Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Billionaire philanthropist Chuck Feeney is credited with saying, “I want the last check I write to bounce.” While that is ideal, it’s unrealistic.

Or is it?

No one can predict exactly how long they will live, but they can estimate their maximum life span. Age 95 is a common benchmark, but for a cushion you could use 100 or 105. Regardless of what age you pick, it’s possible to plan for your principal to approach zero at that age by using the DoubleBucket® method. The DoubleBucket method uses a variable withdrawal rate that adjusts to market conditions. Even with that adjustment, the average withdrawal rate for the DoubleBucket method has always been higher than the 4% rule.

The 4% rule, as well as the Monte Carlo method, do a good job of providing a high level of confidence that a specified income stream will be met. However, to provide this safety net, the withdrawal rate needs to be conservative. In addition, there is no guarantee how much money will be left at the end. History has shown that some spans using the 4% rule barely made it, while other spans left several multiples of the original principal. Many clients are willing to sacrifice lower cash flow for this confidence, but other clients may have a different viewpoint. They may feel like money is being left on the table and are willing to take some risk in optimizing their income stream. Some clients may have under-saved and have no legacy wishes at all. This is where the DoubleBucket methodology offers a better approach.

How does the DoubleBucket manage to wind down exactly to zero? To answer that, let’s consider the inverse situation. If you are 30 years old and want to save a million dollars for retirement in 30 years, how much would you need to save each year? Using your financial calculator with a 6% return estimate (9% for the stock market minus 3% for inflation), a monthly savings rate of about $1,000 should suffice. However, due to sequence of returns, inflation and market unpredictability, the deposit amount and investment diversification would need to adjust along the way. With those adjustments, the end goal could be met. The DoubleBucket methodology does the same, but in reverse.

The advantage of the 4% rule and Monte Carlo method is that they give a high-level of confidence of an inflation-adjusted income stream, whereas the DoubleBucket prescribes an income stream that varies. The advantage of the DoubleBucket is that the average income stream will be higher in almost all scenarios because it will exhaust the principal in its entirety. With respect to the ending principal, the 4% rule and Monte Carlo method may leave a considerable sum at the end. The DoubleBucket method, on the other hand, will always run down to zero.

To analyze how the DoubleBucket has performed in recent history, we will consider the past 21 30-year spans (1972-2001 up to 1992-2021). For any 30-year span, the DoubleBucket suggests an initial ~6% withdrawal rate, a full 50% higher than the 4% rule. With an aggressive withdrawal rate like that, some spans suffer. Specifically, if we look at the span from 1973 to 2002, an initial withdrawal rate of $61k (6.1% of $1m), dropped all the way to $47k just two years later (in real dollars). Real withdrawal rates continued to tumble all the way down to $44k after 10 years. If the client had budgeted $61k to pay non-discretionary expenses, that is a problem.

However, it still beat the 4% rule. In addition, the incomplete spans starting in 2000 and 2007 were problematic, but both seemed to have recovered nicely by 2021. In summary, out of the 21 30-year spans, a few spans performed poorly, while the other spans were much better. Even in the worst spans, the performance was still better than the 4% rule.

A 6% withdrawal rate should be considered a limit. The client can certainly withdraw less to preserve capital for later.

What I’ve talked about so far is a monolithic retirement plan where the same withdrawal amount is required each year. However, a client’s income requirements typically vary from year to year due to a variety of factors. Delaying Social Security, part-time income, and discretionary spending can all affect yearly withdrawals. The DoubleBucket can handle this by shifting money from one phase of retirement to another so that withdrawal amounts are optimized across the entire span.

Let’s take an example of a single client with the following scenario:

- Pre-retirement at age 60 while earning $50k/year in part-time work

- Full retirement at age 65 (no part-time income)

- Delay SS to age 70 at $30k/year

- Desired income of $100k/year from age 60 to 85

- Desired income of $70k/year from age 85 to 105

In tabular form (all amounts are inflation adjusted):

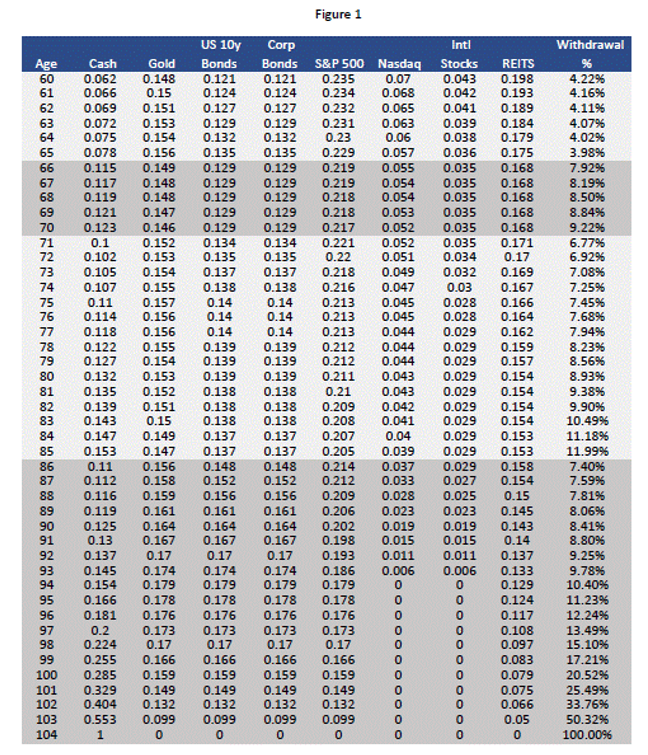

The DoubleBucket will take this data and estimate the required savings to meet these goals. In this case, that amount is a little less than $1.2m. Then, an annuity table (see figure 1 below) will be generated that specifies where assets should be invested and the withdrawal percentage for each year. Asset diversification becomes more conservative in each year of retirement, saving cash for the end. This is how the DoubleBucket guarantees that the principal will last. The withdrawal percentage changes at the inflection points of each phase (these phases are shaded in the figures).

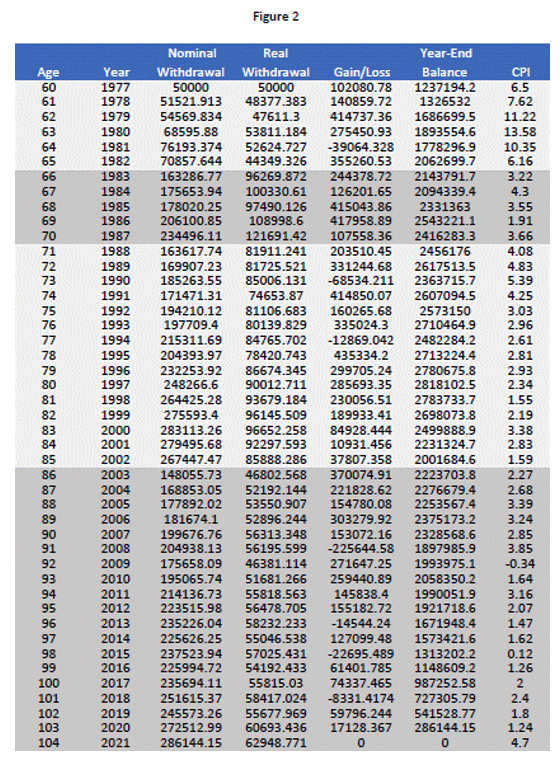

To see how this plays out in practice, see figure 2 below for the span from 1977 to 2021. The “real withdrawal” column in figure 2 roughly correlates to the “principal withdrawal” column from the table above.

The DoubleBucket method is a good way to optimize withdrawals from a fixed principal amount over a finite period. This can be ideal for those clients who don’t have a legacy requirement and can take a little risk with their discretionary spending. Also, it can benefit those clients who have under-saved and have accepted the possibility of surviving off Social Security and Medicaid during their later years. For more information, please see DoubleBucket resources.

Charles Fulmer is based in Tampa, Florida and worked at Fidelity Investments as an advisor.

Read more articles by Charles Fulmer

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.