultants. These surveys report that a loss of more than 10% by someone near retirement is excessive.

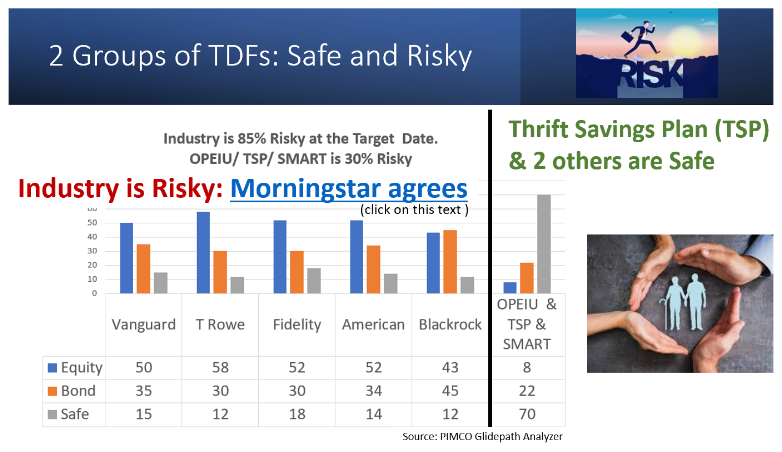

This new door requires a safety standard. Until now, Vanguard TDFs have been the standard, but a recent Congressional inquiry cited the Federal Thrift Savings Plan (TSP) as a better standard. The idea is that TDFs should be safe at the target-date. The TSP is only 30% in risky assets at the target-date, while the industry is 85% risky, as shown in the following.

Two types of TDFs: Safe and Risky

Most fiduciaries only know the risky group of TDFs and believe that they can’t all get sued, equating popularity with procedural prudence. But most fiduciaries paid excessive fees until lawsuits stopped that nonsense.

Substantive prudence triumphs.

The safe group of TDFs is small. The TSP is joined by the Office and Other Professional Employees International Union (OPEIU), one of the largest AFL-CIO unions, and the SMART target-date Fund Index (for which I serve as a paid consultant).

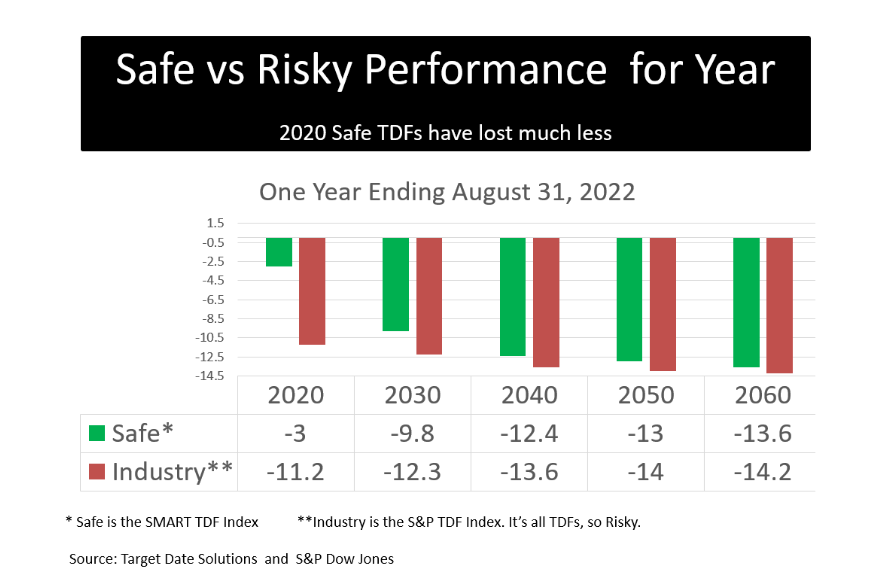

The following shows the recent performance of the two groups.

The industry (risky) had “excessive“ (below 10%) losses of 11.2% in its 2020 funds, versus losses of only 3% for the safe group.

Conclusion

There are good reasons to expect continuing deepening losses in stock and bond markets that will be felt most by those near retirement in TDFs. It will get worse.

The greater the harm, the greater the foul.

The door is open to correct this breach of the fiduciary duty and protect beneficiaries who default their investment decision to their employer. Most assets in TDFs are there by default. It is the most popular Qualified Default Investment Alternative (QDIA).

The plaintiff’s bar is watching. They will be the heroes in the next 2008-like debacle.

Ronald Surz is co-host of the Baby Boomer Investing Show and president of target-date Solutions and Age Sage, Target-Date Solutions serves institutional investors, namely 401(k) plans. Age Sage serves do-it-yourself individual investors.

His passion is helping his fellow baby boomers at this critical time in their lives when they are relying on their lifetime savings to support a retirement with dignity, so he wrote a book Baby Boomer Investing in the Perilous 2020s and he provides a financial educational curriculum.

Read more articles by Ron Surz

Read more articles by Ron Surz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives. The courts will decide the merits of these new lawsuits. The important consequence is that a new door has been opened for TDF lawsuits, a door that can and should address a serious crime, in the same manner that lawsuits successfully corrected excessive fees.

The courts will decide the merits of these new lawsuits. The important consequence is that a new door has been opened for TDF lawsuits, a door that can and should address a serious crime, in the same manner that lawsuits successfully corrected excessive fees.