Hedge Funds at War for Top Traders Dangle $120 Million Payouts

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWhen portfolio manager David Lipner said he was quitting billionaire Izzy Englander’s Millennium Management to join a rival, the hedge fund countered with an unusual proposal: A one-year paid sabbatical and an incentive upon return if Lipner stayed.

And stay he did. For Millennium, the $58 billion industry giant known for ruthlessly cutting underperformers, the generous offer was seen as totally worth it. After all, Lipner had made money for the firm for more than a decade, longer than most hedge funds remain in business.

Such enticements are now becoming part of a growing array of expensive tools the world’s biggest hedge funds are deploying to hire and retain traders. They show how a limited pool of talent and surging demand for steady returns in a volatile market are prompting firms to pull out all the stops to attract the best — with clients footing the bill.

The hunt is no different from the bidding war for Premier League or NBA players, one executive said. Last year, a senior portfolio manager was lured by a major New York fund with more than $120 million in guaranteed payouts, according to a headhunter who said he’d done several deals paying north of $50 million. Contracts worth $10 million to $15 million are increasingly becoming common for traders, said another.

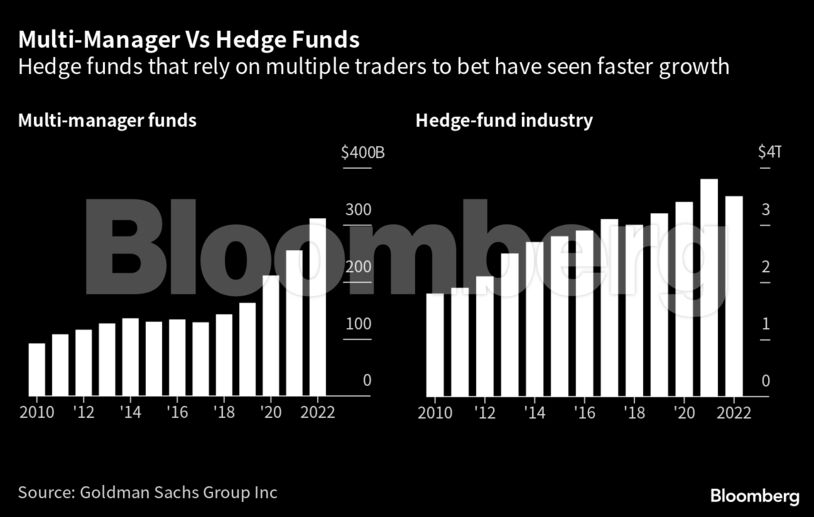

Hedge funds have long been the land of eye-popping rewards, but a few recent trends are converging to take it to new levels. The stellar track record of several giant firms that spread money across teams of traders following multiple strategies has caused their assets to surge. That’s prompted a hiring spree to add more traders and strategies so the existing ones aren’t overstretched.

The performance — and resulting wait lists of investors wanting it — has also given the firms leverage over clients to charge many times the traditional 2% management fee and use that for recruitment and retention. And as the firms increase rewards and defer more of them over several years, it’s taking even bigger offers to tempt traders into leaving.

“In a world where there’s a lot of liquidity, the bigger challenge in developing a platform business is investing in talent rather than attracting capital,” said Chris Milner, the chief operating officer of London-based Eisler Capital, which is transforming itself into a multi-strategy hedge fund from its roots in macro trading.

Lipner wasn’t the only one offered the sabbatical by Millennium, people familiar with the matter said. The New York-based firm recently dangled similar deals at several others, they said, asking not to be identified discussing internal matters. One of them quit anyway, showing such baits don’t always do the trick. Lipner didn’t respond to requests for comment. A representative for Millennium declined to comment.

Millions of dollars in signing bonuses and a higher cut of trading profits during initial periods — aimed at replacing any pay lost from leaving a past employer and having to sit out non-compete periods — are now becoming the norm at multi-manager investment firms ranging from Millennium, Citadel, Point72 Asset Management to BlueCrest Capital Management and Balyasny Asset Management. While the rest of the hedge fund industry grapples with outflows, the biggest is beefing up.

Clients mostly do not get to see details of the payouts and guaranteed bonuses though they foot the bill through an opaque blank check for a “pass-through” fee. That payment allows hedge funds to charge clients for anything from compensation and research to entertainment.

Clients also can be on the hook for expenses such as fitness plans for traders at Point72, relocation expenses at Balyasny, investment and litigation-related costs at Verition Fund Management and Millennium's key-man life insurance on Englander for the fund, according to their client offering documents reviewed by Bloomberg News.

A Point72 spokeswoman said though the fitness plan costs are included in the offering document, they are not currently passed on to customers. She declined to comment further.

“It’s not a scandal and I am intellectually not against higher fees, but multi-PM hedge funds are setting the bar too high,” said Mario Unali, a senior money manager at Kairos Partners which invests in hedge funds. “There doesn’t seem to be a limit to the hedge fund compensation scheme.”

The traditional 2-and-20 fee model hedge funds once employed meant that for a 20% gross return, the firm took about one-third of the gains and the clients got the rest. A rough calculation by Sebastien Sirois, chief investment officer at Blue Lotus Management also gives money to hedge funds, showing fees have gone so high at multi-manager platforms that investors on average get back only about 45% of the trading profits, and the firms take the majority.

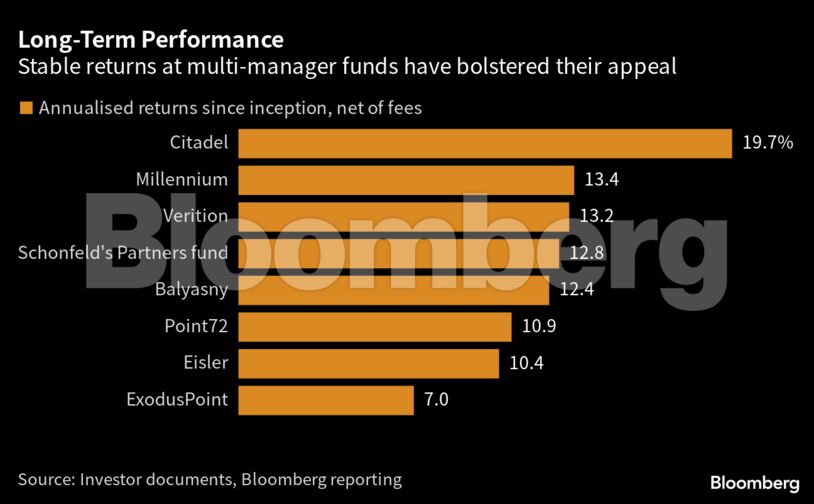

So far, even after the higher fees are accounted for, the net performance at the biggest firms is still attracting investors.

The most obvious place for those firms to recruit new talent is from each other. A flurry of such moves has also brought conflicts, litigation, and punitive measures to try to avoid changes of heart.

So some multi-strats have found success convincing promising traders to close up their own shops, even when they’re doing well. Eisler lured Sean Gambino, who ran his own Heron Bay Capital, into shuttering it. Schonfeld Strategic Advisors persuaded famed trader Ben Melkman to abandon his plans for a hedge fund startup and instead run a strategy for its own macro business. More than a quarter of Balyasny’s investment team recruits came from single-manager firms last year, according to a person with knowledge of the matter. A representative for Balyasny declined to comment.

And when hedge funds aren’t poaching talent from rivals, they are devising ways to lock in their own traders.

One tool is the multi-year non-compete agreement, a practice that’s come increasingly under scrutiny globally, with the US Federal Trade Commission proposing a ban in January and the UK planning to limit the restriction to three months.

Yet the use of the clause is widespread, and even some firms that once eschewed it are changing their tune.

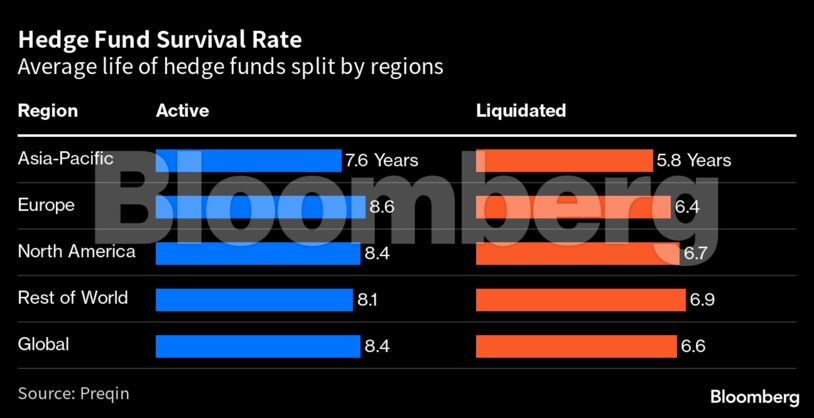

When ExodusPoint Capital Management debuted five years ago as the biggest-ever hedge fund startup, it typically had traders sign a standard employment contract with a three-month exit notice. They could even walk away with their trade secrets.

But of late, the $12.7 billion ExodusPoint has been resorting to non-compete contracts that stretch a year or longer. That comes as it adds top managers including Pete McConnon, previously the co-head of macro trading in London for Balyasny, and Patrik Olsson, the former chief investment officer of Nektar Asset Management.

Long Haul

Hedge funds are also looking beyond financial incentives to retain talent. Pitches include a collaborative culture, help for portfolio managers to build their teams, and greater tolerance for explainable trading losses. Firms expanding globally also offer flexibility to work from any location.

“A lot of PMs want more than a capital provider, they want a partner who can help them build a business for the long haul,” said Jennifer Blake, the global head of business development at Balyasny. “Competitive compensation is table stakes; the question is how can you differentiate the seat by leveraging tech resources, data, and market insights across strategies.”

But the standard retention method is still to make it tough to leave.

Balyasny imposes longer sit-out and non-solicitation restrictions if a trader leaves for direct competitors such as Millennium, Citadel, or Point72, people with knowledge of the matter said, asking not to be identified discussing internal matters.

At Michael Platt’s BlueCrest, payouts are deferred by two years, and quitters who break their contracts lose those awards. The firm pays as much as 30% of the trading profits, one of the highest rates in the industry, a headhunter said, describing it as a golden chain.

Billionaire Ken Griffin’s Citadel also has a multi-year deferral program, which allows staff to invest in Citadel funds. With its flagship hedge fund gaining 38% last year, that’s another carrot to keep existing employees and lure recruits.

Representatives for BlueCrest, ExodusPoint, and Verition all declined to comment.

External Managers

When all efforts to hire the best of the best fail, large hedge funds end up tapping top traders at smaller firms to manage hundreds of millions of dollars externally.

Millennium, where more than 290 teams of traders invest across asset classes, remains one of the most prolific employers in the industry. Still, it gave several billion dollars to Delta Global Management and Lorenzo Rossi’s Kedalion Capital Management to manage. Such external arrangements make up less than a tenth of Millennium’s teams of traders, and many of the outside groups manage money exclusively for the firm, according to a person with knowledge of the matter.

Point72, BlueCrest, Balyasny, and Schonfeld are among those that have given money to external teams through so-called managed accounts that still give them control. Just over half of all the multi-manager hedge funds now allocate to outside traders, according to Goldman Sachs Group Inc.

“Even the biggest hedge funds have become meaningfully more flexible to win the bidding war for talent because there’s so much more capital in the space and so many more firms trying to emulate successful players,” said Marlin Naidoo, global head of capital introduction and consulting at BNP Paribas.

‘Apex Predator

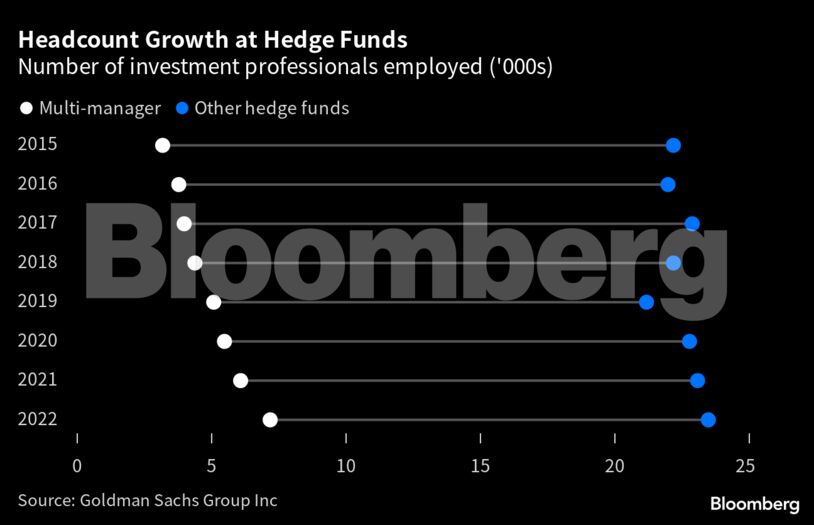

But poaching traders is still the most common approach, with one top industry executive describing multi-manager firms as the “apex predator.” Those firms manage just 8% of the industry assets, they employ 24% of total staff, according to estimates by Goldman Sachs.

“The market is absolutely competitive, but we’re in it to compete for the best talent,” said Danielle Pizzo, Schonfeld’s chief strategy officer. “We’re flexible, we customize our offering in ways that others don’t,” she said, adding that the approach has ensured that only three portfolio managers left voluntarily over the last decade.

There’s even been hiring to enable more hiring.

When Schonfeld launched its discretionary macro and fixed-income business in 2021, the firm brought on individuals within the unit reporting to co-heads Colin Lancaster and Mitesh Parikh to exclusively focus on acquiring talent. Peter Hornick, previously at ExodusPoint, leads such a team at Brevan Howard Asset Management. Eisler recently hired former Goldman partner Alain Marcus to concentrate just on recruiting.

Still, for investors who pay for it all, the only reliable way to earn stellar returns is to keep giving money to platforms that can prevail in the race.

“Multi-PM platforms are first and foremost an HR business,” Blue Lotus’s Sirois said. “We worry about some of our multi-PMs who are not keeping up with the bidding war or provide the sub-par environment for the traders.”

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All