Equal-weighted (EW) portfolios have outperformed market-capitalization-weighted portfolio, also referred to as value-weighted (VW) portfolios, over multiple decades across various investment universes. The simple, naive (1/N) approach of equally weighting portfolio constituents is a popular choice of academics doing research. EW’s outperformance has also attracted the interest of investors. For example, Invesco’s S&P 500® Equal Weight ETF (RSP), which like the S&P 500 Index is rebalanced quarterly, had assets of more than $33 billion as of November 2022. The fund’s expense ratio is 0.20%.

Equal-weighted (EW) portfolios have outperformed market-capitalization-weighted portfolio, also referred to as value-weighted (VW) portfolios, over multiple decades across various investment universes. The simple, naive (1/N) approach of equally weighting portfolio constituents is a popular choice of academics doing research. EW’s outperformance has also attracted the interest of investors. For example, Invesco’s S&P 500® Equal Weight ETF (RSP), which like the S&P 500 Index is rebalanced quarterly, had assets of more than $33 billion as of November 2022. The fund’s expense ratio is 0.20%.

EW portfolios have greater exposure than VW portfolios to the CAPM market beta factor and the Fama and French size and value factors because small stocks have lower market capitalizations than larger stocks, and they also tend to have higher market betas; value stocks tend to have lower market capitalizations than growth stocks. Since the beta, size and value factors have provided premiums over the long term, the greater exposure to these factors could explain EW’s outperformance.

However, other factors could be at work as well.

Alexander Swade, Sandra Nolte, Mark Shackleton and Harald Lohre, authors of the November 2022 study “Why Do Equally Weighted Portfolios Beat Value-Weighted Ones?,” investigated the long-term evidence of the equal-weighted minus value-weighted (EW–VW) return spread in a broad U.S. equity universe across multiple factor models in order to determine the source of the historical outperformance of EW portfolios. They began by noting that the EW portfolio “requires rebalancing to maintain equal weights over time. At each rebalancing date, it sells winners and buys losers and is thus considered a mean-reversion, contrarian strategy. The deterministic weighting scheme does not require any expected return or variance input and intrinsically enables diversification. Therein, a naive investor is only reliant on the average correlation coefficient to determine acceptable risk-return trade-offs.”

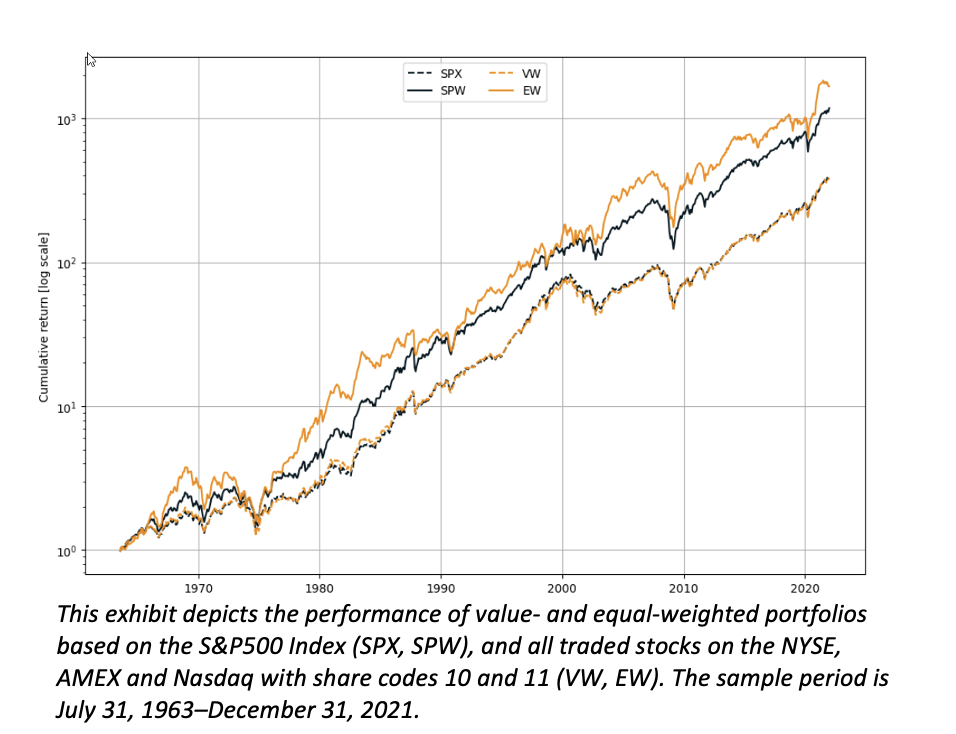

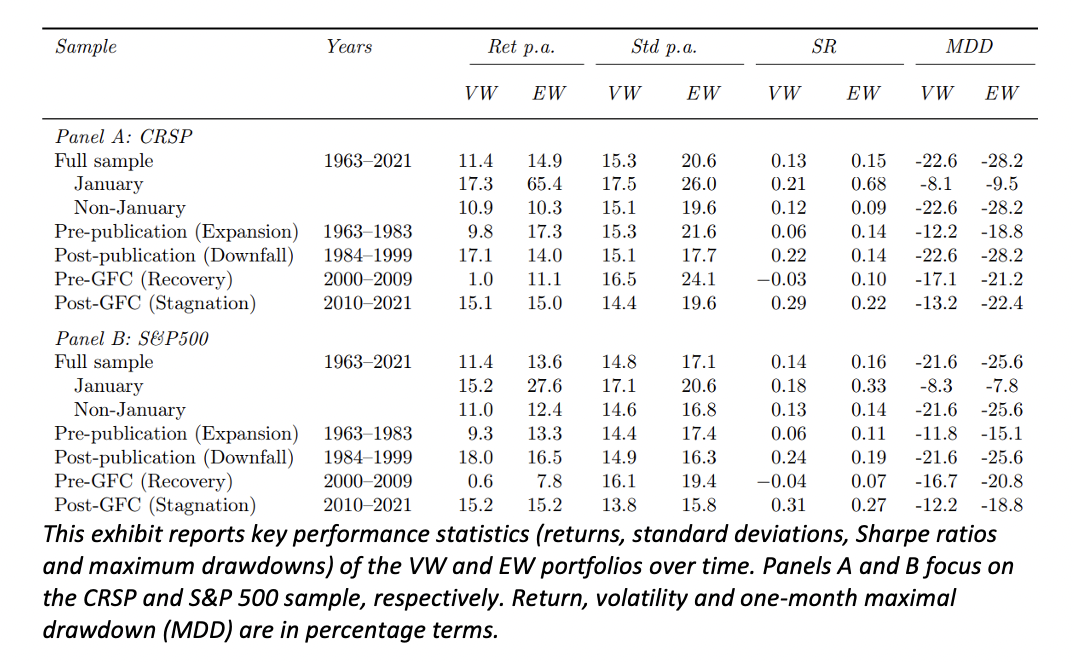

Their sample period was July 1963-December 2021, and they used monthly data from CRSP and Compustat covering stocks traded on the NYSE, AMEX and Nasdaq. Over the full period they found that in the CRSP universe, EW returned 14.9% per annum at a volatility of 20.6%; and in the S&P 500 universe, EW returned 13.6% per annum at 17.1% volatility, providing higher returns than the two VW portfolios, which showed similar annual returns (11.4%) at about 15% volatility (see Exhibit 1 below). They also found that the EW portfolios provided higher returns than their VW counterparts in 33 (37) out of the 59 years. The higher returns were accompanied by higher risks in terms of higher volatility and more severe drawdowns. However, over the full period the EW portfolios produced higher Sharpe ratios (SR), as can be seen in Exhibit 2.

Exhibit 1. Cumulative Performance EW and VW Portfolios

The authors also examined the performance of the VW and EW portfolios across various subperiods: July 1963-1983, 1984-1999, 2000-2009 and 2010-2021. As can be seen in Exhibit 2, the relative performance of the two strategies varied over time, with the EW portfolio:

- Producing higher returns and a higher SR, though experiencing a larger maximum drawdown, over both the full period and the 1963-83 and 2000-09 subperiods.

- Underperforming by all metrics over the 16-year subperiod 1984-1999.

- Producing similar returns but higher volatility, a greater maximum drawdown and a lower SR over the 12-year subperiod 2010-21.

Exhibit 2. The Effect of Equal Weighting Across Sample Periods and Universes

The varying performance across subperiods should not be a surprise because all risk strategies, including factor-based strategies, experience long periods of poor performance. If that was not the case, there would be no risk and no risk premiums (the premiums would likely be arbitraged away). Time-varying results argue in favor of factor diversification rather than concentrating exposure in a single factor, such as market beta.

Swade, Nolte, Shackleton and Lohre also examined the performance relative to various factor models and found that the EW portfolios had significant betas (β) of 1.15 (t-stat = 5.77) for the CRSP universe and 1.07 (t-stat = 5.55) for the S&P 500. The higher betas contributed to the higher returns and greater volatility of the EW portfolios. They also found that the EW portfolios produced monthly alphas (α) relative to the single-factor CAPM model. The CRSP alpha was 0.20 (t-stat = 1.67) and the S&P alpha was 0.14 (t-stat = 2.56).

The Effect of Equal Weighting Across Sample Periods and Universes

The EW–VW spread through a multifactor lens

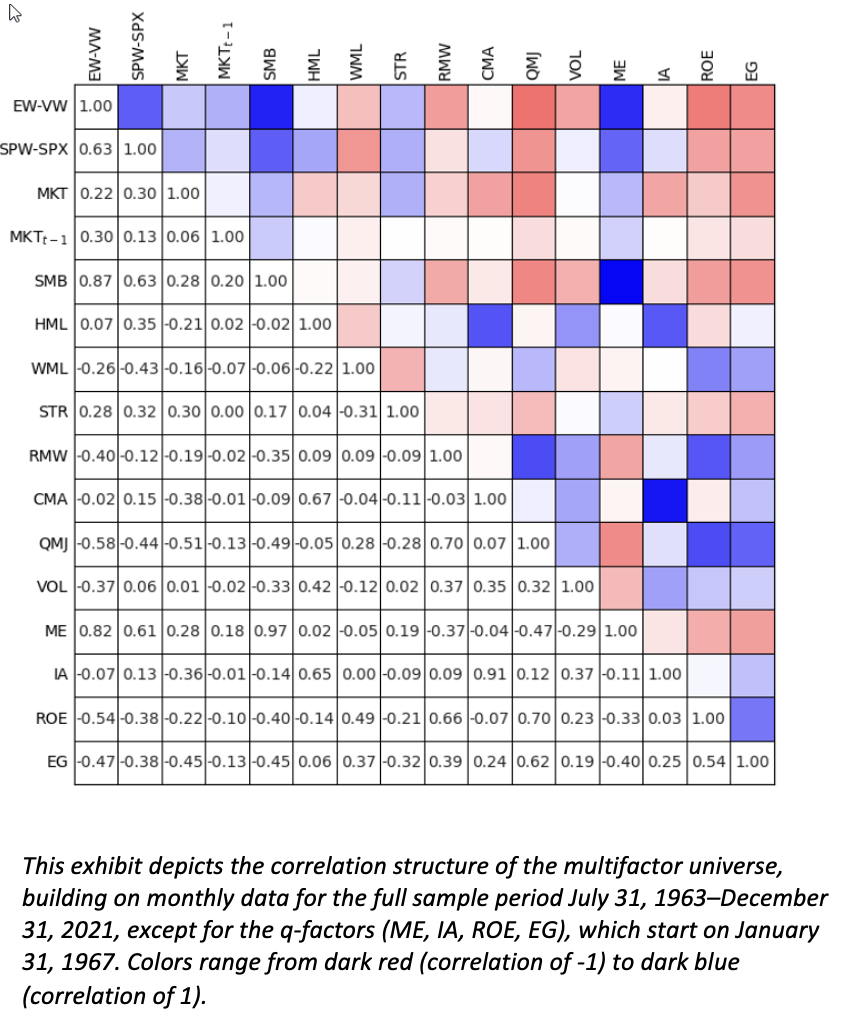

Swade, Nolte, Shackleton and Lohre also investigated the systematic drivers of the EW–VW spread with a focus on a set of common factors used among academics as well as practitioners: market equity (ME), size (SMB), value (HML), profitability (RMW), investment (CMA), momentum (WML), short-term reversal (STR), volatility (VOL) and quality-minus-junk (QMJ); and from the q-factor model, the factors of investment-to-assets (IA), return on equity (ROE) and expected growth (EG). Following is a summary of their findings on the correlation of the factors to the EW−VW spread:

- Size was highly correlated (0.87) with the CRSP EW−VW spread.

- Momentum (WML) was negatively correlated (-0.26) with the CRSP EW–VW spread (due to rebalancing), as was profitability (-0.40) and the related factors of quality (-0.58) and ROE (-0.54).

- The volatility factor (VOL) also showed negative correlations with the EW–VW spread of the CRSP sample (-0.37).

- The expected growth factor (EG) from the q-factor model was negatively correlated (-0.47) with the CRSP EW−VW spread.

- The short-term reversal factor was positively correlated (0.28) with the CRSP EW−VW spread.

Correlation Matrix for Multifactor Universe

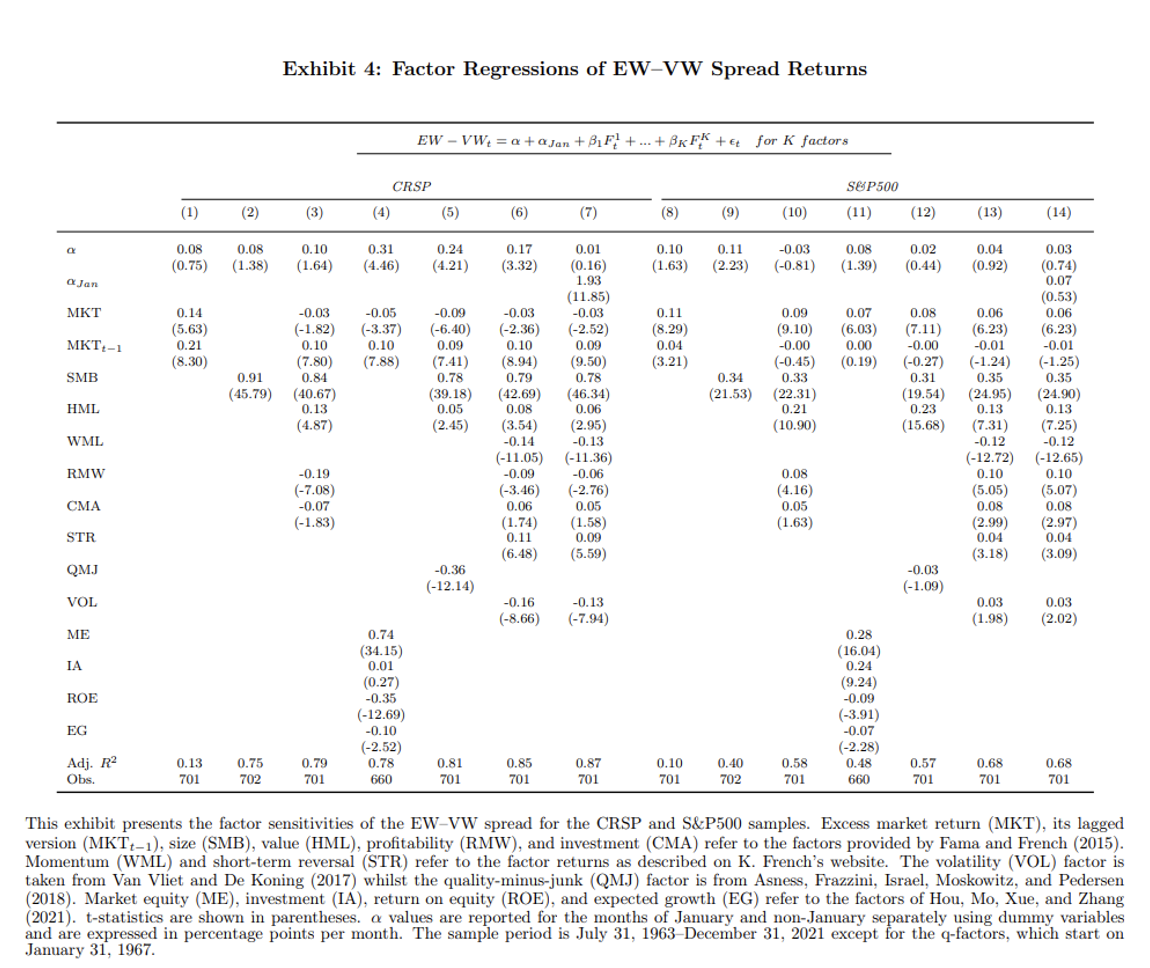

Swade, Nolte, Shackleton and Lohre next turned to analyzing the results of multifactor regressions to determine the impact of factor exposures on the EW−VW spread. They included one-month lagged market returns (MKTt−1) in their models to account for nonsynchronous trading of small stocks.

Multifactor regressions

The multifactor regressions showed:

- Significantly positive coefficients of 0.14 and 0.11 (t-stats of 5.63 and 8.29) for the market factor suggests that the average stock’s market beta was greater than 1.

- Highly significant positive loadings of the lagged market return in the CRSP universe (t-stat = 8.30) and still significant ones for the S&P 500 (t-stat = 3.21) indicated illiquidity effects among the smaller stocks in both samples.

- Regressing the EW–VW spread univariately on SMB gave an adjusted R-squared value of 75% with a highly significant t-stat of 45.79, suggesting the spread was mostly harvesting the size premium.

- Model 3, based on Fama and French’s five-factor model (ME, SMB, HML, RMW and CMA) showed that the coefficient of HML was positive but not as strong as the size factor (t-stat = 4.87), indicating that the spread might benefit from a value tilt. RMW had a negative coefficient on the EW–VW spread (t-stat = -7.08), while CMA was just statistically significant at the 10% level (t-stat = -1.83). Notably, the market factor became insignificant and negative in this model, while the one-month-lagged market factor remained significant (t-stat 7.80). The adjusted R-squared of this five-factor model was 79%, increasing the explanatory power by 4 percentage points relative to using SMB as a stand-alone factor.

- Model 4 used the q-factors and Model 5 used QMJ. The q-factor model showed similar loadings to the Fama-French (FF) five-factor model, i.e., ME was highly significant (t-stat = 34.15) and was complemented by ROE (t-stat = -12.69) and EG (t-stat = -2.52). The EW–VW spread loaded negatively on the QMJ factor (t-stat = ‑12.14), highlighting the importance to control for junk among the smallest stocks in the EW portfolio. Thus, all three models emphasized the impact of size, illiquidity and quality, but neither model offered superior explanatory power relative to the variation of the EW–VW spread, with the R-squared values ranging from 78% for the q-factor model to 81% for the model including QMJ.

- Model 6, extending the FF5 model with momentum (WML), short-term reversal (STR) and volatility (VOL) factors, increased the adjusted R-squared to 85%, with WML and VOL having significantly negative coefficients (t-stat of -11.05 and -8.66, respectively). The spread loaded positively on STR with a t-stat of 6.48. At the same time, the CMA coefficient turned from negative to positive but was only marginally significant. The size factor SMB as well as the lagged market return (MKTt−1) remained highly significant for all model specifications. They noted that “these findings resonate with the contrarian rebalancing style of the EW–VW spread which benefits from a short-term reversal effect and momentum underperforming.”

- Model 7 examined the impact of seasonality – the January effect. The regression documented strong seasonality in the EW–VW spread return, with an average January premium of 193 basis points (t-stat = 11.85) in the CRSP sample. The other factors remained significant, with size still dominating (t-stat = 46.34), followed by momentum (t-stat = -11.36). The overall adjusted R-squared increased to 87%, while the alpha of non-January returns was insignificant (t-stat = 0.16).

Having documented the systematic drivers of the EW–VW spread in the CRSP universe, the authors then examined whether their results carried over to a more investible universe – the stocks of the S&P 500 Index. They found:

- The lagged market factor virtually disappeared due to the greater liquidity of the large stocks in the S&P 500 Index.

- The SMB factor decreased across all models, though it remained highly significant. Conversely, the value factor HML increased in relevance.

- The January effect was reduced dramatically (alpha of 0.07% per month with t-stat of just 0.53).

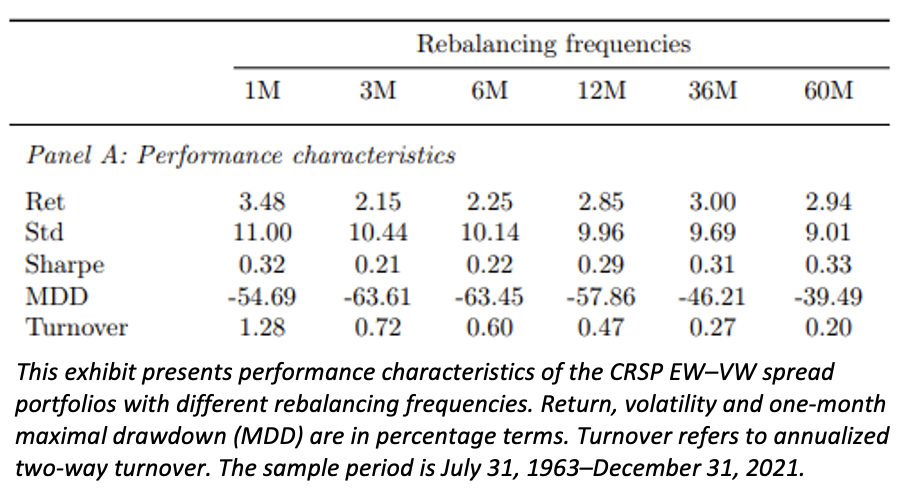

Swade, Nolte, Shackleton and Lohre next examined the impact of different rebalancing periods, from one to 60 months.

Impact of rebalancing frequency

The authors found the highest annualized return (3.48%) for the monthly rebalanced portfolio, though the highest SR was at the 60-month interval. Note also that turnover dropped monotonically as the horizon increased, reducing implementation costs, which is especially important for EW portfolios with greater exposure to small caps. In addition, the maximum drawdown was significantly smaller at the longer rebalancing horizons. Regressions showed that as the rebalancing horizon increased, factor exposures changed. For example, the size exposure was reduced, and the reduced rebalancing frequencies lowered and even inverted the negative momentum exposure of the EW–VW spread.

Investor takeaways

Historically, the equal-weighted portfolio has outperformed its value-weighted counterpart because it benefited from diversification across additional factors with historical premiums and low correlations. Swade, Nolte, Shackleton and Lohre contributed to the literature by identifying the key drivers of the EW–VW spread through the lens of different factor models. By design, the EW portfolio puts more weight into small-cap companies, which is reflected in a large exposure to small stocks relative to a VW portfolio. Also, regular rebalancing to equal weights sees the EW portfolio selling winners and buying losers, which is reflected in negative momentum exposures and a positive loading to the short-term reversal factor. On average, the EW−VW spread is long higher volatility stocks and thus is betting against the low volatility anomaly. The overweighting of small firms also results in negative quality exposure – unless a fund controls for junk.

The high turnover costs of an equal-weighted strategy was why John McQuown, the creator of the first index fund for Samonsite in 1971, eventually abandoned the strategy. While working at Wells Fargo, he used about $6 million from the Samsonite pension pot to create an equal-weight gauge tracking all the shares on the New York Stock Exchange, which then numbered around 1,500. However, the fund was not a big success. The complexity and cost of constantly reweighting the fund’s constituents was a huge drag, and in 1976 the Samsonite product was rolled into another fund that held members of the S&P 500 Index in proportion to their market values.

For those investors interested in an equal-weighted strategy, perhaps because they are seeking greater factor diversification than offered by value-weighted funds such as those replicating the total stock market or the S&P 500 Index, they can invest in the aforementioned Invesco S&P 500® Equal Weight ETF (RSP). Alternatively, investors can create their own version of an equal-weight strategy by owning a total market fund and then adding exposure to the other factors that Swade, Nolte, Shackleton and Lohre identified that explain the EW−VW spread. For example, adding exposure to Dimensional, Avantis, or Bridgeway’s small value mutual funds or ETFs would provide greater exposures to the size and value factors while also avoiding the negative exposures to the profitability, quality and momentum factors (which act as drags on returns) that the EW strategy include.

As one example, Morningstar shows that as of the end of October 2022, while RSP’s average market capitalization and P/E ratios were $34.1 billion and 14.7, Bridgeway’s Omni Small Value Fund (BOSVX) average market capitalization and P/E ratios were just $900 million and 6.3. Using the regression tool at Portfolio Visualizer, we can see that BOSVX has had much higher loadings on the common factors than does RSP: beta (1.09 versus 1.03), size (1.19 versus 0.11), value (0.68 versus 0.15), momentum (0.06 versus -0.1) and quality (0.4 versus 0.08). And their patient trading strategies would keep turnover costs at a minimum. In that way, investors get the benefits of the positive exposures to factors with historical premiums without some of the negatives of an equal-weighting strategy.

Larry Swedroe is the head of financial and economic research for Buckingham Wealth Partners.

For informational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based upon third party data and may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed adequacy of this article. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio nor do indices represent results of actual trading. Information from sources deemed reliable, but its accuracy cannot be guaranteed. Performance is historical and does not guarantee future results. All investments involve risk, including loss of principal. Mentions of specific securities are for informational purposes only and should not be construed as a recommendation of specific securities. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. The opinions expressed here are their own and may not accurately reflect those of Buckingham Strategic Wealth® and its affliates. LSR-22-416

Read more articles by Larry Swedroe

Equal-weighted (EW) portfolios have outperformed market-capitalization-weighted portfolio, also referred to as value-weighted (VW) portfolios, over multiple decades across various investment universes. The simple, naive (1/N) approach of equally weighting portfolio constituents is a popular choice of academics doing research. EW’s outperformance has also attracted the interest of investors. For example, Invesco’s S&P 500® Equal Weight ETF (RSP), which like the S&P 500 Index is rebalanced quarterly, had assets of more than $33 billion as of November 2022. The fund’s expense ratio is 0.20%.

Equal-weighted (EW) portfolios have outperformed market-capitalization-weighted portfolio, also referred to as value-weighted (VW) portfolios, over multiple decades across various investment universes. The simple, naive (1/N) approach of equally weighting portfolio constituents is a popular choice of academics doing research. EW’s outperformance has also attracted the interest of investors. For example, Invesco’s S&P 500® Equal Weight ETF (RSP), which like the S&P 500 Index is rebalanced quarterly, had assets of more than $33 billion as of November 2022. The fund’s expense ratio is 0.20%.