Fortune Doesn’t Always Favor the Bold: The Perils of Concentrated Stock Positions

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Yet even the smartest, most determined fund picker can’t escape a host of nasty surprises. Next time you’re tempted to buy anything other than an index fund, remember this – and think again.

Yet even the smartest, most determined fund picker can’t escape a host of nasty surprises. Next time you’re tempted to buy anything other than an index fund, remember this – and think again.

– Robert Barker, “It’s Tough to Find Fund Whizzes,” BusinessWeek.com, December 17, 2001

Many successful entrepreneurs and executives who hold much of their wealth in a highly appreciated single stock (i.e., accepting uncompensated idiosyncratic risk) face a difficult financial dilemma: Sell the stock and diversify, having to pay the taxes owed, or risk catastrophic loss. Advisors can help by educating their clients on the historical evidence that demonstrates diversification is the prudent strategy.

Investors need to distinguish between two very different types of risk: good and bad risk. Good risk is the type that you are compensated for taking, with the compensation being in the form of a risk premium – greater expected (not guaranteed) returns. For example, equities are riskier than fixed-income investments. Therefore, equities must compensate investors by providing greater expected returns. The risk, of course, is that the expected does not occur. Similarly, the stocks of small-cap and value companies have been riskier than their large-cap and growth counterparts. And just as the risk of owning equities cannot be diversified away, the risk of owning small-cap and value stocks cannot be diversified away. Therefore, small and value stocks must also carry risk premiums.

In addition to the risk of equities and the risk of small and value stocks, there is another type of equity risk: the idiosyncratic risk of an individual company. Consider the case of Enron, once named by Fortune as “America’s Most Innovative Company” for six consecutive years. Its stock achieved a high of $90.75 per share in mid-2000 and then plummeted to less than $1 by the end of November 2001; it eventually declared bankruptcy. Since this type of risk can easily be diversified away, the ownership of individual stocks is one that the market does not compensate investors for taking. Thus, it is bad (uncompensated) risk. And because investing in individual stocks involves the taking of uncompensated risk, it is more akin to speculating than investing.

The benefits of diversification

The benefits of diversification are obvious and well known. Diversification can reduce the risk of underperformance. It can also reduce the volatility and dispersion of returns without reducing expected returns. A diversified portfolio, therefore, is considered both more efficient and more prudent than a concentrated portfolio. Individual stock ownership offers both the hope of great returns (finding the next Google, for instance) and the potential for disastrous results (ending up with the next Enron or FTX). Because investors are not compensated for taking the risk that their result will be disastrous – the market doesn’t compensate investors with higher expected returns for taking risks that are easily diversified away – the rational strategy is to not buy individual stocks. Unfortunately, the evidence is that the average investor, while risk averse, doesn’t act that way. In a triumph of hope over wisdom and experience, they fail to diversify.

Given the obvious benefits of diversification, the question is: Why don’t investors hold highly diversified portfolios? One reason is that it’s likely most investors don’t understand just how risky individual stocks are. To correct that lack of knowledge, we’ll review the literature. I’m confident that most investors would be shocked at the data on individual stock returns. We’ll begin with a review of the performance of U.S. stocks.

Hendrik Bessembinder contributed to our understanding of the risky nature of individual stocks with his study, “Do Stocks Outperform Treasury Bills?,” published in the September 2018 issue of the Journal of Financial Economics. His study covered the period 1926-2015 and included all common stocks listed on the NYSE, AMEX and Nasdaq exchanges. Following is a summary of his findings:

- Only 47.7% of returns were greater than the one-month Treasury rate.

- Even at the decade horizon, a minority of stocks outperformed Treasury bills.

- From the beginning of the sample, or first appearance in the data through the end of sample or delisting, and including delisting returns when appropriate, just 42.1% of common stocks had a holding period return greater than one-month Treasury bills.

- While more than 71% of individual stocks had a positive arithmetic average return over their full life, only a minority (49.2%) of common stocks had a positive lifetime holding period return, and the median lifetime return was -3.7%. This was because of volatility and the difference in arithmetic (annual average) returns versus geometric (compound or annualized) returns. For example, if a stock loses 50% in the first year and then gains 60% in the second, it has a positive arithmetic return but has lost money (20%) and has a negative geometric return.

- Despite the existence of a small-cap premium (an annual average of 2.8%), smaller capitalization stocks were more likely to have returns that fell below the benchmarks of zero or the Treasury bill rate. Just 37.4% of small stocks had holding period returns that exceeded those of the one-month Treasury bill. In contrast, 80% of stocks in the largest decile had positive decade holding period returns and 69.6% outperformed the one-month Treasury bill.

- Reflective of the positive skewness in returns, only 599 stocks, just 2.3% of the total, had lifetime holding period returns that exceeded the cross-sectional mean lifetime return.

- The median time that a stock was listed on the Center for Research in Security Prices (CRSP) database was just more than seven years.

- Only 36 stocks were present in the database for the full 90 years.

- A single-stock strategy underperformed the value-weighted market in 96% of bootstrap simulations (a test that relies on random sampling with replacement) and underperformed the equal-weighed market in 99% of the simulations.

- The single-stock strategy outperformed the one-month Treasury bill in only 28% of the simulations.

- Only 3.8% of single-stock strategies produced a holding period return greater than the value-weighted market, and only 1.2% beat the equal-weighted market over the full 90-year horizon.

- By far the most frequent one-decade buy-and-hold return was -100%.

We now turn to the international evidence.

International evidence

Jiali Fang, Ben Marshall, Nhut Nguyen and Nuttawat Visaltanachoti contributed to the literature with their study, “Do Stocks Outperform Treasury Bills in International Markets?,” published in the May 2021 issue of Finance Research Letters. Their data sample covered more than 70,000 stocks in 57 countries over the period 1996-2017. Following is a summary of their findings:

- More than half the common stocks in the majority (55 of 57) of international equity markets generated total returns less than local Treasury bill returns.

- The average cross-country proportion of stocks outperforming was 42.4% compared to 49.7% in the U.S. – individual stock underperformance was even more prevalent internationally.

- There was a sizable variation in the extent of this underperformance, ranging from as low as 30.8% in Columbia to 55.1% in Bangladesh. Switzerland, the other country with a majority of stocks outperforming, at 51.0%, was the only developed country with a slight majority of individual stocks outperforming local Treasury bills. In 18 countries, less than 40% of individual stocks outperformed their local Treasury bills.

- A greater proportion of stocks underperformed in countries with weaker governance, less individualistic investors, less openness to trade and foreign equity market investment, less financial market development and weaker economies (lower growth, higher inflation and higher unemployment).

- The results were robust to subperiod tests.

Summarizing the evidence, most common stocks do not outperform Treasury bills over their lifetimes. The research findings highlight the high degree of positive skewness (lottery-like distributions), and the riskiness, found in individual stock returns. For example, Bessembinder noted that the 86 top-performing stocks, less than one-third of 1% of the total, collectively accounted for more than half of the wealth creation. And the 1,000 top-performing stocks, less than 4% of the total, accounted for all the wealth creation. Collectively, the other 96% of stocks just matched the return of riskless one-month Treasury bills! The implication is striking: While there has been a large equity risk premium available to investors, a large majority of stocks have negative risk premiums. This finding demonstrates just how great the uncompensated risk is that investors who buy individual stocks (or a small number of them) accept – risks that can be diversified away without reducing expected returns.

A problem for successful entrepreneurs and executives

Many successful entrepreneurs and executives who hold much of their wealth in a highly appreciated single stock (taking that uncompensated idiosyncratic risk) face a difficult financial dilemma. While the high idiosyncratic volatility of a concentrated single-stock position can lead to those lottery-like returns, it also runs the much greater risk of catastrophic losses. The evidence we reviewed shows that owning a concentrated position is one of the riskiest investment strategies an investor can pursue. It is likely also highly imprudent because once you have sufficient wealth to live a comfortable lifestyle, your marginal utility of wealth falls toward zero. While more wealth is always better than less, any incremental wealth won’t improve your life in any meaningful way, but the downside risk would be unthinkable for those who seek to become guardians of wealth for themselves and their families. The problem for many people faced with this situation is that selling the stock can result in an immediate and punitive tax burden.

Loss aversion, that people often avoid a sure loss in favor of an uncertain, but probable, bigger loss, is a well-documented phenomenon in behavioral economics. As Nobel Prize winner Daniel Kahneman noted in his book Thinking, Fast and Slow: “People become risk seeking when all their options are bad.” Thus, we should not be surprised that even absent trading restrictions, many investors choose uncertain economic loss over a certain and immediate tax liability and delay diversifying their appreciated concentrated stock holdings.

The decision about how to handle concentrated stock is further complicated by other factors: rational (such as insider knowledge) and irrational (behavioral biases, such as familiarity breeding the illusion of safety, and sentimental value attached to the stock).

Nathan Sosner, author of the study, “When Fortune Doesn’t Favor the Bold: Perils of Volatility for Wealth Growth and Preservation,” published in the winter 2022 issue of The Journal of Wealth Management, developed an analytical framework – examining the mean (the average), median (the value separating the higher half from the lower half of a data sample), mode (the value that appears most frequently in a data set) and shortfall probability – for evaluating this choice and explained how it relates to classic betting strategies and economic theory.

In his analysis, Sosner assumed a volatility of 50% for an individual stock, which is about 2.7 times greater than the overall market’s historical volatility of 18.4%. While that may seem high, it is consistent with the median Barra model volatility for information technology and health care stocks in the Russell 2000 Index universe of around 55%. It is also consistent with the median annualized volatility of IPO stocks in the first five years after the IPO, which Sosner found to be in excess of 50%. He also found that the median volatility increased above 55% for smaller IPO stocks.

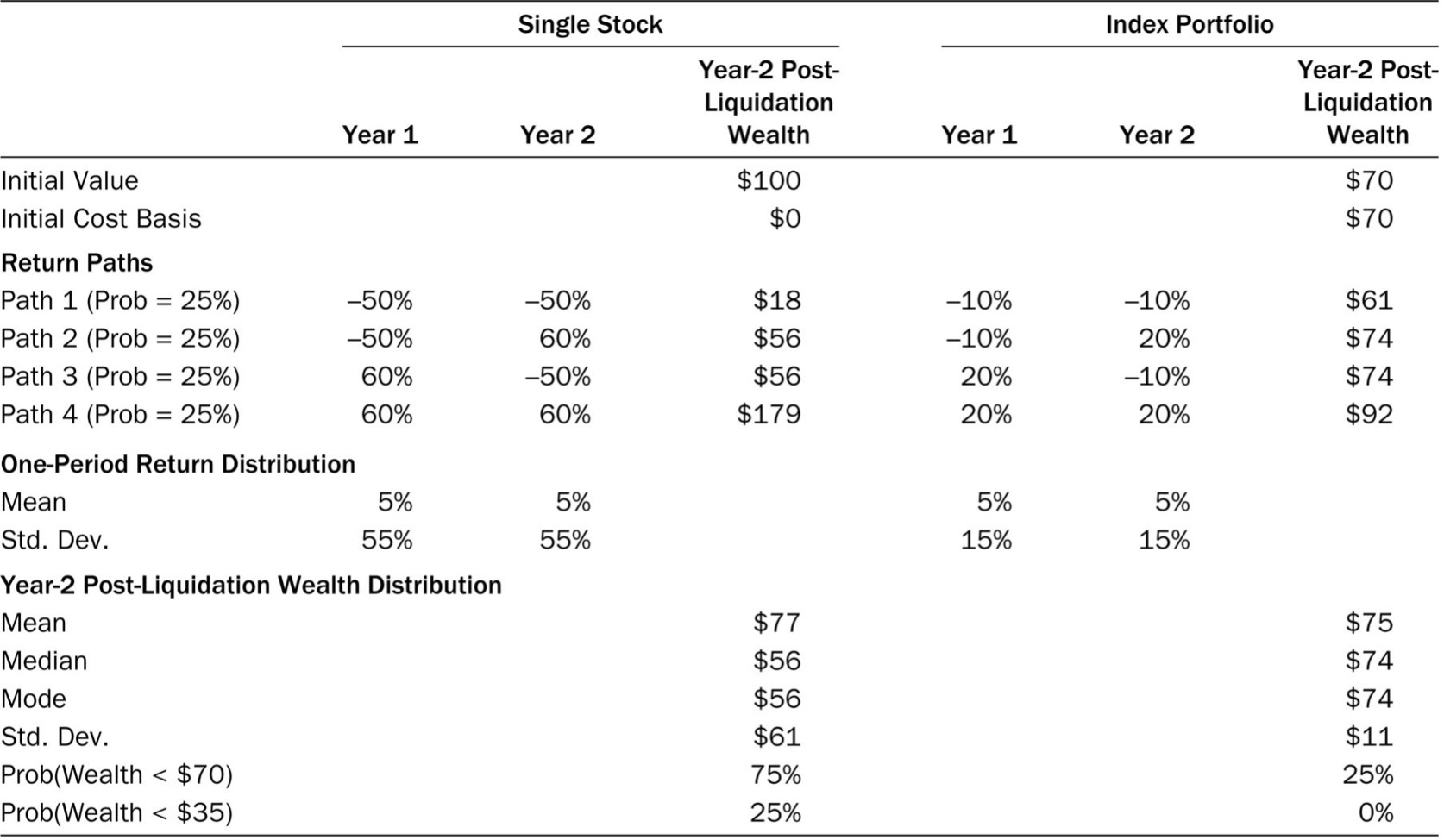

To illustrate the problem created by the high volatility of concentrated portfolios, Sosner created the following simple two-period illustration, with the capital gains tax rate assumed to be 30%:

The above example demonstrates that the distribution of wealth achieved after two periods with a highly volatile single stock investment is very different from that achieved with a lower-volatility index (diversified) portfolio in two ways: With the single-stock investment, the mass of wealth distribution is shifted significantly toward zero, and the skewness of wealth distribution is much greater (as evidenced by its long right tail). The implication is that even though sticking with a single stock position might yield a greater upside, diversifying into an index portfolio reduces the risk of a significant downside and improves the chances of wealth preservation – likely the more important objective.

With the understanding of the role of volatility, the following is a summary of Sosner’s findings:

- Due to significant positive skewness (lottery-like distribution), the best outcome under the single-stock scenario was much greater than with a diversified index portfolio. However, the lower upside of a diversified index portfolio was compensated by a significantly lower dispersion of potential outcomes, and specifically lower downside risk – improving the odds of wealth preservation.

- The urgency to diversify increases with the stock’s return volatility (and the average difference between the high and low price of a NYSE stock during a year has been about 40%, making individual stocks much riskier than the market) and the investor’s risk aversion and investment horizon.

- Mean wealth is always greater than median wealth; median wealth becomes infinitesimally small relative to mean wealth as the investment horizon increases; and the probability of wealth exceeding mean wealth converges to zero as the investment horizon increases. Mathematically, the mass of the distribution of after-tax wealth derived from a high-volatility concentrated stock is likely to shift toward zero with the investment horizon (recall Bessembinder’s finding that by far the most frequent one-decade buy-and-hold return was -100%). This puts the prospects of long-run wealth growth and preservation of capital in serious peril. Diversifying concentrated risk is essential for avoiding catastrophic loss of wealth.

- For risk-averse investors, median wealth and mode wealth are more relevant wealth distribution statistics than mean wealth, and a stock’s volatility has a primary effect on these statistics. That is why focusing on arithmetic mean returns is likely suboptimal for higher net worth investors, especially those with long investment horizons.

- The tax liability that would result from diversifying a concentrated low-basis stock has only a secondary effect on the median and mode of wealth.

- For many concentrated low-basis stock investors, it is optimal to liquidate the stock and invest the after-tax proceeds in a diversified portfolio despite the significant upfront liquidation tax burden.

- Tax-efficient techniques for disposing of concentrated low-basis stock can strike the balance between the urgency to diversify and aversion to taxes.

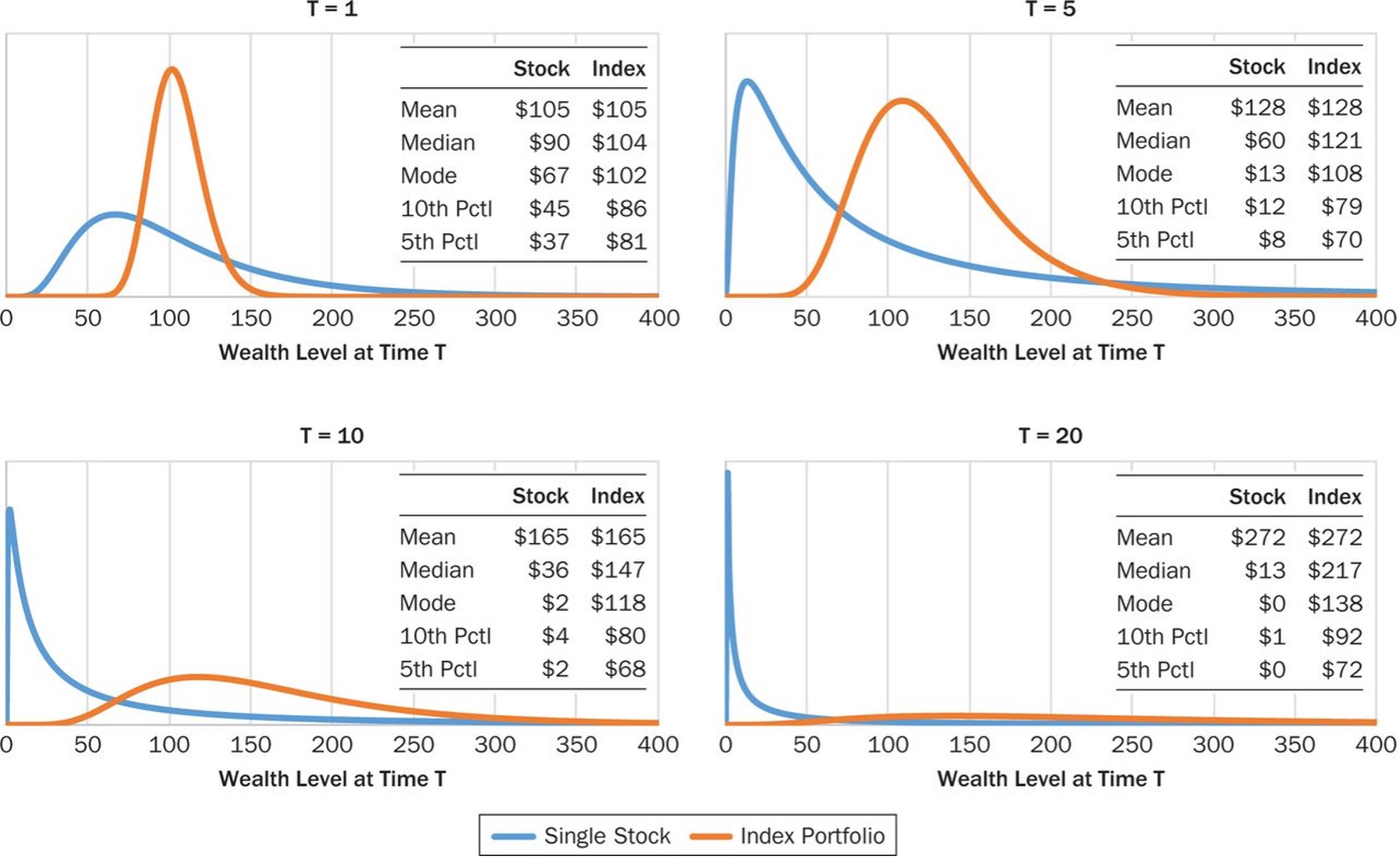

The following exhibit shows the distribution of compounded wealth achieved with a hypothetical single stock and an index portfolio and reports mean, median and mode wealth at alternative investment horizons of 1, 5, 10 and 20 years. Both the stock and index are assumed to have 5% annual arithmetic mean return. The annual return volatility for the single-stock and index portfolio is 55% and 15%, respectively. The initial invested capital is $100 for both the stock and index investment.

As you can see, as the investment horizon increases, the mass of the wealth distribution shifts to the left, with the shift being particularly pronounced for the highly volatile single stock. The author explained: “These results show yet again that mean compounded wealth (and arithmetic mean return that determines its level) is not the right quantity to focus on for a long-run investor. Depending on return volatility, mean wealth might lie far out in the right tail of the wealth distribution and might be a highly unlikely outcome to achieve. The highly volatile single stock, despite having the same arithmetic mean return and achieving the same mean wealth as the index portfolio, performs disastrously poorly based on the median and mode wealth criteria. … A lower volatility index portfolio exhibits substantially better wealth distribution properties.”

The important takeaway from his findings is that “in the long run, the distribution of compounded wealth has such a long right tail that mean wealth has little to do with what an investor can reasonably ‘expect’ as the level of her long-run compounded wealth. Whereas mean wealth is dominated by a few large positive outliers, the mass of the wealth distribution, which is better described by such statistics as median and mode, falls well below the mean.”

Sosner then shifted the analysis to the impact of taxes.

Tax considerations

Sosner began by noting: “Concentrated wealth is often a problem faced by ultra-high-net-worth families for whom estate tax exemption might shield (from estate tax) only a small part of their wealth. Such families typically transfer their wealth into trusts that shield the wealth from estate tax but do not allow for a basis step-up at death. Economically, it makes sense to give up the basis step-up in favor of avoiding estate tax. First, estate tax rates are substantially higher than long-term capital gain rates. Second, whereas realization of capital gains can be deferred, the same cannot be said about death.”

In terms of his analysis: “A fraction of a single stock position is sold down at the beginning of the investment period, a capital gains tax is paid on the liquidation gain, and the post-liquidation proceeds of the stock sale are reinvested in an index portfolio. At the end of the investment horizon, all the positions – the remaining single stock and the index – are fully liquidated, liquidation capital gains tax is paid, and the post-liquidation wealth statistics are calculated and reported.”

Sosner found that by diversifying, the investor does reduce mean post-liquidation wealth because of the upfront tax burden of liquidation. However, by diversifying the single-stock position, the investor significantly increased median and mode wealth. The probability of a substantial loss of wealth was very high for large allocations to the single stock but was reduced to close to zero for large allocations to the index portfolio. Importantly, Sosner also found: “Even when the arithmetic mean return of the stock is three times as high as that of the index, the investor maximizing median wealth or mode wealth should still liquidate most of the single stock position despite the significant upfront tax burden.” The reason is that the probability of substantial loss of wealth remains quite high with the single stock holding.

Tax strategies

Charitable and/or gifting strategies (charitable remainder trusts, private foundations, donor advised funds, etc.) are alternatives that can be used to reduce the tax impact – assuming the charitable contributions were going to be made in any event. Another option to improve tax efficiency is to consider using the combination of a variable prepaid forward (VPF) with a tax-enhanced reinvestment diversification strategy, as explained by Clifford Quisenberry and Scott Welch in their article, “Increasing the Tax-Effectiveness of Concentrated Wealth Strategies,” published in the summer 2005 issue of The Journal of Wealth Management, summer 2005.

Takeaways

Owning a single stock creates a significant drag on long-run wealth compounding in terms of a lower probability of achieving mean wealth, lower levels of median wealth and mode wealth, and a higher probability of catastrophic loss of wealth. These deleterious effects increase with the volatility of the stock and the investment horizon – the cost of delaying diversification grows rapidly over time. The reason is that volatility is deleterious for the long-run growth and preservation of wealth. The conventional wisdom that by taking the long view investors can enjoy wealth compounding over multiple decades does not apply to highly volatile concentrated stock positions – even having considered full liquidation and immediate taxation – because the risk of destroying the wealth is so great.

The evidence demonstrates that investors holding concentrated stock positions are not being adequately rewarded for the risks they are taking.

Larry Swedroe is head of financial and economic research for Buckingham Wealth Partners.

For informational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based upon third party data and may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed adequacy of this article. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio nor do indices represent results of actual trading. Information from sources deemed reliable, but its accuracy cannot be guaranteed. Performance is historical and does not guarantee future results. All investments involve risk, including loss of principal. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. The opinions expressed here are their own and may not accurately reflect those of Buckingham Strategic Wealth® and its affiliates. LSR-22-417

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Live Virtual Event: Join Now

Upcoming Virtual Events View All