The Time is Now for a Systemic Market Hedge

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The dynamics between the VIX and the S&P 500 last year marks a gateway to an impending crisis.i Declining markets with a nervous, range-bound VIX between 20 and 35, as we experienced in 2022 and into this year, have occurred repeatedly in the past. In each case, they preceded second-leg crises with VIX spiking to well above 35 – when most of the value destruction occurred. A range-bound VIX between 20-35 has common markers and dynamics which signal a “crisis gateway” that deserves a defensive posture.

Last year, 2022, was a challenging period for passive allocations to U.S. equities generally and to the S&P 500 in particular, which ground down 24.5% through October 12th from the market peak on January 3rd before regaining its tenuous footing into the first quarter of 2023. As of March 31, 2023, the S&P 500 was down 12.5% from its prior peak, having retraced about 50% of its losses. During this period, the VIX remained rangebound between 20-35, which indicated a transitioning market. Not all transition VIX markets are followed by crises, but there is a high probability that the current declining transition market off its high will become a crisis.

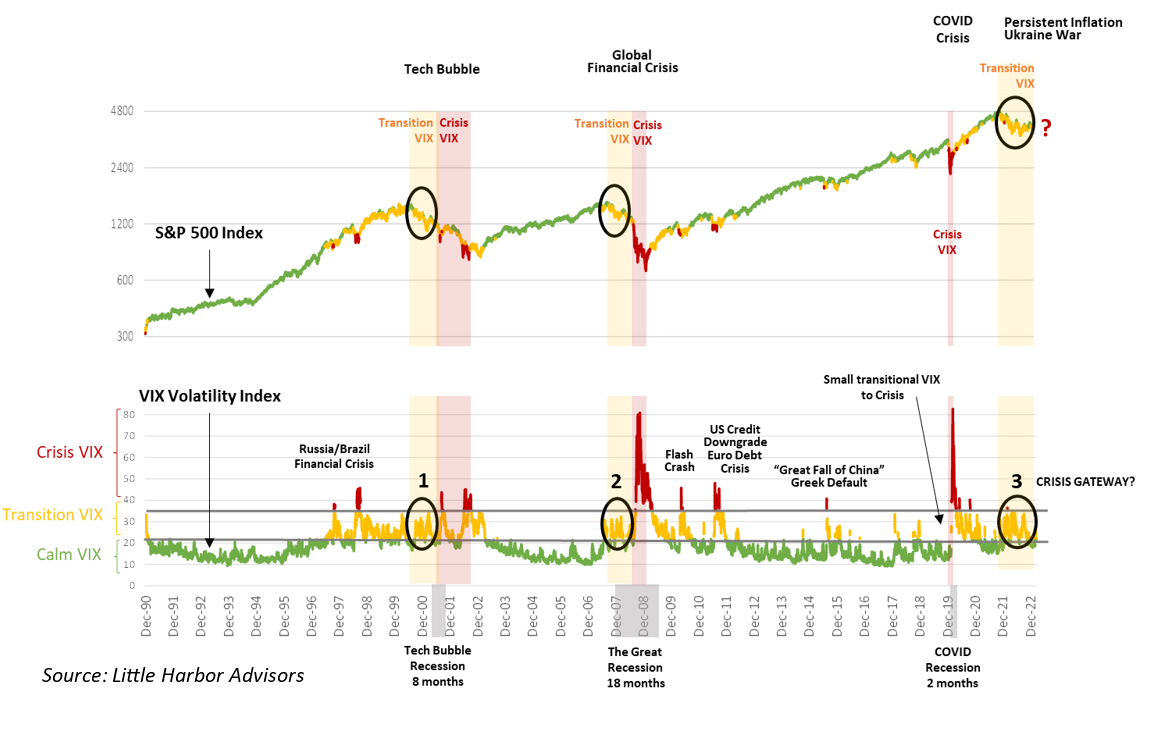

S&P 500 and VIX in perspective

To place 2022-2023 in perspective, the chart below illustrates the S&P 500 and the VIX indices going back to December of 1990. The S&P 500 index is presented in logarithmic scale to visually compare the 2022 decline in the context of the other secular crises and episodic shocks affecting the equity markets since 1990. For ease of reference, the

corresponding VIX index chart is divided into three color levels – green, yellow, and red corresponding to “calm VIX,” “transition VIX,” and “crisis VIX:”

In 2022, despite losses in the S&P 500, the absolute level of the VIX remained squarely in the yellow transition VIX zone, which was similar to the run-ups to the global financial crisis (GFC) in 2008 and the tech bubble in 2001. The COVID crisis, by contrast, experienced a very a sharp increase in the VIX as a result of an episodic shock similar to the Russian financial crisis of 1998, flash crash of 2009, the European debt crisis of 2012, and the China crisis of 2015.

The primary difference between secular crises and episodic shocks is the length of the transitional VIX period. When the S&P 500 is declining in a transition VIX period, it is generally a “gateway” to a crisis VIX period.

The dynamics of episodic shocks

Episodic shocks typically proceed from a calm market VIX to crisis VIX in relatively short periods of time. As the name suggests, an episodic shock occurs when a perceived threat to the U.S. stock market has the potential to create a crisis. A VIX level above 35 corresponds to a meaningful two-standard-deviation divergence from the VIX mean of 20 – which typically occurs when there is consensus in the market that a systemic risk exists that needs to be broadly hedged with S&P puts.ii Episodic shocks are generally not tied to the fundamental secular dynamics of the U.S. economy and account for smaller market drawdowns.

The dynamics of secular crises

One of the key characteristics of rarer secular crises is that they coincide with cycles of economic recessions. One of the major reasons that the S&P 500 declines in extended transition VIX periods is that investors are not using puts on the S&P 500 as a systemic hedge. Rather, they are rotating leadership in their stock allocations and contributing to the controlled decline in what they view as a correction opportunity. Investors use periods of lower cross-correlations to pick leadership diversification within equity indices like the S&P 500 and, generally, continue to do so while stock fundamentals exist and there is little perceived systemic risk in the market.

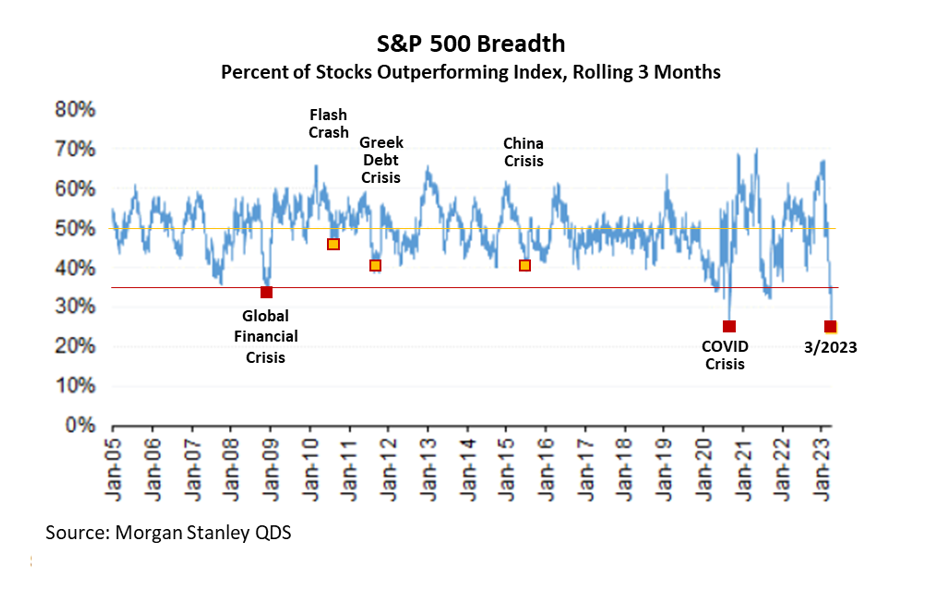

But picking leadership diversification becomes harder in a late-cycle lead-up to secular crises. This has typically been associated with large increases in price cross-correlations in the equity markets due primarily to the deterioration and collapse of market breadth – strong indications of breadth deterioration occur when the majority of stocks in the S&P 500 have negative forward earnings and are trading below their 200-day moving average, or the percentage of stocks outperforming the index fall to new lows.

In the tech bubble and GFC secular crises, the observed “gateway” between transitional and crisis VIX levels was when the systemic risk of a U.S. recession was fully priced into the market and there was little benefit from sector or stock selection as correlations converged. In this environment, the lack of diversification leaves no option but to hedge the S&P 500 index. In those instances, the VIX above 35 signaled the capitulation of the S&P 500 and the final stages of value destruction in the market.

Crisis gateways generally occur halfway down

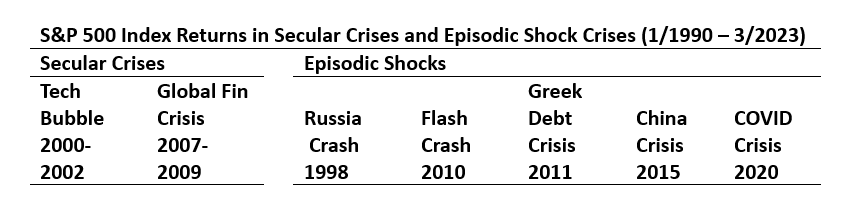

The following table illustrates the disaggregation of drawdowns since 1990 into their transition VIX and subsequent crisis VIX components:

As one would expect, secular crises have had larger total drawdowns and long periods of transition VIX before capitulating to crisis VIX levels when recessions get priced into the market. Episodic shocks had lower total drawdowns and shorter transition and crisis VIX periods. In both cases, however, the transition VIX and crisis VIX each contributed roughly equally to the total crisis drawdowns (with the notable exceptions of the GFC and the COVID crises when 60% and 70%, respectively, of the value destruction occurred during crisis VIX periods). In both cases, the crossover from transition VIX to a crisis VIX was almost always accompanied by a pronounced inversion of the term-structure of the VIX into backwardation (an indication that there is more near-term than long-term fear).

COVID crisis – Perfect storm

The exception to my easier categorization into episodic shock or secular crisis was the market reaction to COVID, which was a simultaneous consensus response to the shock of a fearsome pandemic and to its recessionary fallout – which both warranted massive hedging of the S&P 500 index to offset quickly evident systemic risk in the market. The structure of the COVID crisis was unique in its speed and scale. The transition VIX period was very brief with a -8% S&P 500 decline, followed by a large -26% decline associated with crisis VIX levels. Further declines were likely stemmed by the reassertion of massive monetary intervention, zero-interest-rate policy, and extraordinary fiscal stimulus programs.

2022-2023 – Gateway to crisis VIX?

Hedged-equity strategies that use the VIX as a hedging mechanism for passive long portfolios can face a challenging hedging environment when declining equity markets are in extended transition VIX stages – grinding down slowly without the VIX moving above 35, which generally announces crisis VIX and offers the most potent hedge.

As I noted earlier, crisis VIX levels typically occur during secular crises when systemic risk of recession gets priced into the overall market – usually after the collapse of market breadth leaves traders few diversification options and significantly increases the rationale for systemic put hedging.

As illustrated in the chart below, one of the measures of market breadth – the percentage of stocks outperforming the S&P 500 index – is at two decades lows:

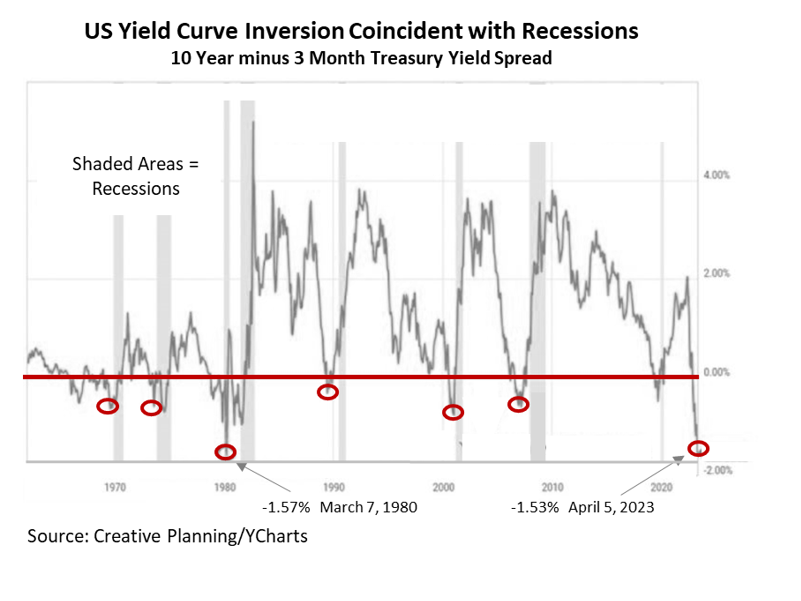

In addition to extreme concentration of stocks, the inversion of the Treasury yield curve has in the past supported the probability of recessionary outcomes for the economy as a whole:

This 2023 yield-curve inversion may not be any different from those in the past, particularly the stagflation decade of 1970s, when inflationary expectations were so high that the Fed’s rising interest rates lowered output and employment rather than capping prices – and led to three yield curve inversions and three recessions before inflation was ultimately tamed. The Fed’s current determination to stifle inflationary expectations is one of the leading reasons that it will continue to be hawkish well into a hard-landing recession, if necessary.

A systemic market hedge is more prudent than ever. The transition VIX of the last year may, as it has in the past, mark a topping process in the S&P 500 and a gateway to an impending crisis – as the reality of a looming recession undermines the narrow group of large-market-capitalization stocks upholding the market, and as market participants realize that the Fed is effectively short the S&P 500 until inflation is under firm control.

Moses Grader is the chief risk officer of Little Harbor Advisors, LLC, and a founding member of its research team, which focuses on developing and incubating Market State™ factors driving the firm’s approach to tactical investing and risk management.

i S&P 500 Index is the S&P 500 (TR) Index and VIX is Chicago Board Options Exchange (CBOE) Volatility Index.”

ii The VIX measures expectations for stock market volatility over the next 30 days by using options data in combination with other factors such as volume data and open interest index data in order to compute a value. Increase in S&P puts relative to S&P calls increases VIX.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All