My research confirms what academic theory predicts: There has been no historical alpha among dividend-paying stocks, including those with a history of increasing dividends. Investors are better served by “tilting” allocations to factors that have historically outperformed (e.g., value).

My research confirms what academic theory predicts: There has been no historical alpha among dividend-paying stocks, including those with a history of increasing dividends. Investors are better served by “tilting” allocations to factors that have historically outperformed (e.g., value).

One of the more popular strategies is investing in companies with a track record of increasing dividends. S&P has even created an index of “dividend aristocrats” that measures the performance of S&P 500 companies that have increased dividends every year for the last 25 consecutive years. The Index treats each constituent as a distinct investment opportunity without regard to its size by equally weighting each company.

Asset managers are aware of the well-documented behavioral preference of investors for dividend-paying stocks – despite the fact that this behavior is an anomaly from the perspective of classical financial theory, as Merton Miller and Franco Modigliani famously established that dividend policy should be irrelevant to stock returns. As they explained, at least before frictions like trading costs and taxes, investors should be indifferent to $1 in the form of a dividend (causing the stock price to drop by $1) and $1 received by selling shares. This must be true unless you believe that $1 isn’t worth $1. This theorem has not been challenged, at least in the academic community. Catering to the investor preference for dividends, investment firms have created ETFs and mutual funds that focus on buying the stocks of the dividend aristocrats.

We can observe the popularity of such strategies by looking at the AUM of some of the leading ETFs that invest in stocks with growing dividends:

- Vanguard Dividend Appreciation ETF (VIG) with AUM of about $64 billion. The fund follows the S&P U.S. Dividend Growers Index, which is composed of large-cap stocks that have a record of raising dividends every year. Expense ratio of 0.06%.

- SPDR S&P Dividend ETF (SDY) with AUM of about $23 billion. The fund provides exposure to U.S. stocks that have consistently increased their dividend for at least 20 consecutive years and tracks the S&P High Yield Dividend Aristocrats Index. Expense ratio of 0.35%.

- iShares Core Dividend Growth ETF (DGRO) with AUM of about $23 billion. The fund provides exposure to companies having a history of consistently growing dividends by tracking the Morningstar US Dividend Growth Index. Expense ratio of 0.08%.

Is this popularity deserved? Do the funds provide superior returns, which would be a financial theory anomaly? To answer the question, I ran factor regressions (using the tool at Portfolio Visualizer) – for the longest period available – which help us understand the sources of risk and return of a fund as well as determining if the fund generated risk-adjusted alpha (outperformance after accounting for exposures to common factors).

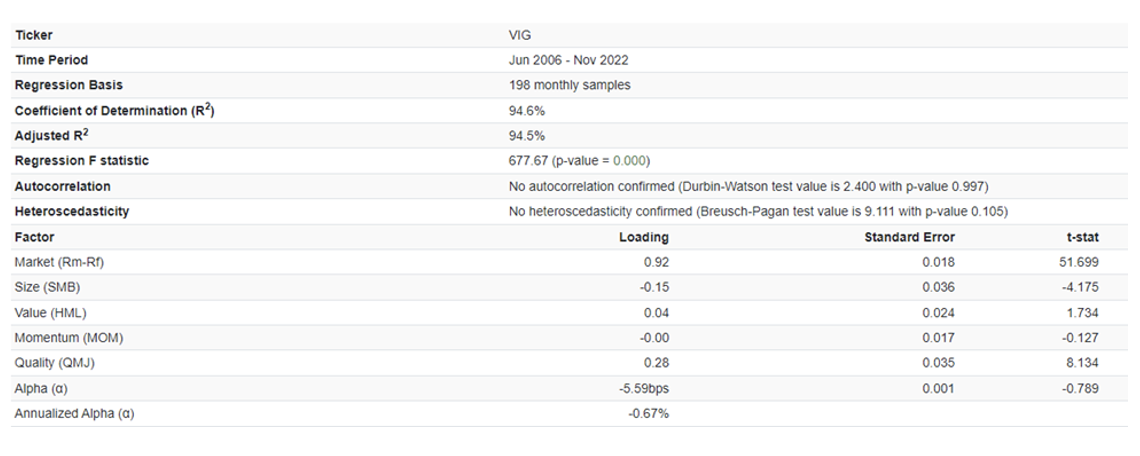

We begin with an analysis of VIG. The regression (the r-squared of 94.5% indicates that the model does a good job of explaining returns) shows that over the period June 2006-November 2022, VIG produced a statistically insignificant annualized alpha of -0.67%. The regression also shows that the fund had less exposure to the systematic risk of the total equity market (market beta of 0.92) and was tilted to large-cap and quality stocks.

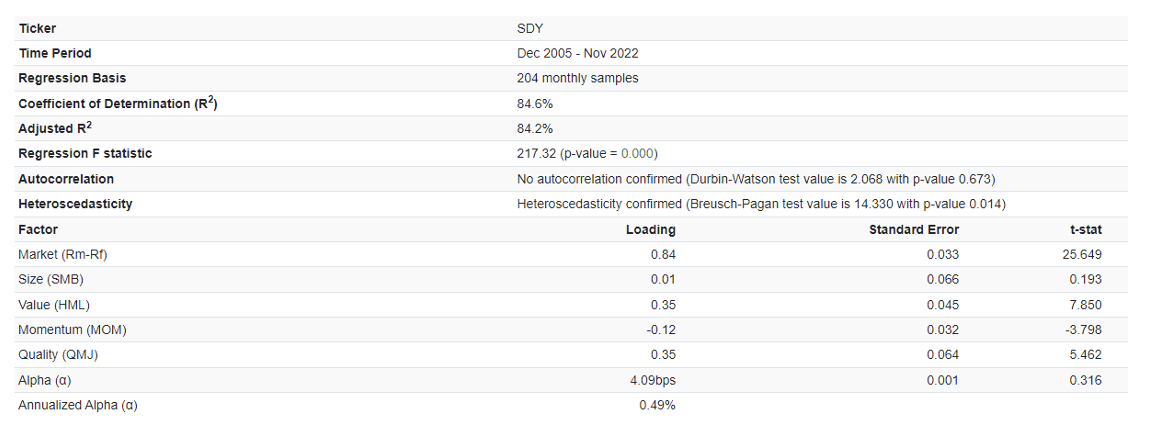

For SDY, over the period December 2005-November 2022, the fund produced a statistically insignificant alpha of 0.49% (r-squared = 84.6). The regression shows that the fund’s market beta was well below 1, and it had significant exposure to the value and quality factors, and negative exposure to momentum. Over this period, the fund produced a statistically insignificant alpha of 0.49%.

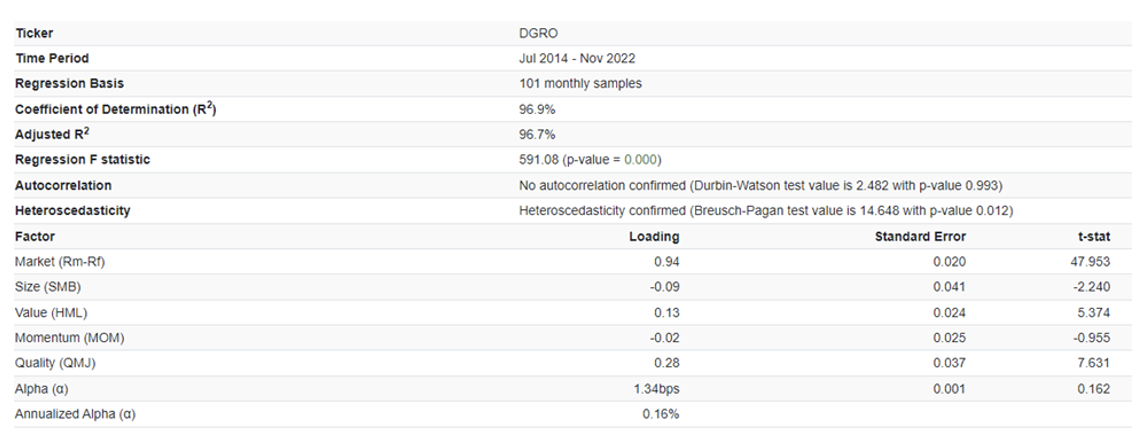

For DGRO, over the period December 2005-November 2022, the fund produced a statistically insignificant alpha of 0.16% (r-squared = 96.9%). The regression shows that the fund’s market beta was below 1, and it had statistically significant exposure to large stocks, value stocks and quality stocks.

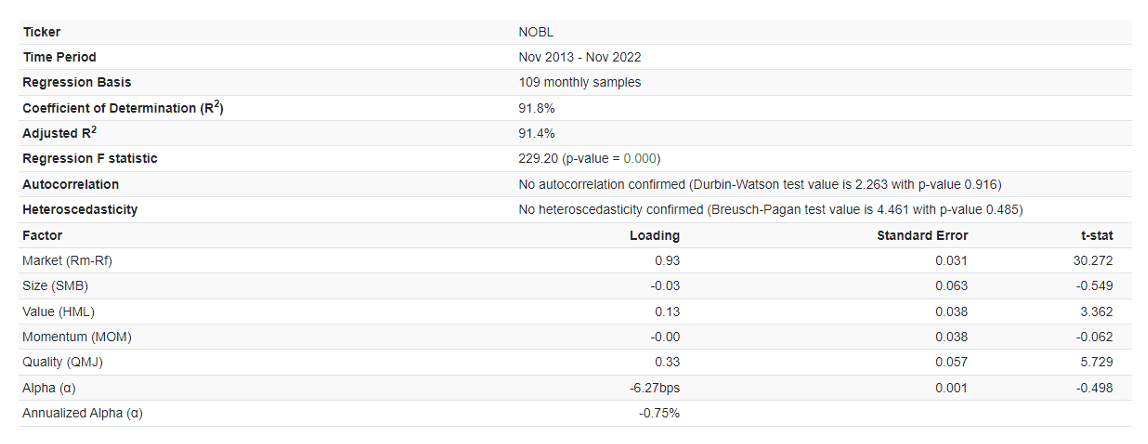

For NOBL, over the period November 2013-November 2022, the fund generated a statistically insignificant alpha of -0.75%. The regression reveals that the fund had a market beta of less than 1, and statistically significant exposures to the value and quality factors.

Summarizing my findings:

- None of the four dividend-appreciation ETFs produced a statistically significant alpha.

- The average alpha was slightly negative, at -0.19%.

- The individual funds had varying exposures to the factors that explain most of the differences in returns of a diversified portfolio. The lesson is to understand the factor exposures before investing.

Evidence consistent with theory

The lack of findings of significant alphas is consistent with the theory that dividend policy is irrelevant to returns – asset pricing models show that the exposure to common factors is the major determinant of returns. The lack of evidence might surprise many investors because it is well known that changes in a firm’s dividend can have a noticeable effect on its share price – share prices react to announcements of dividend initiations, increases, decreases and elimination. Thus, it seems likely they believe that an increase in dividends will lead to increased returns. However, that hypothesis ignores market efficiency.

The effect of repeated dividend increases on market returns

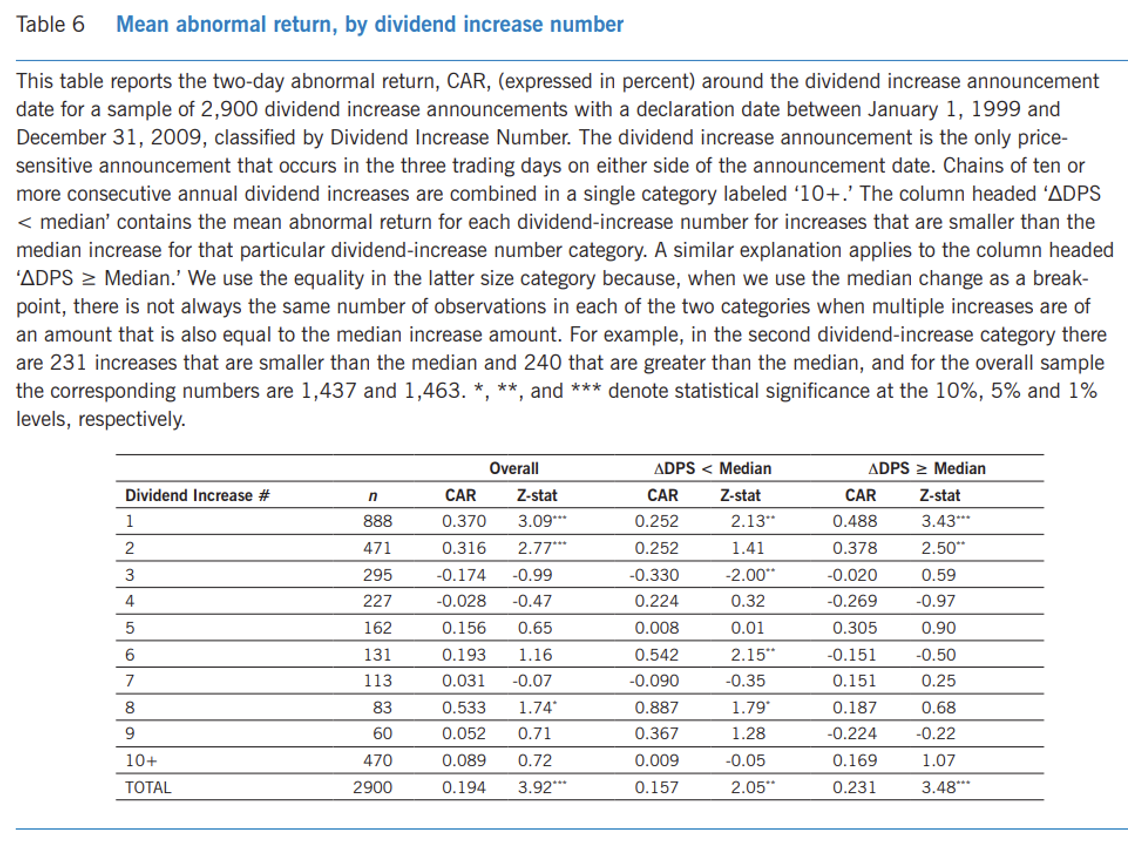

David Michayluk, Karyn Neuhauser and Scott Walker, authors of the 2014 study, “Are Certain Dividend Increases Predictable? The Effect of Repeated Dividend Increases on Market Returns,” examined the market reaction to a dividend increase for companies with a pattern of consistent dividend increases to determine if the market eventually learns to anticipate a dividend increase. They examined all taxable regular quarterly dividends declared during the 48-year period 1962-2009. They found that more than 400 firms announced their 20th or higher consecutive increase during the years 1999-2009.

They began by noting that prior research had found that, on average, stock prices increased upon the announcement of a dividend increase. Their investigation sought to determine if the abnormal returns from dividend increases are different depending on the frequency of prior dividend increases. In other words, do markets learn from a pattern of increasing dividends and anticipate them? Here is a summary of their findings:

- Abnormal returns around the first and second dividend increase announcements were significant and positive but were much less significant for the third and subsequent increases.

- The announcement of the first dividend increase was associated with a significantly positive abnormal two-day return of 0.37%, suggesting that those announcements were not anticipated. At the announcement of the second increase, the abnormal return declined to 0.32%. After that, there was no statistically significant excess return (even before expenses).

- The size of the dividend change tended to decrease as more increases occurred – larger percentage dividend changes tended to occur earlier in the sequence. That helped explain why the first two dividend increases showed significant alphas before expenses.

- Controlling for the number of prior dividend increases and firm-specific variables, only the first two dividend increases were strongly significant (before considering transactions costs) – the market had learned to anticipate future increases by the time a firm increased its dividend for two consecutive years.

- The median market capitalization tended to increase as the chain length increased – explaining the negative exposure to the size factor of the dividend appreciation ETFs.

Their findings led Michayluk, Neuhauser and Walker to conclude: “It is clear that the conventional method of analyzing dividend increases without consideration of past increases does not tell us much. Our results indicate that the market reaction to dividend increases is positive and significant for the first and second dividend increase, but then becomes insignificant for subsequent increases.”

Before concluding, we will examine the evidence on the broader question of whether investors prefer dividend payers over nonpayers.

The performance of dividend payers versus nonpayers

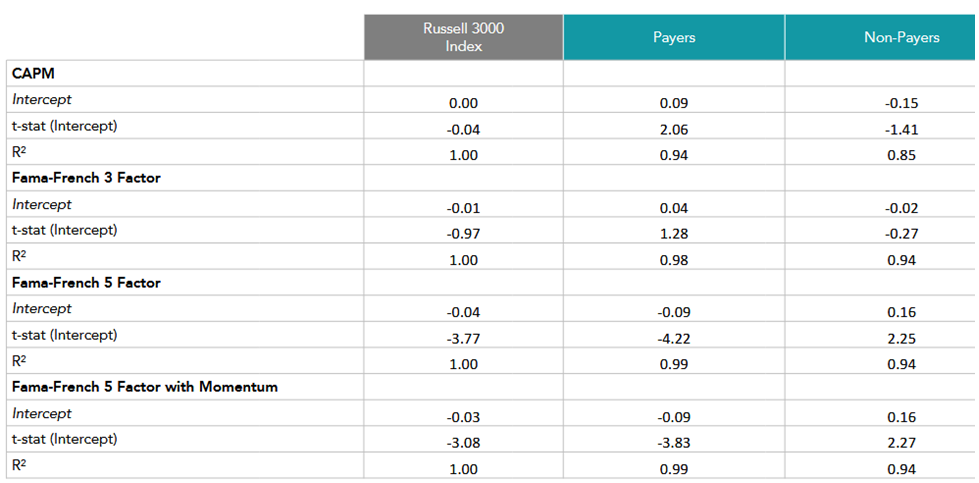

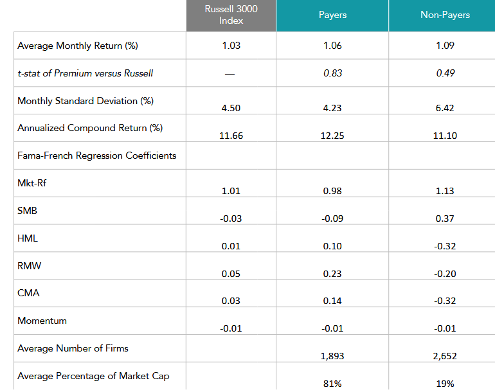

I will review the performance of U.S. dividend payers versus nonpayers over the period January 1979-October 2022. In my analysis, I will also examine exposures to the market, size, value, profitability, investment and momentum factors in the Fama-French six-factor model. As the table below indicates, the dividend payers had lower exposure to the market and size factors and greater exposure to the other factors. With that said, investors can target exposures to these factors directly without screening for dividends and will gain the benefit of having a significantly more diversified portfolio (see average number of firms and percentage of total market cap).

Past performance, including hypothetical performance, is no guarantee of future results.

Source: Dimensional, using data obtained from Ken French’s website. Fama/French five-factor returns also obtained from Ken French’s website. Firms are classified as nonpayers if no dividend was paid in the preceding 12 months. Returns are in USD. SMB, HML, RMW and CMA are factors for the premiums associated with size, relative price, profitability and investment, respectively. Frank Russell Company is the source and owner of the trademarks, service marks and copyrights related to the Russell Indices.

Without controlling for the factor exposures, while the dividend payers had lower monthly returns (1.06% versus 1.09%), the significantly higher monthly volatility of the nonpayers (6.42% versus 4.23%) resulted in the dividend payers having a higher annualized compound return (12.25% versus 11.10%).

The following table covers the same January 1979-October 2022 period but now controls for exposures to various models: the single-factor CAPM, market beta; the Fama-French three-factor model, which adds size and value; the Fama-French five-factor model, which adds profitability and investment; and the Fama-French six-factor model, which adds momentum. If the intercept is positive (negative), it shows that after controlling for those factors, the category outperformed (underperformed). A t-stat greater than 2 (3) indicates statistical significance at the 5% (1%) confidence level. The intercepts show monthly returns.

To begin our analysis, note the extremely high r-squared values, indicating the models did a good job of explaining performance. As factors were added, the explanatory power improved. If profitability was not controlled for (neither the CAPM nor the Fama-French three-factor model control do so), the dividend payers generated alpha – though the alpha was only significant against the CAPM, not against the Fama-French three-factor model. However, once profitability was included (along with other factors), the alphas of the dividend payers turned negative and with much greater statistical significance. On the other hand, the alphas of the nonpayers, while negative relative to the CAPM and Fama-French three-factor models, were positive once profitability and the other factors were included and were significant at the 5% level.

Investor takeaways

Be skeptical of strategies that conflict with economic theory. Even without considering the negative tax implications of a dividend-paying stock (versus a stock that provides all its returns in the form of capital gains, allowing investors to benefit from the potential additional growth in investment by paying taxes only when the investment is sold), investors are better served by directly targeting factor exposures in their portfolio rather than using a dividend screen, which reduces the investable universe significantly because only about 40% of stocks pay dividends. Investors screening for dividends are excluding about 60% of the eligible stocks and about 20% of the total market capitalization.

All else equal (such as factor exposures), a portfolio that is less diversified is less efficient. And instead of screening for dividends, investors can screen out the stocks with characteristics shown to negatively impact the performance of the nonpayers. Among them are a group of stocks that have “lottery-like” return distributions: so-called “penny stocks,” stocks in bankruptcy, IPOs and growth stocks (high P/E stocks) with both high investment and low profitability.

Larry Swedroe is head of financial and economic research for Buckingham Wealth Partners.

For informational and educational purposes only and should only be construed as specific investment, accounting, legal, or tax advice. Certain information is based on third party data and may become outdated or otherwise superseded without notice. Third-party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio nor do indices represent results of actual trading. Information from sources is deemed reliable, but its accuracy cannot be guaranteed. Performance is historical and does not guarantee future results. All investments involve risk, including loss of principal. By clicking on any of the links above, you acknowledge that they are solely for your convenience and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed adequacy of this article. The opinions expressed by featured authors are their own and may not accurately reflect those of Buckingham Strategic Wealth® or its affiliates. LSR-23-461

Read more articles by Larry Swedroe

My research confirms what academic theory predicts: There has been no historical alpha among dividend-paying stocks, including those with a history of increasing dividends. Investors are better served by “tilting” allocations to factors that have historically outperformed (e.g., value).

My research confirms what academic theory predicts: There has been no historical alpha among dividend-paying stocks, including those with a history of increasing dividends. Investors are better served by “tilting” allocations to factors that have historically outperformed (e.g., value).

Past performance, including hypothetical performance, is no guarantee of future results.

Past performance, including hypothetical performance, is no guarantee of future results.