Playing Inflation Russian Roulette in Retirement

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits The question most asked by investors late last year, as Treasury bill yields hovered just above zero was “Where can I go for yield?” followed soon after by “What can I do to protect myself from inflation?”

The question most asked by investors late last year, as Treasury bill yields hovered just above zero was “Where can I go for yield?” followed soon after by “What can I do to protect myself from inflation?”

The answer to the first question is that interest rates area discount rate – the price one pays or the return one gets for accepting risk. They have an inverse effect on the prices of assets. One is thus faced with a metaphysical choice between a large portfolio with crummy interest/dividend payments, or else a smaller one with a higher yield. In other words, be careful of what you wish for.

In 2022, that penny dropped as investors finally got their devoutly desired higher yields, paid for with the savaging of the principal value of their portfolios.

The second question had an equally painful answer to many investors in 2021, the most obvious way to protect against inflation seemed to be the purchase of Treasury Inflation-Protected Securities (TIPS). After all, a TIPS provides a nearly perfectly safe way of paying for inflation-adjusted living expenses, but only when held to maturity.

The rub is that the road to that desired result is often bumpy, and, more importantly, the price paid for that inflation guarantee at maturity can vary widely. What folks who bought TIPS last year and early this year, hypnotized by that inflation protection and seemingly riskless promise of secure future consumption, ignored was that the price paid would be dear indeed if and when the Fed responded to inflation by raising rates. For example, the 30-year TIPS auctioned this February at a 0.125% coupon went for 97.96; as of this writing, that same protection of real consumption in 2052 can be purchased for an inflation-adjusted price of 69.23 (which calculates to a real yield of 1.63%). Ouch. Another way of putting it is that good things often come to those who wait; the losses in long nominal Treasury securities have been similar.

The prices of equities followed a similar path. Just who won and who lost during the annus horribilis of 2022? The most obvious winners were young savers who can now purchase stocks and bonds at much lower prices and at much higher yields and expected returns.

The most obvious losers were the folks who in 2021 reached for yield by extending maturities, or who decided it was a good time to defease their future consumption with TIPS. This is best illustrated at the short end of the nominal Treasury curve: In mid-2021, the three-month yield stood at 0.16%, while the five-year note offered all of 0.29%. In other words, one got 13 bp more yield by extending out 4.75 years.

At the risk of being overly harsh, that wasn’t a yield curve, it was an IQ test.

But this suggests another group of winners: those who kept their maturities short and can now extend those maturities at a much higher yield or defease their future consumption at a much lower cost.

The only question is how to do that. Investing is about the conveyance of real consumption from one’s present self to one’s future self. For the average person, that means the conversion of today’s human capital into tomorrow’s investment capital, and the most secure way of doing so, by far, is with a stream of real income throughout retirement. The key word in that last sentence is real. It does no good to defease future consumption with nominal instruments if future high inflation turns today’s seemingly plump annuity and long bond yields into tomorrow’s funny money.

It would be nice if one could purchase inflation-adjusted annuities, but those products have gone the way of disco, and I suspect that proposing their revival would not be a career enhancing move for any insurance company executive who suggests it. The best that one can do in this regard is to “purchase” the inflation-adjusted annuity offered by spending down one’s retirement assets to defer Social Security until age 70.

The most fortunate retirees are those whose living expenses are covered by Social Security and pension checks, and whose retirement assets, consequently, do not actually belong to them, but rather to their heirs, to their charities, and to Uncle Sam (to whom we all owe a great deal).Most, however, will need an additional source of retirement income to defease their future consumption.

The single most important factor that determines how to do that is the nest-egg burn rate (your annual spending divided by the size of your retirement portfolio). I suggest the following rule of thumb: if your burn rate is below 2% at age 60, below 3% at age 70, or below 4% at age 80, a standard stock/bond portfolio will nicely see you through your retirement, and you have no need to annuitize your assets.

If your burn rate is above those thresholds and you want to annuitize, how should you do it? At a practical level, one has two choices: a 20-30-year TIPS ladder or a nominal single-premium immediate annuity (SPIA). There are pros and cons to both; the major risk of a TIPS ladder is that one will outlive the 30-year rung, while the major risk of a SPIA is inflation. (An acceptable alternative to a TIPS ladder, which for the sake of simplicity I won’t discuss, is a combination of TIPS funds whose average duration is appropriate to your retirement horizon.)

My colleague and friend Allan Roth recently wrote a marvelous article on this website which demonstrated how to construct, using a spreadsheet written by retired corporate analyst Bob Hinkley, a TIPS ladder from which one could spend an inflation-adjusted 4.3% per year before it ran out in 30-years. Hinkley’s spreadsheet is rather complicated; Allan used it to personally purchase 24 of the 50 currently outstanding TIPS at an average yield of 1.83%. (Allan only bought 24 different TIPS, and not 30, because there are no maturities for the years 2033–2039)

Hinkley’s spreadsheet is rather daunting, and unless you’re a glutton for punishment, you don’t need to purchase rungs for each year; five or six widely spaced ones, which upon maturity might be used to purchase a short-term TIPS fund, are likely adequate. A simple straight-line mortgage calculation serves as an excellent approximation to converting the TIPS yield to the 30-year burn rate; with annual payments, Allan’s TIPS purchase yield of 1.83% produces the exact same safe spending rate of 4.3% with annual withdrawals over 30 years.

At present, the average TIPS yield across its curve is 1.6%, which converts to a 30-year burn rate of 4.2%; a $1,000,000 ladder extending out 30 years will yield an initial monthly payment of $3,494.73, which rises with inflation. (To keep an apples-to-apples comparison, I assumed the theoretical simplification of monthly payouts for both the TIPS and annuity strategies.)

As an alternative, a 65-year couple old can purchase a joint-survivor nominal SPIA with a payout of 6.6%, which will produce a nominal $5,500 monthly payment, which will, however, not rise with inflation. Our theoretical annuitants, who will also be spending the same inflation-adjusted $3,494.73 every month as with the TIPS ladder, can bank the extra $2,005.27 in an “excess account” that first month. That excess falls every month as they spend yet a little more as time passes to keep up with inflation. Further assume, for the sake of simplicity, that the “side account” of excess funds is invested in Treasury securities at a zero real rate. As spending increases with inflation, that excess will decrease and finally disappear, at which point one taps into the excess account. Finally, after some years, the excess account runs out, and the couple is left with only a rump nominal payout that provides only a fraction of the real initial payout.

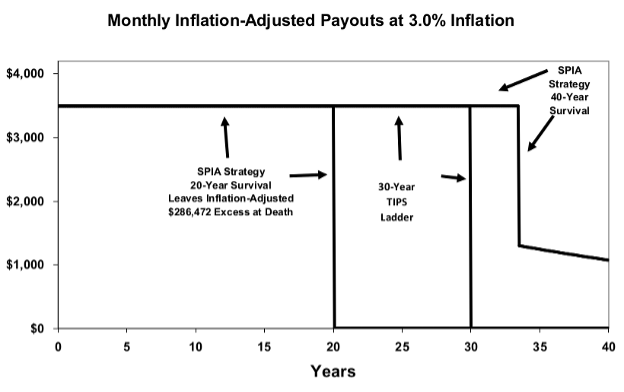

Let’s see how this plays out in a “normal” world of 3% inflation in Exhibit 1:

This plot needs a little unpacking. The path to the far right represents the sequence described above if the couple survives 40 years; here, the annuity + side account strategy is clearly superior the TIPS ladder cuts out at 30 years (at which point our couple has survived to age 95), whereas the annuity + side account lasts for 33 years (at age 98), following they receive a much smaller stream. But if the couple’s joint survival only lasts 20 years, their income stream disappears at that point, and their heirs inherit a $286,472 side account, which would be less than the total real $419,368 stream they’d inherit with the last 10 years of payments from the 30-year TIPS ladder (assuming a zero real discount rate).

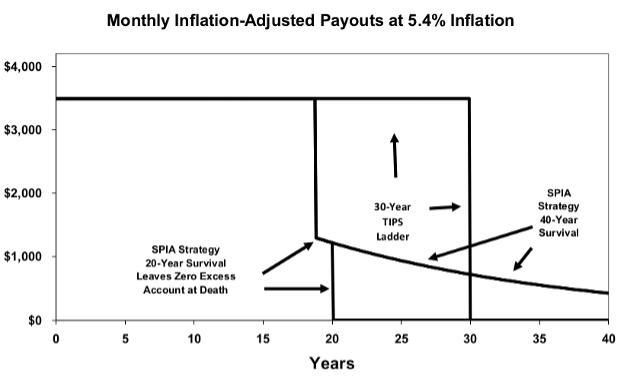

Now let’s look at how the two strategies do with high inflation. The worst 30-year inflation in the U.S. was the 5.4% rate experienced between 1966 and 1995. What happens in this scenario is shown in Exhibit 2:

In this case, the results are potentially catastrophic for the annuity + side account strategy; to maintain the monthly $3,494.73 real payout, the side account gets exhausted after only 19 years, following which only the rapidly depreciating real stream of nominal income remains. And if the couple’s joint survival lasts only 20 years, the heirs lose out on the last 10 years of the undiminished real stream of the TIPS ladder.

Some might point out that it’s possible to purchase a SPIA with a cost of living adjustment (“COLA”). Such products have a lower initial payout that increases at a constant rate, not the actual inflation rate, and are thus not a true COLA of the sort offered by Social Security. But they do offer a useful way of thinking about the effects of inflation; if one buys a SPIA with a 3% annual “COLA,” one wins/loses if inflation is lower/greater than 3%. Moreover, the SPIA with “COLA” is in fact more exposed to inflation, since its discount-weighted cash flow occurs further out into the future.

The choice between the TIPS ladder and annuity + side account strategies is a classic Pascal’s wager; “losing” in a low-inflation environment with the former by missing out on a slightly longer stream of income might be painful, but “losing” with the latter in a high-inflation environment could prove devastating.

What are the odds of such an inflationary scenario? One is reminded of Nassim Taleb’s dictum that “this so-called worst-case event, when it happened, exceeded the worst case at the time.” In other words, 5.4% long-term inflation is nowhere near the worst-case scenario. Even a casual glance at the global history of fiat money in the twentieth century shows that hyperinflation is the rule, not the exception. During the above-mentioned 1966-1995 period, U.S. debt/GDP averaged around 50%; now, it’s more twice that level and rising rapidly, and given the hundreds of trillions of dollars of additional implicit debt (promises to Social Security and Medicare, and to backstop future emergencies – think military aid to Ukraine and weather or terrorism disaster relief) it won’t take much to tip things over into a debt spiral, especially if the Treasury has to roll its debt over at higher interest rates for very long.

I have no idea what the odds of such a future inflationary scenario are, but it’s a good bet that, given the cruel mistress of economic history and burgeoning explicit and implicit debt, those odds are well above zero.

The risk of blowing your brains out playing Russian Roulette are one in six, which I submit are a conservative estimate of the probability of significant future inflation, so why play retirement Russian Roulette with a nominal annuity or, for that matter, with long-term nominal bonds of any sort?

Moreover, nominal annuities also carry credit risk, which is not trivial; insurance company salesmen are fond of pointing out that none failed in 2007-2009, and that in any case they are backed by state guarantees. But in 2022, U.S. fiscal strength is not what it used to be, and in a real crunch, the state guarantees will not even be a speed bump on the way to widespread insurance company defaults.

I’ll give the closing words to the erstwhile Mr. Roth, who phrased his skepticism of annuities as follows: “Actuaries are very smart people, and if they aren’t willing to take the inflation risk, I don’t recommend my clients take it either.”

William J. Bernstein is a neurologist, co-founder of Efficient Frontier Advisors, an investment management firm, and has written several titles on finance and economic history. He has contributed to the peer-reviewed finance literature and has written for several national publications, including Money Magazine and The Wall Street Journal. He has produced several finance titles, and four volumes of history, The Birth of Plenty, A Splendid Exchange, Masters of the Word, and The Delusions of Crowds about, respectively, the economic growth inflection of the early 19th century, the history of world trade, the effects of access to technology on human relations and politics, and financial and religious mass manias. He was also the 2017 winner of the James R. Vertin Award from CFA Institute.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All