Introducing Protected Lifetime Income Benefits (PLIBs): Part 1

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Despite more than a half century of research detailing the potential value of guaranteed lifetime income products for retirees, sales of annuities, especially traditional products such as single premium immediate annuities (SPIAs), remain low. There are theories to explain why this “annuity puzzle” persists, but one notable barrier to annuitization is the irrevocable transfer of the premium common among annuities.

Despite more than a half century of research detailing the potential value of guaranteed lifetime income products for retirees, sales of annuities, especially traditional products such as single premium immediate annuities (SPIAs), remain low. There are theories to explain why this “annuity puzzle” persists, but one notable barrier to annuitization is the irrevocable transfer of the premium common among annuities.

A product that addresses this concern, which has been available since the 1990s, is an annuity with a guaranteed lifetime withdrawal benefit (GLWB) feature,1 which is common with both variable annuities (VAs) and fixed indexed annuities (FIAs). These products guarantee some minimum level of lifetime income even if the underlying account value goes to zero.

GLWBs have recently come out of favor among some insurers, with a growing number of companies exiting the business. In response, new products are being introduced where the guaranteed income amount “evolves” during the payout phase based entirely on returns of the account, a product I refer to as a “protected lifetime income benefit” (PLIB). While similar to GLWBs, the PLIB is categorized separately because the way the income changes is materially different and can decline. The PLIB concept is not new, with tontines being one of the earliest examples of products that provide protected lifetime with a form of “shared” risk exposure.

In this series, I will: introduce the PLIB framework (part 1); contrast the efficacy of a variety of longevity protected solutions, in particular a SPIA, DIA, GLWB, and PLIB (part 2); provide context as to why PLIBs end up doing so well in the analysis (part 3); and finally provide some context on the optimal risk levels for PLIB strategies (part 4). This series is based on a larger research paper, available here.

GLWBs and PLIBs: An overview

Early research on the potential benefits of annuitization focused on more traditional, relatively simple guaranteed income products such as SPIAs, also referred to as immediate-fixed annuities. Despite the potential benefits of SPIAs and annuities in general, they remain relatively unpopular among retirees, an effect commonly dubbed the “annuity puzzle.”

While there are a variety of explanations for the annuity puzzle, one notable barrier is the irrevocable design of many annuities (e.g., SPIAs), which requires the annuitant to permanently cede the premium to receive the lifetime income. The irrevocable aspect of the product is likely the primary reason sales of SPIAs and DIAs are relatively low compared to other income strategies.

One product feature that provides lifetime income yet also allows on-going access to the premium is a GLWB, also sometimes referred to as a “guaranteed minimum withdrawal benefit” or GMWB. These are common in both variable annuities (VAs) and fixed indexed annuities (FIAs) and could be offered with more traditional portfolios as part of a contingent deferred annuity (CDA). Introduced in the 1990s, GLWBs allow access to the contract value (i.e., are revocable) and guarantee some minimum level of lifetime income (which could potentially increase) even if the underlying account value goes to zero.

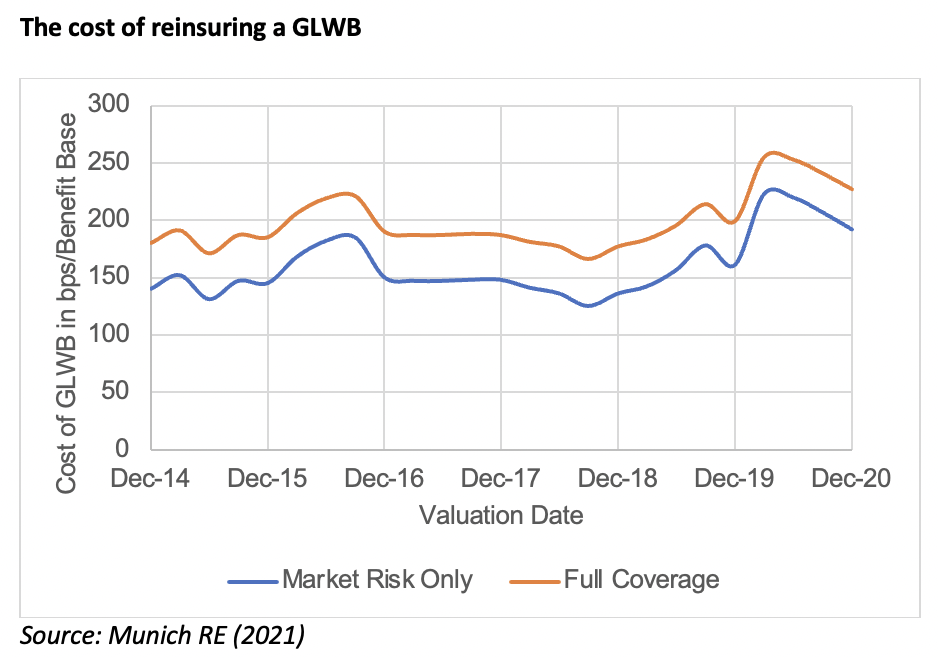

GLWBs have come out of favor, with several providers exiting the business, given the low bond yield environment and the rising costs associated with issuing them. For example, Munich RE (2021) has released research estimating how the reinsurance cost of GLWBs has changed from January 2000 to December 2020, which is included below.

Munich RE has two potential cost estimates2 and the cost of both has increased significantly, recently exceeding 200 bps, well above current fee levels, which tend to be 150 bps or less.

In response to the challenging economics associated with issuing GLWBs, there has been an increasing number of products that offer lifetime income. But their income amount “evolves” based on the returns of the underlying portfolio, for better or worse, without the same income floor as GLWBs (i.e., the income level can decline). I refer to these products as PLIBs. While PLIBs are relatively similar to GLWBs and could fall under the same general lifetime income umbrella, a separate naming approach is used given the notable difference in how the income can change during retirement.

The PLIB structure is not new. For example, one of the oldest longevity products that could fall under the PLIB umbrella is a tontine. It is an annuity structure devised in the 17th century where annuitants (also called subscribers, shareholders, investors, etc., depending on the structure) share in the investment and mortality experience of the pool. While tontines are not widely available, there is growing interest in the structure and some recent products have been designed using the approach.

This analysis assumes that only the investment returns affect the PLIB benefits, not the mortality experience, which implies the backing of an insurance company. While tontines could theoretically be included in the analysis, miscalculations regarding mortality experience can have significant implications for the annuitants who survive the longest. By focusing on an “insured” PLIB structure, we can more easily compare the benefits of a strategy with other strategies that have a different payout approach (e.g., GLWBs) but which also have explicit mortality guarantees.

Additionally, an immediate variable annuity is a PLIB since the lifetime income evolves based on how the credited returns compare to the assumed interest rate (AIR) during the distribution period. These products are relatively rare3, though, and typically require an irrevocable decision.

GLWB payout mechanics

The income for a GLWB is based on applying the payout rate, also known as the guaranteed percentage or lifetime distribution factor, to the “benefit base” (also called the income base). The payout rate is based on the age of the annuitant at the time of the first withdrawal, or the younger of the two annuitants if it’s a joint couple. GLWB payout rates typically increase at older ages at varying increments (e.g., some companies have five-year bands, other more granular levels) and are typically higher for single versus joint annuitants.

The benefit base is a “shadow account” (i.e., it is not accessible) that determines the income level. The benefit base typically uses the greatest of the contract policy values at each of the previous anniversary dates (i.e., the highwater mark). Some GLWB products have additional valuation methods, such as guaranteed crediting rates, which guarantee minimum increases in the benefit base through time.

For example, if a male retiree, age 65, invested $100,000 in a GLWB with a 5% payout rate, he would be guaranteed at least $5,000 per year for life ($100,000 * 5 percent = $5,000), regardless of the underlying contract value (i.e., if it goes to zero). If the annuity portfolio value were to increase to $110,000 (on an anniversary date) the benefit base would “step up” to $110,000 and the guaranteed lifetime income amount would increase to $5,500 ($110,000 * 5 percent = $5,500) and stay at least that level for life, regardless of future performance. The benefit base, and corresponding income level, could increase again if the portfolio value reached a new high on a future anniversary date (although this becomes increasingly unlikely over time).

GLWB fees and provisions vary by provider. Since the GLWB rider is essentially a lifetime put option, if the fee associated with the GLWB rider didn’t vary by equity allocation, investors would be best served investing in the most aggressive portfolio possible inside the annuity. While it was common to offer a variety of investment options before the market crash of 2008 (i.e., the global financial crisis), the vast majority of insurers today still offering GLWBs require annuitants to select among a few relatively well diversified portfolios or only offer a single investment option once the income begins (e.g., a 60% equity portfolio).

When assessing the potential value of a GLWB, or any annuity, it’s important to focus on the product in its entirety versus a single attribute. For example, just because a given GLWB has a relatively high fee does not necessarily mean the product is lower quality. The higher fee could offsett some other benefit that make it relatively more attractive (e.g., a higher payout rate). This can make assessing the relative value of a GLWB difficult given the myriad of features associated with the various strategies. For example, some newer GLWB strategies offer only a few step-ups at a lower fee, an effect I’ve dubbed “GLWB Lite” that can significantly erode the efficacy of the benefit.

PLIB payout mechanics

Payouts from PLIBs are similar to GLWBs, in that PLIBs provide some amount of guaranteed income for life regardless of the underlying account value (i.e., even if it goes to zero). The key difference is that the income from the PLIB changes over time based on performance (of the investments and mortality, depending on the structure), while the income from a GLWB is based on adjustments to the benefit base. For the income to increase from a GLWB in the distribution phase, the return must exceed the distribution amount and the fees, something that becomes increasingly unlikely over time.

The growth in income of a PLIB is typically going to be based on the credited return minus any applicable fees (i.e., net performance), although gross performance could also be used (ignoring any mortality adjustments). For example, if the income from a PLIB was $5,000 and the net return of the account (including fees) for the prior period was +20%, the income level would increase by 20% to $6,000. In this case the income would increase regardless of the underlying value of the contract.

Since the PLIB payout is solely focused on returns (for this analysis), the probability of an income increase is significantly higher with a PLIB versus a GLWB; however, the reverse is also true, whereby the income from a PLIB can decline if the returns are negative (while they would not for a GLWB). For example, if net return of the PLIB account was -20%, an income of $5,000 would drop to $4,000. The income could drop even further depending on account performance. This creates an interesting dynamic around the optimal risk level for PLIBs, which I address in part four of this series.

The income level from a PLIB can either remain constant (for the life of the annuitant) once the account has been depleted or continue to evolve based on the performance of the account. For this analysis, I assume the income is based on the previous year’s value before the account is exhausted.

Comparison

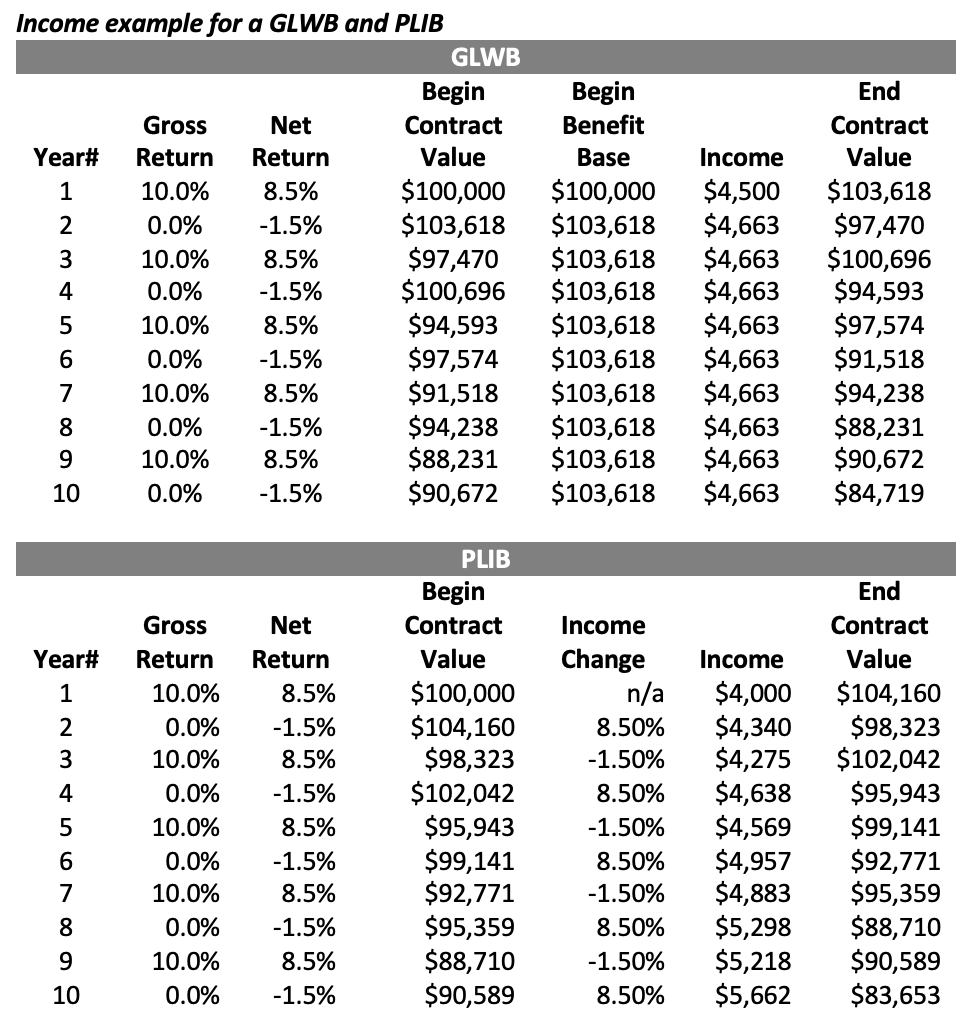

The table below provides an example of how the income would change over time for a GLWB and PLIB, assuming the same initial contract value ($100,000) and returns. The gross returns are assumed to alternate between 10% and 0% each year and the fee is 1.5%, which is assessed against the contract value (effectively reducing the credited return). The initial payout for the GLWB is assumed to be 4.5% versus 4.0% for the PLIB, which reflects existing market payout dynamics for a 65-year-old couple (where initial GLWB payout rates tend to be higher than PLIBs).

The initial income level is higher for the GLWB ($4,500 versus $4,000); however, by the end of the 10-year period the PLIB income level is higher ($5,662 versus $4,663). This is primarily attributed to the positive average return over the period (5% gross and 3.5% net). While the income from the GLWB increased in the first year, there were no subsequent increases because the contract value never again reached a new highwater mark (effectively entered a death spiral, which is common with GLWBs). This contrasts with PLIB, where the income level changes annually based on realized returns, increasing in years with the positive net returns and decreasing in years with the negative net returns. By freeing the income growth level from the benefit base, the PLIB provides significantly more upside with respect to income, but also subjects the annuitant to more downside.

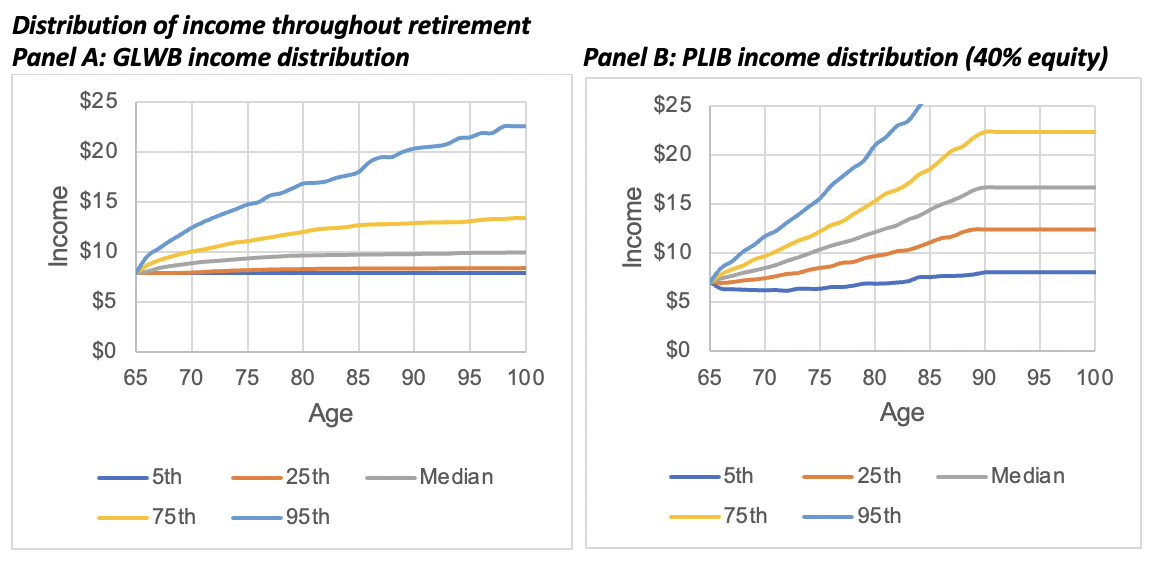

The distribution of the income from a GLWB and PLIB is demonstrated below, which is based off the key assumptions outlined in the next piece in this series (exploring the efficacy of the products). The GLWB is assumed to have a 60% equity allocation (the maximum possible) and annual step-ups, while the PLIB is assumed to have a 40% equity allocation (more conservative to balance the risk associated with portfolio declines and the subsequent reduction in lifetime income).

The income distribution for the GLWB is clearly tighter than for the PLIB. While there are a few scenarios where the income level increases considerably for the GLWB, the increases tend to be relatively small, and occur at a decreasing rate throughout retirement. In contrast, the income levels from the PLIB increasingly diverge over time, reflecting the cumulative returns (and volatility) of the portfolio over time. Positive returns generally benefit the PLIB more than the GLWB, since the income level for the PLIB is based entirely on the credited return (versus achieving a new highwater mark for the GLWB). Again, the PLIB income is assumed to remain constant after the portfolio values are exhausted, which is why the income distribution flattens for the PLIB at older ages (although some PLIB products do have income levels that continue to evolve even after depletion).

Conclusions

This piece introduces an acronym, protected lifetime income benefit (PLIB), to describe an emerging category of longevity-protected solutions. Market dynamics have made GLWBs less favorable, and some of the new products being introduced have attributes that result in questionable value to retirees.

The underlying construct of “shared” risk exposures for lifetime income is not new, with products such as tontines dating back to 17th century.

In part two in this series, I will more explicitly address how PLIBs perform compared to other annuities when it comes to generating lifetime income (hint: PLIBs do very well). In part three, I provide context around the inherent advantages PLIBs have over other strategies, and in part four, I provide some context on optimal PLIB risk levels.

David Blanchett, PhD, CFA, CFP®, is managing director and head of retirement research at PGIM. PGIM is the global investment management business of Prudential Financial, Inc. He is also an Adjunct Professor of Wealth Management at The American College of Financial Services and a Research Fellow for the Retirement Income Institute.

1Also called a “Guaranteed Minimum Withdrawal Benefit” or GMWB

2The “Market Risk Only” level of the RCI uses a reinsurance structure that provides similar risk protection to a complete market-risk hedging program covering all relevant greeks, while also reinsuring all cross-greeks and operational risks associated with a hedging program. The “Full Coverage” level of the RCI uses a reinsurance structure that transfers all material risks, including non-hedgeable risks such as behavior risk and basis risk (with the exception of post-claim longevity risk which is not transferred because the reinsurance claim is paid as a lump sum).

3Perhaps the most notable exception would be the CREF variable annuity, offered by TIAA

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All