Top 50 Hedge Funds Outperform the Market by 28 percentage points through the first nine months of the year

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

3Q Update to Global Investment Report's 2022 Hedge Fund Survey

As we close out the year, extreme market volatility has dashed hopes that the worst of the selloff is over. Uncertainty is being driven by continued monetary policy tightening, intensification of the Russian war against Ukraine that’s fueling a global energy crisis, rising food costs, and now recession in Europe, which most observers believe will jump the Atlantic to the US next year. Growing liquidity concerns threaten to turn this troublesome brew toxic. All this makes the top 50 hedge funds’ performance even more noteworthy. The group was up nearly 4.5% through September, outpacing the market by 28 percentage points.

November 20, 2022

Multistrategy, volatility arbitrage, and global macro funds again propel the Top 50 further into the black as the market selloff deepened

Early in November, the Financial Times’ Lawrence Fletcher gave us a rare glimpse at a recent Elliott Management investor letter. The venerable hedge fund warned economies and markets were likely to get much worse before turning around. The clear message: it’s different this time.

Paul Singer, manager of the $56 billion fund, believes an “extraordinary” set of financial extremes that have come as the era of cheap money draws to a close is making “possible a set of outcomes that would be at or beyond the boundaries of the entire post-WWII period.”

The asset manager says, according to Fletcher, that markets could correct by as much 50%, accelerated by hyperinflation and “losses on bridge financing and potential markdowns of collateralized loan obligations and leveraged private equity.”

Bill Winters, CEO of Standard Chartered Bank, which manages over $800 billion globally, feels a bit more sanguine. “It’s appropriate to be cautious right now,” he explains, “but the gloom, arguably, is overdone.”

Then in mid-November, US October inflation numbers came in well below expectations. They were coupled with continued job and retail sales growth and confirmation that the economy did grow in the third quarter, with initial estimates at a not too shabby 2.6%.

These few data points sparked a new round of optimism where some analysts cautiously walked out the prospect that we may finally be getting close to the hump.

All this gives credence to John Kenneth Galbraith’s quip: “The only function of economic forecasting is to make astrology look respectable.”

What to think?

Economist Desmond Lachman, a senior fellow at the American Enterprise Institute, puts things plainly: “The Fed is making the exact same mistake it made leading up to the crisis – except now in reverse.”

Lachman fears the rapid draining of liquidity out of the economy through multiple large rate hikes and quantitative tightening is shocking markets in precisely the same but opposite way extreme rate cuts and massive quantitative easing supercharged them. He fears the result may not only cause significant capital destruction but rising uncertainty that will check investment and growth, which in turn could fuel a cycle of business failures and worse.

Year to date through the third quarter, the market had lost nearly one quarter of its value. Bloomberg reported equity and bond losses amounted to $36 trillion.

However, hedge funds did quite a bit better, according to BarclayHedge. Its broad index of funds lost less than -11.4%. And its benchmark equity long/ short index was down just a bit over 3% during the first nine months of the year.

But Global Investment Report’s diverse group of Top 50 funds – based on the strongest trailing five-year annualized returns through 2021 of broad strategy funds running at least $300 million (that also delivered annual absolute returns since the end of 2017) – generated collective net gains of 4.5%. That topped the S&P 500 by 28 percentage points, a spread that widened 7 percentage points since the end of June.

Returns

Ben Crawford, Head of Research at BarclayHedge, says, “these returns stand out not just in contrast with the average hedge fund performance, but also against returns of the average fund of hedge funds – a more precise comp – which was down -8.2% over the first three quarters of the 2022.”

Even more telling, observed Crawford, is the survey continues, “to show symmetry between consistent returns and the ability to control downside exposure.” Specifically, funds that have been delivering steady long-term gains year over year have weathered the selloff much better than funds that had been generating stronger and more volatile returns. “These observations evolved from the way in which the Top 50 funds were objectively selected,” concluded Crawford.

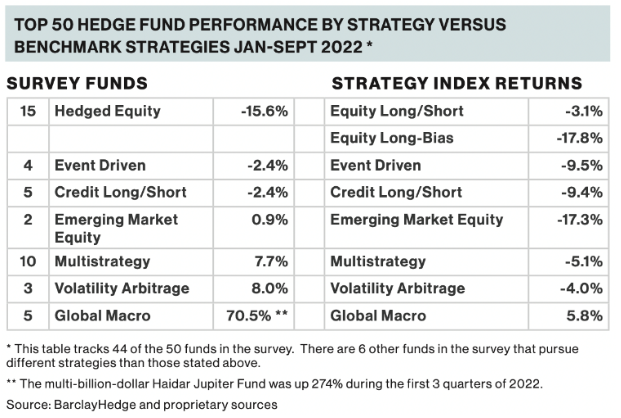

Seven broad hedge fund strategies comprise most of the Top 50. Except for hedged equities, the other 6 strategies outpaced their respective index performance, as reported by BarclayHedge.

Only a few of the Top 50 funds saw substantial changes in performance from the end of the second quarter through the third quarter.

Collective losses of the 15 hedged equity funds saw little change over the quarter, down -15.6%. These declines were offset by 10 multistrategy funds that gained an average of 7.7% and 3 volatility arbitrage funds that returned 8.0% – returns that were in line with their first-half performance. The 5 global macro funds, which soared an average of 70.5%, experienced the most significant change of all strategies during the quarter. All told through September, the Top 50 gained 4.5%.

However, a wide range of strategies and management styles accounted for extreme performance dispersion of the underlying funds. Hedged equity funds saw returns that ranged from +21% to -44%. Their average return (-16%) was just slightly better than the BarclayHedge Equity Long Bias average.

But it was much worse than the database’s Equity Long/ Short Index, which lost -3.1%. The poorest equity performers were North Peak Capital (-43.8%), followed by Old Kings Capital (-40.1%), Legion Partners (-39.7%), and Skye Global (-39.6%). These funds had delivered strong annualized returns going into the bear market.

The best-performing hedged equity funds year-to-date through September were Citadel Tactical (+21.3%) and MAK One (+14.3%), which are actually tracking their historical full-year annualized returns. Schonfeld Fundamental Equity (+3.2%) so far has underperformed its long-term returns by six percentage points.

Through three quarters of the year, two well-known multistrategy managers, Citadel Wellington (+28.7%) and D.E. Shaw (+20.6%), are both significantly outpacing their long-term returns. They helped the group surge past the BarclayHedge Multistrategy index by nearly 13 percentage points.

The Top 50’s global macro funds received a seismic boost from Haidar-Jupiter, which soared 274% through the first three-quarters of 2022. In a recent investor letter, according to Bloomberg, the fund profited strongly from “leveraged rates trading as central banks abandon years of easing and started raising interest rates to contain spiraling inflation. Manager Said Haidar predicts risk assets will remain under pressure as investors readjust their expectations to be more in line with central bank guidance, and monetary policy tightening continues to drain liquidity from markets.”

Macro fund John Street Capital climbed nearly 36%, tripling its historical annual returns. These two funds helped the 5 macro managers in the survey to generate returns light-years past the Barclay- Hedge Global Macro index, which enjoyed respectable returns of 5.8%.

The big question facing all funds that have been on a tear during such a challenging year is whether they’ll be able to adjust their investments when monetary and other key risk factors change. We recently witnessed managers who thrived during the initial shock of the pandemic fail to rotate their portfolios as economies reopened and consumer habits changed.

Some noteworthy returns outside of these 3 strategies include Whitehaven’s Credit Opportunities, which relies on fixed-income relative trades of municipal debt. So far it has weathered rising interest rates with year- to-date returns through September of +2%.

Three managers that also appeared to be vulnerable to rising interest rates and related stress also did quite well. Opportunistic junk debt specialists Millstreet Capital gained 4% and Arena Special Opportunities was minimally in the black. Emerging markets equity manager Waha MENA surged in the third quarter with year-to-date returns up by more than 12%, while the average emerging market hedge fund lost more than -17%.

On the downside, merger specialist Ramius declined -13.2%. And concerns this report initially expressed about how a rising interest rate cycle may hit the intriguing Enko Africa Debt fund have materialized. The fund declined -19.2% during the first nine months of the year – a slight improvement over its mid-year loss.

Macro environment

Despite consensus that recession is coming, Patrick Ghali, managing partner at the alternative investment consultancy Sussex Partners, doesn’t believe markets have yet priced that into valuations. He points to junk bonds, whose first-half collapse has stabilized.

After registering record profits, the head of one of the world’s largest container shipping firms, AP Moller-Maersk, says forward-looking conditions look poor. That’s disconcerting given shipping activity is a bellwether of future trade and a likely reflection of business and consumer confidence. CEO Soren Skou sees, “every indicator we are looking at is flashing dark red.”

US corporate earnings, meanwhile, remained upbeat. As of mid-November, Howard Silverblatt, senior index analyst at S&P Dow Jones Indices, found with more than four-fifths of the S&P 500 companies having reported third-quarter earnings, nearly 70% beat the street’s estimated earnings. This number is slightly below those reported over the past dozen quarters. But it’s within the range of earnings beat over the past decade. So it’s unclear whether this number portends worsening corporate health.

Then there’s the fear of spiraling wage growth. In a recent report, the IMF believes the risks on this front are limited due to several factors: It cites temporary “underlying shocks to inflation coming from outside the labor market, falling real wages that are reducing price pressures, and central banks aggressively tightening monetary policy.”

Looking historically at wages as a percent of corporate income also mitigates this concern.

But Dan Zwirn, manager of Arena Special Opportunities fund (No. 41) sees a more systemic problem, which dates back to 2012 when the Fed embarked on a second round of quantitative easing as economic growth stumbled after escaping the Great Recession.

“You want to use QE in an emergency,” explains Zwirn. “You don’t want to get used to it.” And that’s what happened, again, after the initial shock of the pandemic had passed. This led to tremendous asset bubbles and systematic mispricing of risk, layering “an enormous debt on the economy that we would effectively have to pay,” observes Zwirn. That bill came due in the form of runaway inflation, and to Zwirn, there are no other tools left to use than drastic interest rate increases and the trauma that comes with them.

Former portfolio manager and alternative investment advisor to several Swiss banks, Robert Khoury, cautions the rapidity of sharp central bank rate increases ignores the reality that each rate increase requires six to nine months to reveal its economic impact.

“This is one reason why central banks consistently cause recessions when trying to fight inflation,” Khoury explains. And in the current environment, there are externalities that rising rates can’t touch. This includes China's protracted COVID lockdown and the Russian invasion of Ukraine, the latter causing energy prices to soar. Khoury fears the consequences of relentless monetary tightening, “will likely be dire, impacting liquidity and the health of financial systems.”

While bank leverage has been materially reined in since the financial crisis, Khoury still thinks it’s an issue as financial stress rises. And he believes institutions like Credit Suisse, Deutsche Bank, and BNP Paribas are especially vulnerable. He posits the European Central Bank will likely need to guarantee the health of certain banks to avoid larger shocks.

Economist Desmond Lachman agrees with Khoury. He believes the Fed is too focused on reclaiming its credibility and not modulating its actions in the most effective way. “It risks breaking a whole bunch of things,” says Lachman, since other major central banks will be forced to move in relative lockstep to keep their global businesses competitive.

After years of gross credit misallocation and record debt levels, Lachman fears the net result of sharp and rapid interest rate hikes will likely cure inflation, but at a cost of having created a wave of bankruptcies, credit market stress, emerging market debt defaults, a sharp rise in unemployment, and global financial instability.

Outlook

Despite recent positive news about US inflation, employment, and growth, most observers think we’re still in for more challenging times.

Graham Capital Management’s Ken Tropin was spot on when, in last quarter’s review, he discounted the mid-summer rally and expected stocks to again fall. While the S&P has rebounded in October, he believes the market will remain volatile, with a chance of revisiting previous lows.

This call is largely fueled by Tropin’s belief that inflation will likely remain stubbornly high. While he expects it to start retreating, he believes reaching Fed target rates is still a couple years off. This means the Fed will continue to tighten and the dollar is likely to sustain its strength.

However, with UK and European inflation running red hot, their respective central banks may be forced to drive up interest rates faster than planned around the same time the Fed may be slowing its pace of monetary tightening. This could cause Sterling and the Euro to rally.

Fearing the rapid ascent in interest rates, Desmond Lachman thinks the Fed should be dialing back its pace and size of hikes to see what their impact on the economy will be. He notes mortgage rates have more than doubled since the start of the year to around 7 percent, which has sent the US housing market into recession.

With aggressive monetary policy having caused the equity and bond price bubbles to burst and having sent the dollar to a 24-year high, he urges the Fed to be more mindful of the impact its actions are having across global financial markets. “At the very least,” Lachman says, “the Fed should be slowing down quantitative tightening, which is currently withdrawing liquidity at a rate of $95 billion a month. “Failure to do this is inviting a major financial market crisis both at home and abroad.”

More hawkish than Lachman, Arena’s Dan Zwirn thinks higher rates are essential. But he does agree that risks related to this shift still haven’t been factored into economic forecasts. He believes, “debt loss recognition” is largely being masked by refinancing. But he predicts, “a maturity wall will soon be hit when leveraged loans and distressed bonds come due, but refinancing isn’t available for increasingly troubled companies.”

Arena is addressing this growing risk several ways. Rising demand by many counterparties with which Arena transacts is putting the firm in a strong negotiating position. Zwirn is requiring “tremendous margins of safety, as senior as possible, with as little duration as we can get, with as much compensation and control we can bargain for.”

Arena protected itself earlier in the year against interest rates moving much higher than most thought would happen, which has paid off. And it has rotated realized gains into Put options.

It’s investing in private convertibles and positions “that are intrinsically disconnected from the overall economy,” explains Zwirn, “such as litigation finance, pharmaceutical or musical royalties, and insurance-related investments.”

Alternative investment advisor Khoury urges allocators to favor managers that have reduced leverage and net exposure, targeting macro, trend-following, and market neutral strategies.

While he believes a time will come to turn to distressed and relative value strategies, we’re not there yet. With the current Fed overnight rate under 4%, he thinks it will continue to rise and top out early next year between 4.5% and 5%. When that happens, he thinks default rates will have peaked, offering distressed investors better opportunities. And as the bond market stabilizes along with rates, then there will be more reliable fixed-income relative value opportunities.

Cedric Dingens, head of alternatives at NS Partners with CHF10.5 billion under management, thinks US rates are likely heading even higher, peaking toward 6% by June 2023. “The Fed is desperate to reclaim its credibility after infusing too much liquidity into markets for too long,” explains Dingens. And he thinks this is leading to the Fed’s bifurcated reality: “It’s our currency, it’s your problem.” This is forcing coordination of central bank moves across developed markets and leaving emerging markets in trouble.

Dingens favors global macro strategies that continue to benefit from high volatility across many asset classes, while collecting 4% yields on unencumbered cash. He’s also positive about leading multistrategy funds that continue to deliver positive risk-adjusted returns. With inflation being more accurately reflected in their valuations, the allocator also thinks TIPS look promising going forward.

What he’s not so certain about is hedged equity, which has failed to generate much alpha in 2022 after a so-so 2021. He says one reason is that shorting has been challenging. Because of the cyclicality of alpha, he’s hoping it may return in 2023.

All this said, Dingens commitment to alternatives remains strong. The key reason: the lack of visibility. “This is a problem that seems to be getting worse,” explains Dingens, “as uncertainty remains high with exogenous shocks seemingly now a regular occurrence.”

This leads us back to the war.

Economic historian Niall Ferguson explains, “Wars have played a very noticeable role in the history of inflation expectations.” He adds, “major breaks in the downward trends in interest rates were nearly all associated with wars, particularly those that destroyed capital stock and generated monetary financing of debt.”

Ferguson fears growing economic and geopolitical instability if the war escalates without signs of a decisive winner or a serious pitch towards negotiations.

New York Times columnist Thomas Friedman echoes this sentiment, reminding us what the last three decades have brought. “We have connected so many people, places and markets and then removed so many of the old buffers that insulated us from one another’s excesses and replaced them with grease – that instability in one node can now go really far, really wide, really fast.” That is why, he argues, the Russian attack on Ukraine is a World War.

Ukraine’s retaking of Kherson is just the latest part of a remarkable counteroffensive. It’s emblematic of economy and markets – that recovery comes in steps – never a straight line and always with more challenges than one can anticipate. And even when the end appears near, it can easily drift further away, and morph into something that wasn’t expected.

Eric Uhlfelder has prepared 19 annual hedge fund surveys for Barron’s, The Financial Times, The Wall Street Journal, and SALT. He has been covering global capital markets from New York over the past 30 years for various major financial publications. He wrote the first book on the advent of the euro post currency unification, Investing in The New Europe, for Bloomberg Press. And he has earned a National Press Club Award. To see the full 2022 Global Hedge Fund Survey with detailed metrics of the Top 50 funds, please write the author at [email protected]

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All