Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Tight monetary policy and rising government debt will drive a regime of high interest rates, depressing stock prices and destroying the wealth of clients, most severely those at or near retirement.

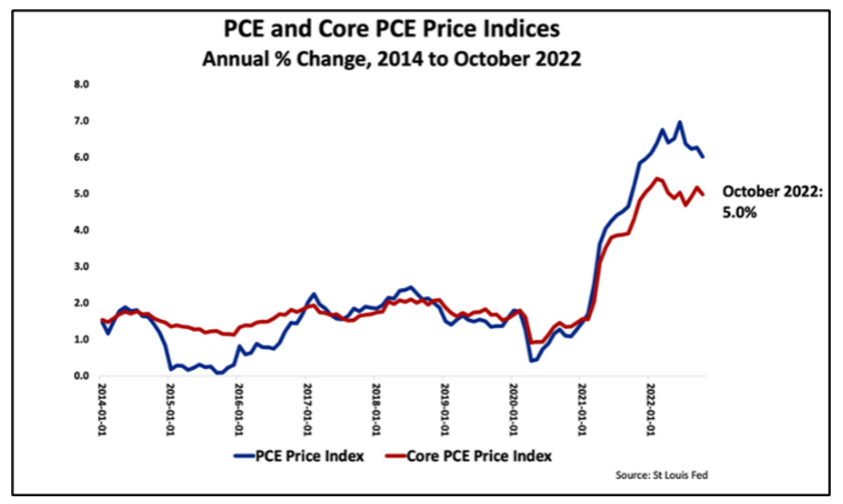

“Inflation and the Labor Market” was the title of Fed Chair Jerome Powell’s speech given at the Brookings Institution on November 30 of last year. Powell shared the Fed’s thinking on inflation, specifically what is propelling it, and how the Fed intends to push inflation back to its 2% annual target.

Powell delivered a hawkish message. He spoke about headline and core PCE, the two inflation measures to which the Fed pays the closest attention. Powell said core PCE inflation continues at a high level, having hovered around 5% throughout 2022, and he acknowledged the Fed’s failure to bring it under control.

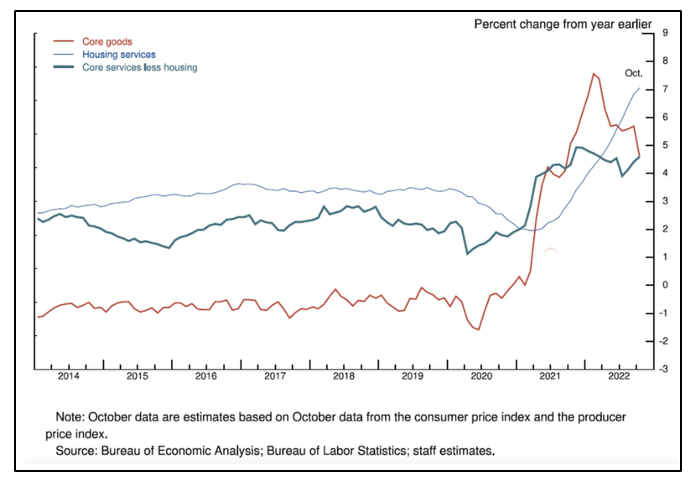

Powell shared a chart that indicated three areas of inflation that are of particular concern: core goods, housing services and core services (less housing). While highlighting the fact that core goods inflation has fallen considerably since its 2022 peak, the opposite was happening in housing services inflation, a trend he projected would not change until the second half of 2023 at the earliest.

Powell also spoke about core services inflation, which he explained accounts for approximately one-half of the core PCE price index. He indicated that the labor market will drive what happens next, while observing that the current extremely strong labor market – 263,000 jobs were created in November – is misaligned with the Fed’s 2% inflation target.

Powell stated that average hourly earnings increased by 5.1% in November compared to the same period in 2021. He explained that the Fed’s 2% inflation target can’t be achieved until wage growth is slowed by around 2% from its current rate of increase. For context, average hourly earnings (HRE) between 2006 and 2019 had an average monthly increase of 0.2%. Toward the end of 2022, HRE increased threefold that average, to 0.6%.

The labor market shows no signs of slowing. According to the St. Louis Fed, there are 1.7 job openings for every person seeking employment. There is no indication that large numbers of workers are going to lose their jobs in the foreseeable future. This also highlights the Fed’s inability to dampen demand.

Macro economist Richard Duncan reminded us that inflation occurs when demand exceeds supply. The Fed, however, has no control over supply. It can only reduce demand by fighting inflation. To reduce demand, the Fed raises interest rates, and destroys money through the process of quantitative tightening (QT). This is done with the unspoken goal of throwing Americans out of work to drive down asset prices and destroy wealth. Fewer jobs and less wealth leads to depressed demand.

Despite all of its recent monetary tightening and rate hiking, to date the Fed has not succeeded in slowing wage growth or in reducing the number of jobs.

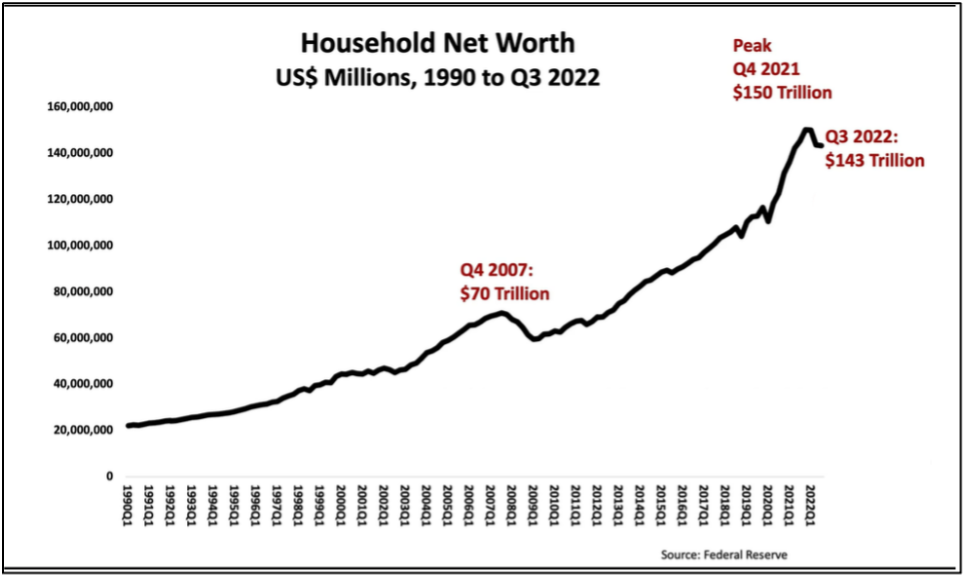

Household net worth

After peaking in January of 2022, by October the S&P 500 declined by 22%. Following a slight rebound, the S&P 500 is now down 20% from its January 2022 peak. But despite that significant level of wealth destruction, it has not been enough to depress demand. This strongly suggests that the Fed will have to double down on its tightening of monetary policy.

Household net worth more than doubled between Q4 2007 and Q4 2021, moving from $70 trillion to $150 trillion. And although there was a decline of $7 trillion over the subsequent nine months, wealth destruction hasn’t been enough to dampen demand. Again, this illustrates why the Fed is likely to become more even aggressive in hiking interest rates and destroying wealth.

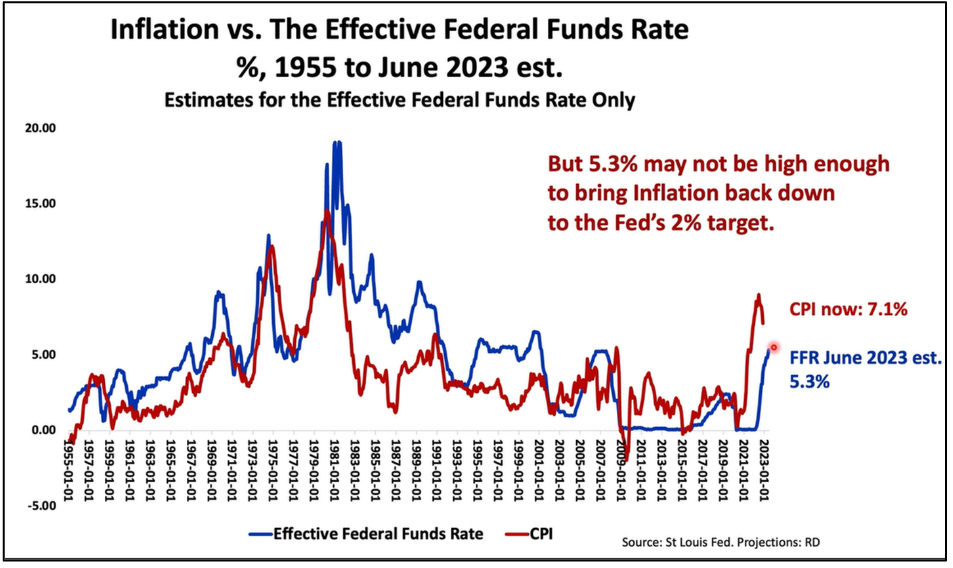

The Federal funds rate now stands at an effective 4.33%. Duncan projected that the Fed will raise rates by 25 bps four more times between now and June, bringing the Federal funds rate to a 5.33%. That would be more than double the 2.4% rate that the Fed reached in early 2019, the last time it employed a policy of rate increases.

Duncan observed that as far back as 1955, the Federal funds rate has generally been higher than the rate of inflation. Today, it is significantly below inflation. This suggests that the Fed’s actions to reduce demand are far from finished.

The Fed has two measures to tighten monetary policy – raising interest rates and destroying dollars through QT. When dollars are destroyed, liquidity in financial markets contracts, and the reduced liquidity tends to cause asset prices to fall. Currently, the Fed’s QT program is destroying almost $100 billion per month. Of course, as liquidity is reduced, the tendency is to push interest rates even higher. The combination of high interest rates and reduced liquidity places even more downward pressure on asset prices.

Reading the tea leaves of bank reserves

Following his speech, Powell was asked how long QT would continue. He replied with some highly interesting quotes:

We would allow bank reserves to decline until we are somewhat above the level that we think is consistent with scarcity.

QT causes bank reserves to decline on the liabilities side of the Fed’s balance sheet as its holdings of Treasury and mortgage-backed securities decline on the asset side.

We are not looking into going back into proving that (reserves) are scarce, because the demand for reserves is not stable. They move up and down very substantially. We want to stop at a place that is safe.

Having a lot of reserves in the system is a really good thing. It’s really a public benefit to have plenty of reserves, plenty of liquidity in the markets, and in the banking system, and in the financial system generally.

Given Powell’s focus on bank reserves, perhaps we can discern the Fed’s future actions by looking at its actions between 2017-2019, the last time it employed QT.

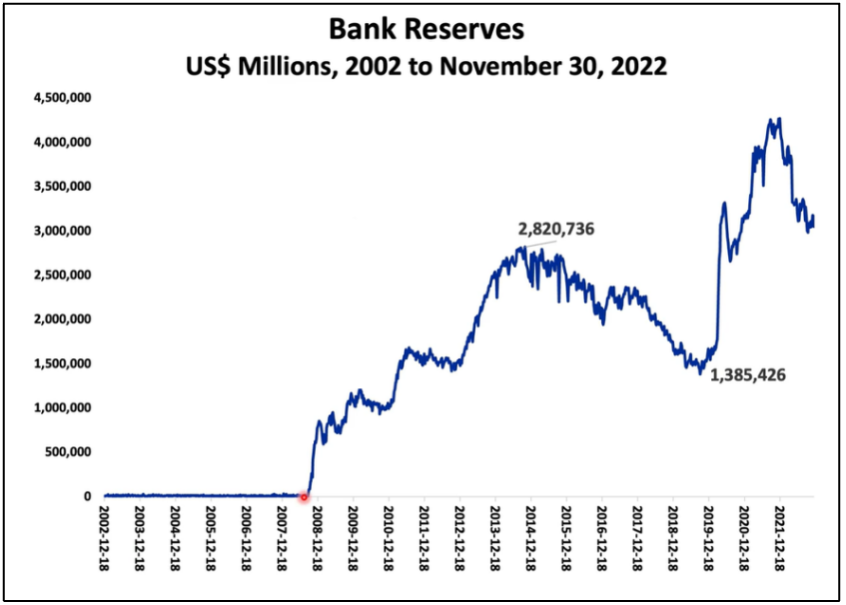

Bank reserves climb during periods when the Fed employs QE. How does this happen? The Fed pays for the bonds it purchases by making deposits into the reserve accounts that banks hold at the Fed. These deposits constitute bank reserves. (The process is reversed during periods of QT).

Prior to the 2008 financial crisis, there were almost no bank reserves. By the end of the Fed’s QE3 program, bank reserves had climbed to $2.8 trillion. Once the Fed had reversed its policy and began to employ QT, bank reserves had shrunk to about $1.4 trillion late in 2019.

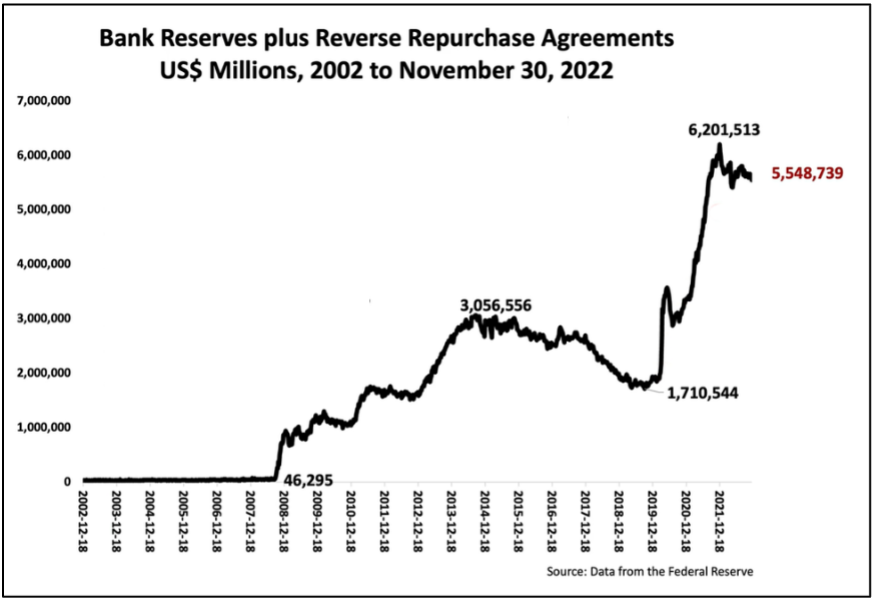

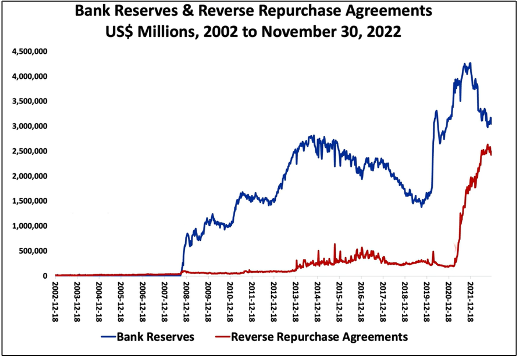

As Duncan pointed out, bank reserves represent only a part of the story. Reverse repurchase agreements (reverse repos) also play a significant role. (Last year I wrote about how the Fed used reverse repos to save money market funds from failing).

Today, reverse repos play a significant role in financial system liquidity. It was in 2013 that reverse repos became part of the liquidity picture, primarily in the context of money market funds. Their importance accelerated dramatically beginning in 2021.

Reverse repos represent liquidity in the financial markets. They appear as liabilities on the Fed’s balance sheet. As Reverse repos expand, they absorb more and more bank reserves. Adding together bank reserves and reverse repos gives us a more complete picture of total liquidity in the financial system. Combined, they totaled only $48 billion in August of 2008, but had increased to $3 trillion by October 2014. Then, due to QT, the combined total of bank reserves and reverse repos declined to $1.7 trillion by September 2019.

Duncan posed the key question, and provided the answer: Why was total liquidity of $1.7 trillion in September 2019 “too scarce?” After all, it wasn’t “scarce” in 2008 when there was only a relatively tiny amount. The reason is government debt.

One of the Fed’s key tasks is to help the government finance its debt at low interest rates. Between 2008 and 2014, the Fed created new dollars totaling $3 trillion. The money creation was used to finance the government’s debt, which skyrocketed during that period.

The Fed makes a big mistake

Let’s recall that in December of 2015, the Fed began increasing the Fed funds rate. Later, in October 2017, the Fed began to destroy dollars through QT, and did not reverse course until July 2019. By then, however, the Fed had moved too far, too fast. Liquidity had become too scarce. In September 2019, interest rates in the overnight repo market climbed to 400% of what the Fed expected. This created a crisis that forced the Fed to resume QE just two months after it had concluded QT.

After the Fed’s response to the repo crisis, COVID hit, government debt skyrocketed, and the Fed pumped additional liquidity into the financial system, eventually reaching $6.2 trillion by the end of 2021.

How much money will the Fed destroy through QT before liquidity plunges to a level that it considers scarce?

Another way of thinking about that is:

How much money will the Fed destroy before liquidity becomes too scare to finance the government’s debt at reasonable rates of interest?

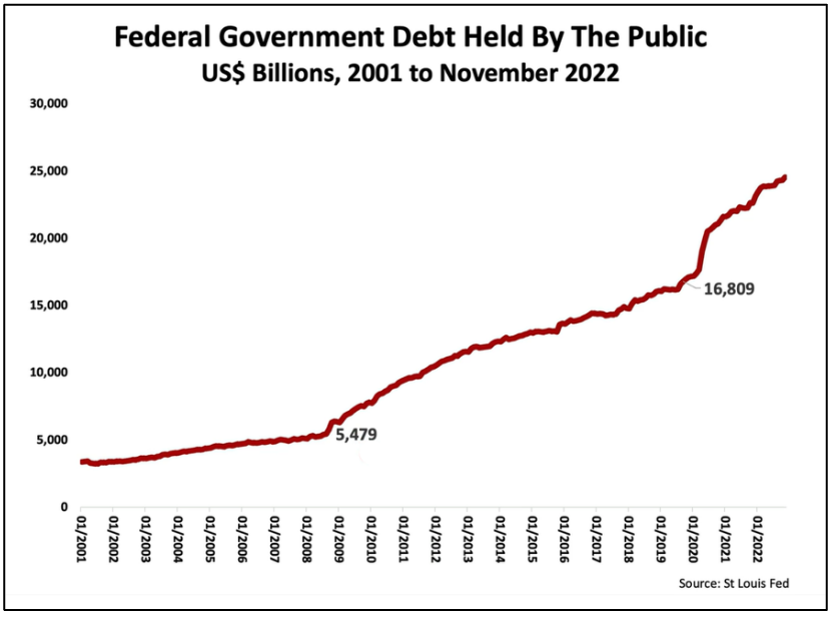

In September 2019, “too scarce” was $1.7 trillion. This time, liquidity must be significantly higher than in 2019 in recognition of all the government debt that has been added. Government debt held by the public has increased by 46% since Q3 of 2019. It now stands at $24.5 trillion.

What should you expect?

Duncan projected that QT may continue until April 2024. If that is the case, and barring some drastic unforeseen event or crisis, there is little in this picture to provide hope that asset prices will climb any time soon. On the contrary, the outlook is for higher government bond yields and significant additional equity market losses.

Financial advisors should be extra careful when working with their clients who are nearing retirement or who have recently retired. Today’s economic conditions are the worst possible for constrained investors who are subject to the threat of timing risk. Last April, I predicted today’s conditions and provided a planning roadmap to protect your clients. This is a good time to read it.

My thanks to Richard Duncan for allowing me to reproduce some of his charts. As always, I recommend that advisors subscribe to Richard’s invaluable video newsletter, Macro Watch.

Wealth2k® founder David Macchia is an entrepreneur, author, IP inventor and public speaker whose work involves improving the processes used in retirement income planning. David is the developer of the widely used The Income for Life Model®, and the recently introduced Women And Income®. David has authored many articles on the subjects of retirement income planning and financial communications. He is the author of two books, Constrained Investor®, and Lucky Retiree: How to Create and Keep Your Retirement Income with The Income for Life Model®.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives. Powell shared a chart that indicated three areas of inflation that are of particular concern: core goods, housing services and core services (less housing). While highlighting the fact that core goods inflation has fallen considerably since its 2022 peak, the opposite was happening in housing services inflation, a trend he projected would not change until the second half of 2023 at the earliest.

Powell shared a chart that indicated three areas of inflation that are of particular concern: core goods, housing services and core services (less housing). While highlighting the fact that core goods inflation has fallen considerably since its 2022 peak, the opposite was happening in housing services inflation, a trend he projected would not change until the second half of 2023 at the earliest. Powell stated that average hourly earnings increased by 5.1% in November compared to the same period in 2021. He explained that the Fed’s 2% inflation target can’t be achieved until wage growth is slowed by around 2% from its current rate of increase. For context, average hourly earnings (HRE) between 2006 and 2019 had an average monthly increase of 0.2%. Toward the end of 2022, HRE increased threefold that average, to 0.6%.

Powell stated that average hourly earnings increased by 5.1% in November compared to the same period in 2021. He explained that the Fed’s 2% inflation target can’t be achieved until wage growth is slowed by around 2% from its current rate of increase. For context, average hourly earnings (HRE) between 2006 and 2019 had an average monthly increase of 0.2%. Toward the end of 2022, HRE increased threefold that average, to 0.6%. Household net worth more than doubled between Q4 2007 and Q4 2021, moving from $70 trillion to $150 trillion. And although there was a decline of $7 trillion over the subsequent nine months, wealth destruction hasn’t been enough to dampen demand. Again, this illustrates why the Fed is likely to become more even aggressive in hiking interest rates and destroying wealth.

Household net worth more than doubled between Q4 2007 and Q4 2021, moving from $70 trillion to $150 trillion. And although there was a decline of $7 trillion over the subsequent nine months, wealth destruction hasn’t been enough to dampen demand. Again, this illustrates why the Fed is likely to become more even aggressive in hiking interest rates and destroying wealth. Duncan observed that as far back as 1955, the Federal funds rate has generally been higher than the rate of inflation. Today, it is significantly below inflation. This suggests that the Fed’s actions to reduce demand are far from finished.

Duncan observed that as far back as 1955, the Federal funds rate has generally been higher than the rate of inflation. Today, it is significantly below inflation. This suggests that the Fed’s actions to reduce demand are far from finished.

Reverse repos represent liquidity in the financial markets. They appear as liabilities on the Fed’s balance sheet. As Reverse repos expand, they absorb more and more bank reserves. Adding together bank reserves and reverse repos gives us a more complete picture of total liquidity in the financial system. Combined, they totaled only $48 billion in August of 2008, but had increased to $3 trillion by October 2014. Then, due to QT, the combined total of bank reserves and reverse repos declined to $1.7 trillion by September 2019.

Reverse repos represent liquidity in the financial markets. They appear as liabilities on the Fed’s balance sheet. As Reverse repos expand, they absorb more and more bank reserves. Adding together bank reserves and reverse repos gives us a more complete picture of total liquidity in the financial system. Combined, they totaled only $48 billion in August of 2008, but had increased to $3 trillion by October 2014. Then, due to QT, the combined total of bank reserves and reverse repos declined to $1.7 trillion by September 2019. One of the Fed’s key tasks is to help the government finance its debt at low interest rates. Between 2008 and 2014, the Fed created new dollars totaling $3 trillion. The money creation was used to finance the government’s debt, which skyrocketed during that period.

One of the Fed’s key tasks is to help the government finance its debt at low interest rates. Between 2008 and 2014, the Fed created new dollars totaling $3 trillion. The money creation was used to finance the government’s debt, which skyrocketed during that period.