This has been a very painful year in investing. Not only are stocks in a bear market but, instead of acting as a shock absorber, bonds are having their worst year ever. For bonds, this is the equivalent of the 88% stock plunge during the Great Depression.

This has been a very painful year in investing. Not only are stocks in a bear market but, instead of acting as a shock absorber, bonds are having their worst year ever. For bonds, this is the equivalent of the 88% stock plunge during the Great Depression.

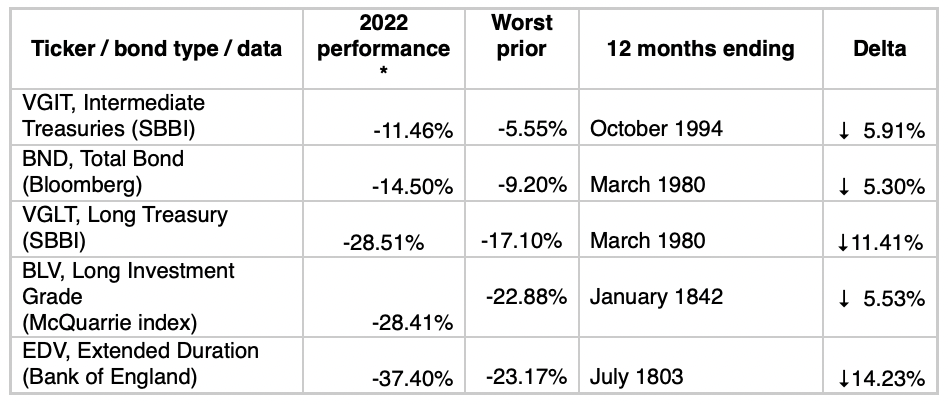

Below is a summary of bond performance from Edward F. McQuarrie, Professor Emeritus in the Leavey School of Business at Santa Clara University who has long researched the history of bonds.

*Values are for the first nine months. Trailing 12-month returns also exceeded the historical worst; in fact, for the two intermediate types (VGIT and BND) returns since 9/30/2021 were slightly worse than those shown.

But there are nuggets of good news:

1. Bonds are finally giving a real yield. Going into 2022, yields were dismal. You could earn 1.26% on a five-year Treasury bill. If you wanted some inflation protection, a five-year Treasury Inflation Protected Security (TIPS) yielded a negative 1.61% annually. Investors were guaranteed to lose spending power.

Perhaps the only silver lining in the bond market plunge is that rates are getting better. While nominal yields have surged, real yields on TIPS have gone from negative to positive. That five-year TIPS is now yielding a positive 1.56%. One can finally be assured of earning more than the CPI-U. That’s a good thing. TIPS are more attractive today than they have been in years.

As of October 10, 2022, the real yield on 30-year TIPS was 1.73%. That makes TIPS a viable solution for clients seeking to lock in 4% real withdrawals over a 30-year retirement. With minimal price volatility, a $1 million portfolio with 4% real withdrawals would leave a $90,000 bequest. Greater price volatility means that is not a “sure thing,” but it compares favorably to traditional portfolios of stocks and nominal bonds.

2. Ditch the dogs. Often, clients come to me with more expensive funds or individual stocks that I’d like to sell. But tax consequences may be more than the benefits of changing to better funds. Not only have the gains of those holdings been reduced, but clients likely have losses in other holdings they can use to offset those gains.

3. Tax-loss harvesting is an amazing opportunity. I tell clients that I’m sorry for your loss, but let’s make the best of it. Harvesting losses can build economic value that can be used immediately or carried into the future via a tax-carryforward.

With the surge in interest rates, bond funds are likely to have a loss. For example, one could sell a total bond fund to harness that loss and then buy a different bond fund or Treasury bill or a TIPS or TIPS fund. If they have losses in stock funds, they can sell and buy a different low-cost stock fund that meets the requirements to avoid a wash sale. And even if the client can’t offset the losses with gains in other holdings, they can generally take $3,000 in losses this year and carry forward the rest indefinitely.

Clients want to do something in bear markets, and this is doing something that adds value.

4. The government subsidized losses in traditional IRA and 401K accounts. A traditional tax-deferred account is a partnership between the owner and the state and federal government. If, for example, the client had a $100,000 IRA at the beginning of the year and expected to be in the 30% marginal tax bracket in retirement, they owned $70,000 of that account. If the account value fell $25,000 to $75,000, they now own 70% of that $75,000 or $52,500. While the account lost $25,000, the account owner only lost $17,500. The federal and state government subsidized $7,500 of that loss.

If the client then wanted to convert to a Roth, it would be a much better time to do it than at the end of last year. The conversion is buying the governments’ share out at a lower cost. Take these seven items into account in considering Roth conversions.

5. Accumulators are buying stocks at a much cheaper price. While I don’t know the future, I’m certain that stocks and bonds are a much better deal today than at the end of last year. Though this doesn’t help people in retirement, people who are still accumulators are buying stocks and bonds on sale. Buying on sale generally works a whole lot better than buying at the top. Yet we extrapolate the future based on the recent past. That recency bias makes us think that markets are riskier now than in the past.

6. You can prove you are a good investor. I tell clients that it’s easy to think of yourself as an investor in good times. But they won’t know if they are really a good investor until the bad times hit. Selling in bad times to go to cash has historically proven to be the wrong thing. Staying the course and rebalancing separates an investor from a speculator. Though there are no guarantees, I expect capitalism to survive.

Encourage clients to look at more than the recent past. Sure, things are bad. Frankly, I’m not only surprised they’re not worse, but at a loss to explain why stocks are up since the end of 2019 given the pandemic, Putin invasion, political infighting and the like. Investing is never easy in bad times. But without pain, there is no gain.

As advisors, and irrespective of our fee model, our job is fairly easy in good times. But we show our value in bad times. Help your client focus on the long term and take advantage of good things in bad markets.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multi-billion-dollar companies and has consulted with many others while at McKinsey & Company.

This has been a very painful year in investing. Not only are stocks in a bear market but, instead of acting as a shock absorber, bonds are having their worst year ever. For bonds, this is the equivalent of the 88% stock plunge during the Great Depression.

This has been a very painful year in investing. Not only are stocks in a bear market but, instead of acting as a shock absorber, bonds are having their worst year ever. For bonds, this is the equivalent of the 88% stock plunge during the Great Depression.