I Don’t Like the Fed

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

And neither should you.

It’s too secretive, unpredictable, unaccountable, insular, powerful, short-sighted, irresponsible, partisan, reckless, doctrinaire, and worst of all?

Ineffective.

We can’t wish it away, sadly. Since the Federal Reserve Act established the Fed by an act of Congress just two days before Christmas, 1913, on a near party-line vote – Democrats for, Republicans against – we are stuck with it.

The gulf between left and right still lingers. Pew Research found 54% of conservatives were unfavorable of the Fed, while only 40% of moderates/liberals leaned unfavorable. Why? Perhaps because although the Fed is an invisible hand, it’s the wrong invisible hand (to the right) – the hand of government.

The Fed consists of three parts, the Board of Governors, the regional Reserve Banks, and the Federal Open Market Committee (FOMC). It’s a good job. The Federal Reserve Board pays an average salary of $1,763,605 to its board members. You may have no issues with what else the Fed does – regulate and supervise banks, bully Congress, research, manage, advise… that is, other than control the money supply and set interest rates, so-called monetary policy.

The Fed has a dual target imposed by Congress: maximum employment and price stability. The employment mandate is not measured by a fixed percentage. However, the price stability (inflation) mandate is 2%. When either stray from their range the Fed steps in.

Think of the economy as a fireplace. There are only two fuels one can add to a fire – wood and air. Wood is money; air is interest rates. To put out the fire, remove same. The Fed adds or subtracts money into the economy through its member banks by selling or buying bonds respectively. It raises and lowers the interest rate it charges these member banks, the Federal funds rate. Member banks lend to non-member banks, those banks accordingly lend to businesses and individuals, and this is how the economy is stimulated or suppressed.

The Fed’s mandate is to fix the problems it caused

About the Fed funds rate: Why did the Fed raise it so fast – the third fastest in 70 years – and did it work?

From March 2022 to March 2023, the Fed raised rates by 4.75%. Over this period, the consumer price index (CPI) dropped from 8.5% to 6% YOY.

Before you hang the Medal of Honor around Fed Chairman Jerome Powell’s neck, as Charlie Bilello, chief market strategist, Creative Planning, Tweeted: “Hiking rates to bring down inflation is not a “policy mistake,” it’s the Fed's mandate. The true policy mistake was believing that 0% rates, buying billions of mortgage bonds in a housing bubble, & increasing the money supply by 40% in 2 yrs would have no negative consequences.”

Any other consequences? If you consider the second (First Republic), third (SVB), and fourth (Signature Bank) largest bank failures in history a problem, yes. Jim Bianco, president of Bianco Research LLC Tweeted on March 28, “There are 4,000+ banks in the U.S. Some are flying closer to the sun than others. This is always the case. Not every bank is healthy; not every bank is sick. So, when you jack rates 500 bps over one year, those closest to the sun will get pushed into it and fry…You have to expect this when you pressure the financial system.”

Any other consequences? If you consider the second (First Republic), third (SVB), and fourth (Signature Bank) largest bank failures in history a problem, yes. Jim Bianco, president of Bianco Research LLC Tweeted on March 28, “There are 4,000+ banks in the U.S. Some are flying closer to the sun than others. This is always the case. Not every bank is healthy; not every bank is sick. So, when you jack rates 500 bps over one year, those closest to the sun will get pushed into it and fry…You have to expect this when you pressure the financial system.”

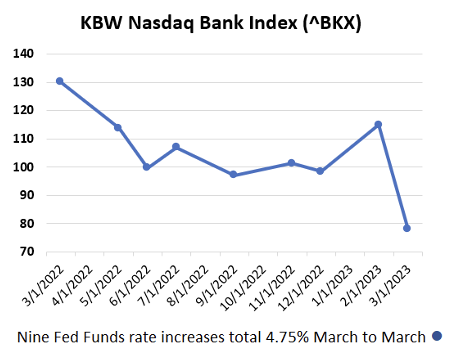

It turns out that most banks flew too close to the Sun. The KBW Nasdaq Bank Index – which tracks 24 U.S. national money center banks, regionals and thrifts – dropped 40% during the March-to-March boost. And the S&P 500 Sub/Regional Banks Index dropped 50.3% from 2/28/22 through 3/31/23 versus -4.30% for the S&P 500 over the same period.

One wonders if the Fed’s third mandate is to defeat all banks but the central bank.

By the way, inflation is nowhere near 2%. So no, Fed policy has not worked.

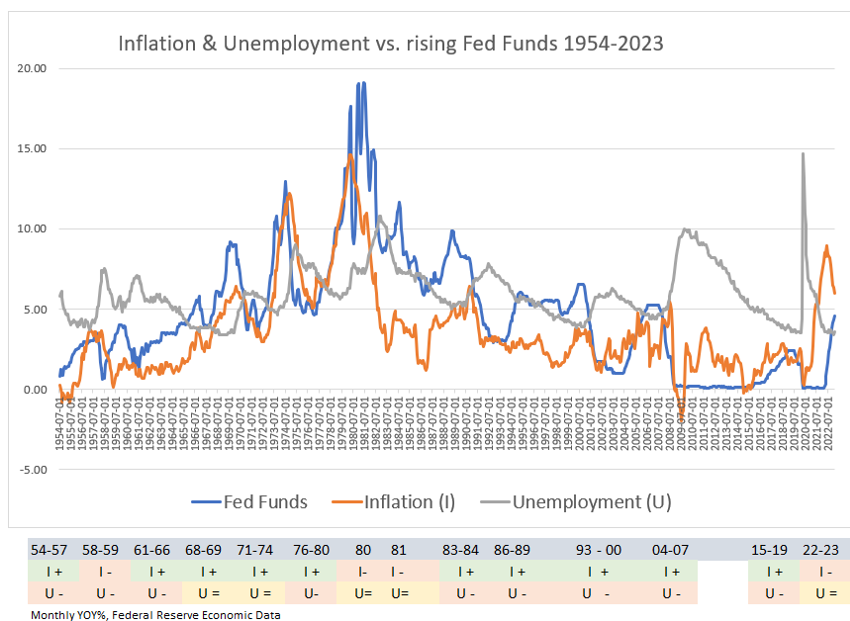

However, do not think that the Fed’s most recent failure is an outlier. How has history treated the Fed?

The Fed changes direction too quickly

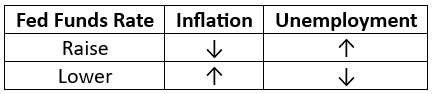

This is how the Fed funds rates impacted inflation (I) and unemployment (U):

Raising rates have failed to push down inflation, but it is a win (or coincident indicator) for pushing down unemployment. (However, pause a second and ask yourself how raising rates could lower unemployment.)

Notice how quickly the Fed changes direction – 27 reversals in the last 68 years. That’s 14 periods when the Fed funds rate was pushed up 2% without a reversal, and 13 periods when the Fed funds rate was pushed down 2%. My guess is this is more frequent than most people think. The Fed is busy either raising or lowering rates, or in rare periods just watching idly.

That means the Fed changes its mind every two and a half years on average. Tell me one other core economic policy that needs reversing every two years? Taxes? Regulations? How would that work? Long-term planning is difficult in such an environment. A commercial real estate investor told me, “It’s impossible to plan now. My bank tells me that they can only fix a lending rate one week before closing. I used to have much more time than that. It is impossible to run accurate pro forma projections.”

Has this worked? When the Fed flooded the economy with money, such as at the beginning of COVID, inflation soared, and employment plummeted. When the Fed tried to fix inflation by raising interest rates, it chased rates up. Interest rates are the cost of money, so why should this surprise us?

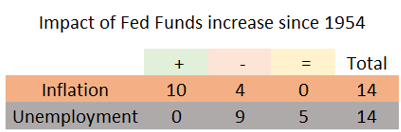

Among the 14 periods since 1954 that the Fed has raised rates, inflation has gone up in 10. Up, not down. Up. You may counter with, “Yeah, but eventually inflation dropped!” Sure, but interest rates were coming down by then. This is not managing; this is miming. The Fed is lip-syncing, or worse, it is shouting down the economy. The hubris of seven Board governors would be laughable if it weren’t so disastrous. The U.S. is a $27 trillion economy. Does it really think it can micromanage this?

Additionally, why did the Fed wait a year too late to start raising rates? If its objective is 2% and CPI was 4.1% in April 2021, why not act? The FOMC holds eight scheduled meetings per year. Even 12-month headline personal consumption expenditures index (the Fed’s preferred inflation measure) was, “3.6 percent…while PCE excluding food and energy was 3.1 percent.” Both were well above the 2% mandate. Unemployment was 6.1%, also above the historical average, yet crickets.

There is something about its dual mandate that is impossible to meet with the tool of raising or lowering interest rates. This chart is the expected effect that raising and lowering the Federal funds rate would have on inflation and unemployment:

The Fed can’t raise and lower interest rates at the same time, so the economy is stuck with one prescription for two diseases.

The Fed can’t raise and lower interest rates at the same time, so the economy is stuck with one prescription for two diseases.

Raising rates should dampen the economy and push down inflation. However, since 70% of small companies and nearly 100% of publicly traded companies borrow money, their borrowing costs go up. Results? Businesses suffer and now have to lay off employees. When would you want this?

Conversely, lowering rates should stimulate the economy and lower the unemployment rate, as businesses hire to meet increased demand. But what does that do to inflation? With more business activity, sales, demand, and prosperity, prices will naturally rise. Results: increased employment, but at the cost of higher prices. When would you want this?

Federal Reserve monetary policy does not work, has not worked, and cannot work.

The Fed is good for one thing

Provide liquidity in a catastrophic market.

That’s it.

The Fed is the banker’s bank. Who can argue with the occasional central-bank-funded lifeline when the U.S. is attacked (2001), banks collapse (2008), or a pandemic locks down the economy (2020), other than the most reality-challenged libertarian? Unfortunately, the Fed behaves as if we are always in a state of catastrophe.

Worse, the Fed blithely trades economic buoyancy for recession to meet its mandate. It’s interesting that among its mandates, avoiding recession, perhaps the only economic activity a political entity should embrace, is not even pondered.

Powell said recently, “No one knows whether this process will lead to a recession or, if so, how significant that recession would be.”

Then why force it? Earnings growth has already peaked according to Bloomberg, profits are expected to fall over 6% – the lowest bottom-up EPS in 20 years – inflation peaked June 2022 at 9.1% and has fallen steadily, the share of small businesses with positions unable to fill is at record highs (this number alone heralded seven of the last seven recessions), consumer spending is flattening, credit card loan delinquencies are rising, and home sales basically stopped.

Yet, come May 3rd? Another planned Fed funds increase.

History tells us not to be optimistic that the Fed will achieve its mandate: The central bank aims for 2% inflation. Yet, CPI and PCE averaged 3.8% and 3.3% respectively from 1960-2022 (WSJ, 2/24/23, and Federal Reserve Bank of St. Louis).

The tyranny of perfection is that it can never be achieved. If the Fed had a less ambitious goal, if the Fed realized that just changing polarity is enough, if the Fed wasn’t trying too hard to fluff their reputation, if…

Do no harm should be the Fed’s mission statement. It has caused damage on both sides – the massive build and now the collapse, first by throwing too much wood on the flame, and now by choking the fire by blocking the air.

“We hurt the economy to help the economy” has been the realized Fed mandate.

The trend is clear. Inflation is dropping, layoffs are growing, the stock market is more than 10% off its high set a year and a half ago, and U.S. bank lending contracted by the most on record in the last two weeks of March.

Dear Fed: It’s time to watch the room.

Andy Martin is author of Dollarlogic: A Six-Day Plan to Achieving Higher Returns by Conquering Risk, foreword by Arthur B Laffer, Ph.D.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All