The Dilemma That Isn’t: Bonds versus Bond Funds

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits“Things are not always as they seem; the first appearance deceives many.” – Phaedrus1

“I’m not what I appear to be.” – John Lennon and Paul McCartney

Should investors build their own portfolios of bonds, or buy shares of bond funds? Is there an economic difference or just one of appearance? Are directly held bonds safer because they mature, and you get your money back? How should one decide?

Let’s ask the experts. Their differing views frame the question. Then, I’ll provide my answer.

“You get your money back”

Many investors and their advisors favor individually assembled portfolios of bonds, usually “laddered” so that each bond matures at a different time, providing a predictable stream of cash. Annette Thau, a former municipal bond trader and author of The Bond Book, expressed the traditional argument in favor of holding individual bonds:

While you can invest in any sector of the bond market either through a bond fund or by buying individual bonds, the two are radically different investments.

The main difference is that an individual bond has a definite maturity date, and a fund does not. If you hold a bond to maturity, on that date it will be redeemed at par, regardless of the level of interest rates prevailing on the bond’s maturity date. Assuming a default has not occurred, you get back 100% of your principal. You have also earned a predictable income for the period that you have held the bond, consisting of coupon interest and, if coupons were reinvested, of interest-on-interest.2

I contend – and I have much support from other experts, whom I cite below – that getting your money back is, in economic terms, exactly like not getting your money back (and instead selling the bond or bond fund when you want the cash).3

Another related, but distinct, argument favoring the ladder has to do with volatility. In her balanced, pro-and-con treatment of the issue, Schwab’s Kathy Jones wrote:

[A] downside to owning bond funds is...[that] the net asset value (NAV) will fluctuate with the market: As interest rates rise and fall, the NAV of a given bond fund will fall and rise respectively, and there’s no certainty as to what the NAV may be at a point in the future. This makes bond funds less attractive than individual bonds when planning for future liabilities.4

But there is no substance to this argument. The value of your individually selected bonds rises and falls in the same way that the NAV of a bond fund does. You may not observe the price variation directly, but that doesn’t mean it’s not happening. More on that below.

Real versus nominal

When you do get your money back at the time a bond matures, you only get it back in nominal terms. The real, or inflation-adjusted, value of the money you get back is not knowable until the moment you get it. Thus, the apparent safety in a bond maturing and returning your original investment is an illusion, because only real returns matter. Ben Carlson, author of the delightful Wealth of Common Sense blog,5 expresses this concept pithily:

“Getting your money back” at maturity might be a wonderful emotional hedge but it’s not like you’re any better or worse off. When rates go up, the value of all bonds goes down, whether you’re holding an individual bond or a bond fund.

While holding to maturity does allow you to get your principal value back at par, in an environment of higher rates and inflation you will still be getting back nominal dollars that are worth less at the time of maturity [than they were when you bought the bond].

For example, let’s say you own a bond fund that yields 2% and rates [then] go to 4%. If the duration of those bonds is 5 years, you would expect that fund to fall something like 10% in value.... [L]et’s [now] say you then decided to sell your bond fund but then buy all of the individual bonds in that fund which now collectively yield 4% and hold them to maturity.

Are you better off now or not? No – you’re in the exact same place either way!

The reason, which Carlson didn’t need to state because it was too obvious, is that the bonds you’re buying have gone down by exactly as much as the bonds you’re selling. The value of a package of securities (bonds or anything else) is the same whether or not you open the package and see what’s inside.

On the other hand...

Transaction costs can be minimal for a self-managed bond portfolio.

Some of the advantages of managing your own bond portfolio are real. One is that transaction costs, as measured, can be managed to exactly zero by buying only U.S. Treasury bonds – directly from the Treasury when originally issued (that is, not in the secondary market) – and holding them to maturity. I emphasize “as measured” because nobody works for free, so the Treasury’s cost of distributing bonds to the public is paid somewhere along the line. This cost should, logically, be impounded in the bond’s yield, which would be slightly higher if there were no such cost.

This cost savings, if it exists, applies only to Treasury bonds. Higher-yielding corporates and tax-exempt municipal bonds must be bought from a broker-dealer. (A few municipal issues can be bought directly from the issuer, avoiding transaction costs.) This is an important consideration because a Treasury-only portfolio isn’t right for everybody.

Manager fees and expenses

Second, and important for any investor, is the matter of manager fees and expenses. Bond portfolio managers don’t work for free – their paychecks can be quite generous – and they have high-priced expenses such as data feeds, office space, and the legal and administrative costs of setting up a fund. All these costs are reflected in fund expense ratios that range broadly. Individuals building their own bond portfolios don’t pay those fees or expenses, other than the value of their own time and effort; this can represent a considerable cost savings, especially relative to a high-expense-ratio fund or ETF. Fund fees and expenses are cumulative and add up over long time periods.

Index funds and passive ETFs are, of course, the cheapest options: Vanguard’s intermediate-term Treasury bond index fund has a rock-bottom expense ratio of 0.07%, or $700 per year per million dollars invested.6 Adding non-Treasury bonds increases the expense ratio, as does active management. The large, actively managed total-return bond funds, which include many types of bonds, not just Treasury securities, have expense ratios of 0.40% to 0.50%, so there is a bigger hurdle to produce alpha (outperform an index fund).

Bond index funds and index ETFs with expense ratios of 0.10% or lower are so economical that it’s hard for advisors to save money with a do-it-yourself approach (unless the advisor has a very large account). Do-it-yourself costs are largely independent of account size, so costs loom larger as a percentage of asset value for smaller accounts, tipping the balance for such accounts in favor of a bond fund.

A third, very minor advantage to a self-managed portfolio is that you can express your tastes and preferences, for example regarding ESG criteria, by buying or avoiding specific bonds. A bond fund manager is selecting the bonds that he or she thinks will please their customer base, not you alone.

Moreover, diversification in the bond market isn’t as beneficial as in the stock market. Most bonds of similar duration and credit quality move together. For this reason, a portfolio of just a few bonds can capture most of the return available in the bond market. This isn’t exactly an advantage of buying bonds individually, but it puts that strategy at less of a disadvantage than if you needed a large bond portfolio to achieve diversification.

Finally, there is some psychological benefit to knowing exactly when the cash will come in and how much it will be (in nominal terms of course). It’s important to know that, if you do this, you haven’t reduced or eliminated inflation risk, which is the most important risk when holding a bond portfolio.

Vanguard’s perspective

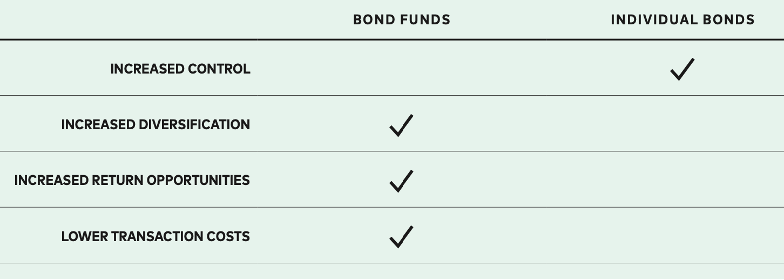

A detailed Vanguard report7 comparing individually held bonds with bond funds began by making the same getting-your-money-back, diversification, and transaction-cost arguments as those I made above. It summarized by noting the following advantages for each strategy:

What’s the advantage of control if you have to sacrifice diversification, “return opportunities” (Vanguard’s claim of being able to add alpha or to buy bonds that most individuals cannot), and transaction-cost efficiency to get it? The Vanguard authors don’t find that control gives much benefit in bond selection or asset-liability cash-flow matching, but they make some valid points regarding taxes:

Because clients directly own the bonds in... a laddered bond portfolio, as their advisor you can use any net losses from individual bond positions for tax purposes to partially offset your client’s earned income or to offset realized capital gain liabilities from other investments.

You can’t do that with a mutual fund or ETF. However, Vanguard points out that:

[a] fund uses realized losses against realized gains and carries forward any excess losses to be used against future gains. Although this may defer the pass-through of losses, it provides long-term tax efficiency to the pooled structure. In addition, as the advisor, you have a further option: You can sell your clients’ fund shares to realize a loss where applicable.

Control doesn’t turn out to be much of a win from that perspective.

But there’s a subtle advantage to individually held bonds that applies to investors who are subject to the alternative minimum tax, or AMT: “the portfolio can be tailored to bonds that are exempt from AMT, or specific to issues from your client’s home state.” More importantly, the realization of capital gains and losses on individual bonds can be timed by the advisor to reduce AMT liability.8

What would Cliff Asness do?

When I can’t quite find the right words to express a concept in investment management, I often turn to Cliff Asness, who has a gift of gab (sometimes acerbic) that is unmatched in our business. In his award-winning Financial Analysts Journal article, “My Top Ten Peeves,” Asness admitted that the perception of bonds being safer than bond funds “may even be helpful to investors” – but it is a misperception nonetheless. His star power was evidenced by the FAJ giving Asness one of its top awards for a list of “peeves” rather than for the quantitative research that the magazine is known for. He writes:

Bond funds are just portfolios of bonds marked to market every day. How can they be worse than the sum of what they own?

They could be. Structure matters. An ETF is better for most taxable investors than a 1940 Act mutual fund. Individual bonds can help with the tax problems noted above. But, in the general case, the bond fund is not worse than the sum of the bonds it owns. It’s not better. It’s the same.

Asness next repeated some of the arguments I made earlier, on which Carlson and the Vanguard authors elaborated. He then brought up a new angle:

Those believing in the fallacy [of individual-bond superiority] often also assert that another negative feature of bond funds is that “they never mature” whereas individual bonds do. That’s true. I’m not sure why anyone would care, but it’s true. But the real irony is that it’s only true for individual bonds, not the actual individual bond portfolio these same investors usually own. Investors in individual bonds typically reinvest the proceeds of maturing bonds in new long-term bonds... In other words, their portfolio of individual bonds, each of which individually has the wonderful property of eventually maturing, never itself matures. Again, this is precisely like the bond funds that they believe they must avoid at all costs.

Getting your money back is exactly like not getting your money back.

How, then, might the misperception of individual-bond superiority be helpful to investors, despite its illogic? “It’s possible,” Asness wrote, “that the false belief that individual bonds don’t change in price each day like a bond fund… [leads] to better, more patient investor behavior.” In other words, waiting for a bond to mature may have the unintended side effect of getting you not to trade, while an investor observing the vagaries of a bond fund’s NAV might trade more often. Not trading beats trading, and patience is a virtue.

Conclusion: Bond funds usually win

Returning to the epigraph – appearances can differ greatly from reality – a bond fund looks quite unlike a bond. A bond fund is a perpetual investment, like a stock fund, from which the investor can only exit at whatever the market price is at the time. The cash flows in and out of the fund are affected by the whims of the other fund shareholders.

A bond, in contrast, is a time-limited investment with a schedule of cash flows that are guaranteed by the balance sheet of the issuer. There are no interim cash flows triggered by other people. These two investments, a bond fund and a bond, then, are obviously quite different.

But that is the wrong comparison! Nobody holds a single bond – at least I hope they wouldn’t. Individual investors who hold a homemade, laddered portfolio of bonds are simply managing a one-customer bond fund. They are doing what professional bond portfolio managers do:

- selecting the bonds based on their duration, credit quality, and other characteristics;

- laddering them to provide the desired cash flow pattern;

- reinvesting coupons and principal repayment into new bonds, or into additional holdings of bonds that are already in the portfolio;

- investing new money (cash inflows) into the bond market; and

- paying out cash as desired by the asset owner.

That’s a lot of work, as any bond portfolio manager will tell you. Many individual investors have simplified the job somewhat – typically by buying only Treasury issues and limiting themselves to the lower but safer yields that come from a government guarantee – but they are still doing the bond portfolio manager’s job themselves. Whether that is an efficient use of their time and talent, relative to the cost of a commercially available bond fund, is for the investor to decide. The investor must also decide who is likely to do a better job, the amateur or the professional.

For most investors under most circumstances, the professional wins.

Laurence B. Siegel is the Gary P. Brinson Director of Research at the CFA Institute Research Foundation, the author of Fewer, Richer, Greener: Prospects for Humanity in an Age of Abundance, and an independent consultant. His latest book, Unknown Knowns: On Economics, Investing, Progress, and Folly, contains many articles previously published in Advisor Perspectives. He may be reached at [email protected]. His website is http://www.larrysiegel.org.

1Phaedrus is a character in Plato’s book Phaedrus, and is based on a real person of the same name with whom Plato engaged.

2Quoted at https://www.bogleheads.org/wiki/Individual_bonds_vs_a_bond_fund. The original source is Thau, Annette. 2011. The Bond Book, Third Edition, New York: McGraw-Hill.

3I’m indebted to that gifted satirist and smartass, the late P. J. O’Rourke, for this expression – but he was talking about the Social Security trust fund: “Having a Social Security trust fund is exactly like not having a Social Security trust fund,” his summary, in a speech, of the argument he made in Parliament of Whores, 2003, pp. 211-220. (I’m quoting from memory; I heard the speech at the Heartland Institute, September 15, 2016.)

4https://www.schwab.com/learn/story/bonds-vs-bond-funds-which-is-right-you

5https://awealthofcommonsense.com/2022/11/owning-individual-bonds-vs-owning-a-bond-fund/

6This is for the Admiral class of shares, which has a $50,000 minimum investment. The Investor class, with a much lower minimum, has a 0.20% expense ratio.

7Dinucci, Ted, Chris Tidmore, and Chris Pettit. 2022. “Individual bonds versus bond funds: Our thoughts on the advisory practice and client outcomes.” Vanguard Investment Advisory Research Center (October), https://advisors.vanguard.com/iwe/pdf/FAIBVBF.pdf

8The AMT advantage accruing to individually held bonds applies only to taxable investments, not to bonds or bond funds held in a tax-deferred (IRA or 401k) or tax-exempt (Roth IRA) accounts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All