Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Famed investor Benjamin Graham once wrote, “The intelligent investor is a realist who sells to optimists and buys from pessimists.” To walk the line between optimism and pessimism is the task of the prudent investor, and that is challenging when the ups and downs of the market encourage ill-advised practices such as market timing or overreliance on historical performance.

The unpredictable cyclicality of the market gives the unemotional investor the advantage to make thoughtful adjustments to a portfolio, even when consumer sentiment is historically low. Staying invested over the long term and deploying more capital when consumer sentiment is pessimistic can lead to better outcomes over full market cycles.

The Michigan Consumer Sentiment Index is a monthly measurement of the health of the economy, from the perspective of consumers. Conducted by the University of Michigan’s Institute of Social Research, it was originally created in the 1940s by Professor George Katona. Katona’s data collection process began with his researchers contacting households nationwide by phone. The index has come a long way. Today, investment managers, advisors, and economists rely heavily on the Index to gain insight into the average consumer’s attitude toward the economy.

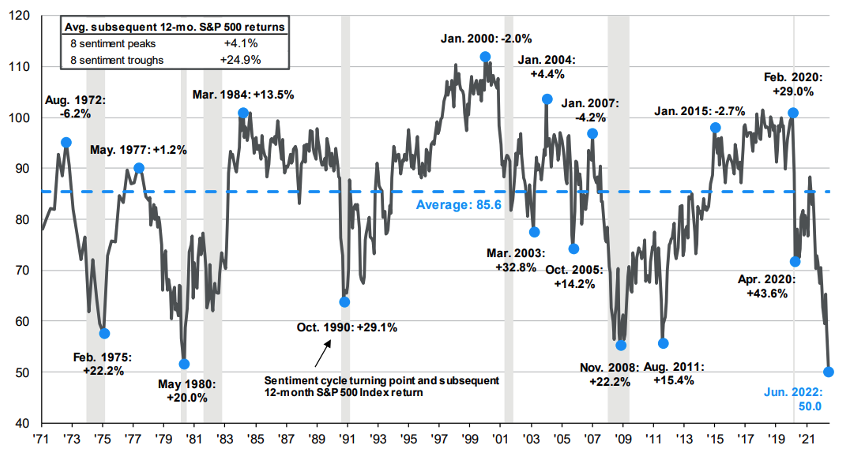

The graph pictured below tells the story of the highs and lows of consumer sentiment from 1971 through the first half of 2022, over a half-century of data. The dark line depicts the Consumer Sentiment Index over time, with the blue dots representing the peaks and troughs over the decades. The shaded vertical bars show recessions since 1971.

Source: JP Morgan

The most important story is the subsequent 12-month S&P 500 returns listed next to each peak and trough. The average 12-month return following troughs in consumer sentiment outperformed the average 12-month return following peaks in the Index 24.9% to 4.1%, a 20% difference. Even if one were to exclude the largest and most recent post-COVID bounce-back (43.6%) from the calculation of the average post-trough return, the figure is still 22.3%. There is substantial correlation between overwhelming pessimism, as measured by the Michigan Consumer Sentiment Index, and very strong S&P 500 returns over the course of the subsequent one-year period. The “Oracle of Omaha,” Warren Buffett, said it best: “Be fearful when others are greedy. Be greedy when others are fearful.”

Source: A Wealth of Common Sense

Market returns hit their ceiling when sentiment is bullish. When sentiment is low, it can seem like the market will never recover; that is, until it does. Supply chain disruptions and pain at the gas pump understandably turned many investors into savers, but liquidity needs should not be overemphasized at a time when markets are trading at a discount. Pessimism leads many investors to stash their spare cash rather than methodically putting it to work in the market like they might have done in more encouraging circumstances.

This is when being an unemotional investor pays dividends.

While it seems like common sense that there isn’t nearly enough luck to go around in timing the market, our human nature still drives us to the very thing we intuitively know not to do. Herd mentality and emotional decision-making come naturally to many investors. We react to information instantly. The market, however, reflects prices three to six months ahead of the current news cycle. Once the doom and gloom settles, and the general population has had their fill of Armageddon, it is often too late. You’ve missed months of the market’s rebound! Using market returns as an indicator of when to invest your household wealth is a dangerous game to play.

Your starting point matters. That is why we believe staying invested during market turmoil is the only way not only to gain back losses, but also to participate in each bull market fully. Shelby Collom Davis, founder of the Davis Investment Discipline, stated “You make most of your money in a bear market; you just don’t realize it at the time.” Taking advantage of market dislocations drives long-term performance. Timing the market rarely captures the same result as staying invested.

While we do not claim to have any ability to predict where the markets will go, the Consumer Sentiment Index hit a 50-year low in June. Consumer sentiment is still low; it is 56.8 versus 50 in June. If today’s headlines are any indication, investors have plenty of reasons to be fearful. Staying the course while considering one’s time horizon is the only way to ensure participation in up-markets. Time and discipline are the most reliable tailwinds.

Peter Girard is a member of the due diligence group and the capital markets team at Innovest Portfolio Solutions.

Jack Schutzius is a member of the retirement plan practice group, a specialized team that maximizes efficiencies and implements process improvements for retirement plan clients. He is also a member of the due diligence group, responsible for independently sourcing investment managers, as well as monitoring recommended products and strategies.

Read more articles by Peter Girard, Jack Schutzius

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.