As is the case with stock and bond funds, not all reinsurance funds are created equal. They can have different expense ratios, levels of diversification and levels of risk – writing policies with higher deductibles (more “out of the money”) and thus smaller premiums, or lower deductibles (less “out of the money”) and thus higher premiums. I will analyze the pros and cons of three funds to access the reinsurance market. Before doing so, I begin with a brief discussion on why investors should consider including reinsurance as part of their diversification strategy.

For investors seeking to diversify the risks of traditional stock and bond portfolios, a logical candidate is reinsurance. Reinsurance investments have a risk premium that has been both persistent (the reinsurance industry has more than 150 years of profitable investing) and pervasive around the globe, survives transactions costs, and has a logical risk-based explanation for why the premium should be expected to persist in the future. And importantly, the risks of reinsurance have been uncorrelated to the economic cycle risks of stocks and inflation, and the credit risks of bonds. Stock market crashes don’t cause earthquakes, hurricanes or other natural disasters. The reverse is also generally true – natural disasters do not cause bear markets in either stocks or bonds. The combination of the lack of correlation and potential for equity-like returns results in a more efficient portfolio, specifically one with a higher Sharpe ratio (a higher return for each unit of risk).

Of course, the expected (not guaranteed) reinsurance risk premium is compensation for accepting the risk that reinsurance will experience extended periods of poor performance – as was the case from 2017 to 2019 for reinsurance funds that invested in quota shares (pro-rata co-investments of the books of business of reinsurers), though not for catastrophe- (“cat-”) bond funds. However, this is no different for any risk assets. For example, the S&P 500 has experienced three periods of at least 13 years when it underperformed riskless one-month Treasury bills. And value stocks experienced their largest drawdown in history from 2016-2020. As another example, gold (which is supposed to be a hedge against inflation) lost almost 90% of its real value over the period January 1980-March 2002. Growth stocks, large stocks, small stocks, international stocks, emerging markets, safe Treasury bonds and real estate have all experienced long periods of underperformance. That’s why investors demand a risk premium! In other words, long periods of underperformance are not a reason to avoid an asset class but a reason investors should construct highly diversified portfolios – reducing the risk that all or most of their “eggs” are in the wrong basket at the wrong time. Most investors are unaware that a traditional 60% stock/40% bond portfolio has about 90% of its risk in market equities, not 60%. The reason is that stocks are much riskier than bonds. That is why institutional investors create much more diversified portfolios. For example, endowments with more than $1 billion had 48% of their holdings in alternatives.

Stocks have experienced their highest returns after the periods of greatest losses (because valuations fell dramatically, allowing investors to buy at low prices). So too have reinsurance returns (because premiums rose, underwriting standards tightened and deductibles rose, reducing risk). Thus, as is the case with stocks, the key to successful investing in reinsurance is to be a patient, long-term investor, buying after periods of poor performance (instead of engaging in panic selling).

Choosing the right vehicle

There are three funds for investors to consider to gain exposure to the reinsurance risk premium – Stone Ridge’s High Yield Reinsurance Risk Premium Fund (SHRIX), Stone Ridge’s Reinsurance Risk Interval Fund (SRRIX) and Pioneer’s ILS Interval Fund (XILSX). Demonstrating that reinsurance is a unique risk asset, the correlation of the S&P 500 to the three funds has been only about 8%. Let’s compare the three funds.

SHRIX

The vast majority of the fund’s assets (typically 85%-90%) are invested in public cat bonds, with a minority invested in illiquid quota shares (pro-rata co-investments of the books of business of reinsurers Stone Ridge partners with). That mix allows the fund to provide daily liquidity. The fund’s expense ratio is 1.74%. Daily liquidity can be an important issue for investors who need/desire liquidity. However, investors in publicly available liquid securities sacrifice a significant illiquidity premium available to investors in XILSX and SRRIX, both of which are interval funds that invest the majority of their assets in quota shares – illiquid one-year contracts. The size of the illiquidity premium is regime dependent (tending to rise in periods of elevated financial risk and fall in calm periods) and can be significant (typically between about 1.5%-3%).

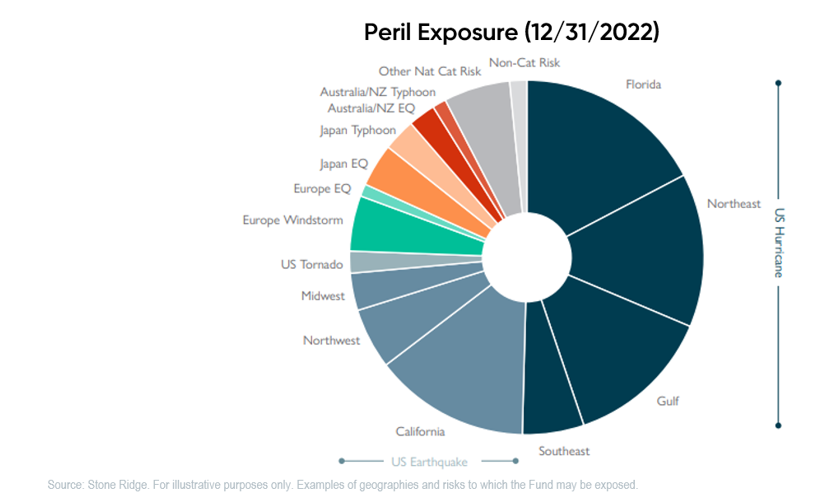

In addition to sacrificing the illiquidity premium available in quota shares, a disadvantage of SHRIX relative to SRRIX and XILSX is that it is less diversified by peril and geographic exposure, with about half the fund’s risk exposure allocated to U.S. hurricanes and about one-quarter to U.S earthquakes.

Another feature of the fund, which some investors will consider to be a positive, is that cat bonds tend to insure against risks that are more out of the money (have larger deductibles). That reduces the likelihood of the fund incurring a loss from an event, which may reduce the risk of some investors abandoning the strategy when short-term performance is poor. Of course, the offset is that the premium the fund receives for taking the risk is proportionately lower, and thus expected returns are lower.

SRRIX

The vast majority of the fund’s assets are invested in illiquid quota shares, allowing the fund to earn the illiquidity premium – a significant advantage for those investors who don’t need full liquidity. The interval fund structure provides for a minimum of 5% liquidity per quarter and 20% per annum. An individual investor may be able to redeem 100% of their investment at a quarterly redemption if no more than 5% of all shares held were submitted for redemption. On the other hand, if a fund had to limit redemption requests over an extended period, it is possible an investor might have to wait five years to fully redeem all their shares (SRRIX investors experienced such a period from November 2018 until February 2023). Reinsurance should be thought of as a long-term investment, as is the case with all risk assets. Investors in tax-advantaged accounts such as IRAs (both Roth and traditional) who are not taking more than their RMD (required minimum distribution) do not typically need more than the minimum 20% liquidity that is provided by the interval fund structure. For those investors, the illiquidity premium is as close to a free lunch as there is in investing.

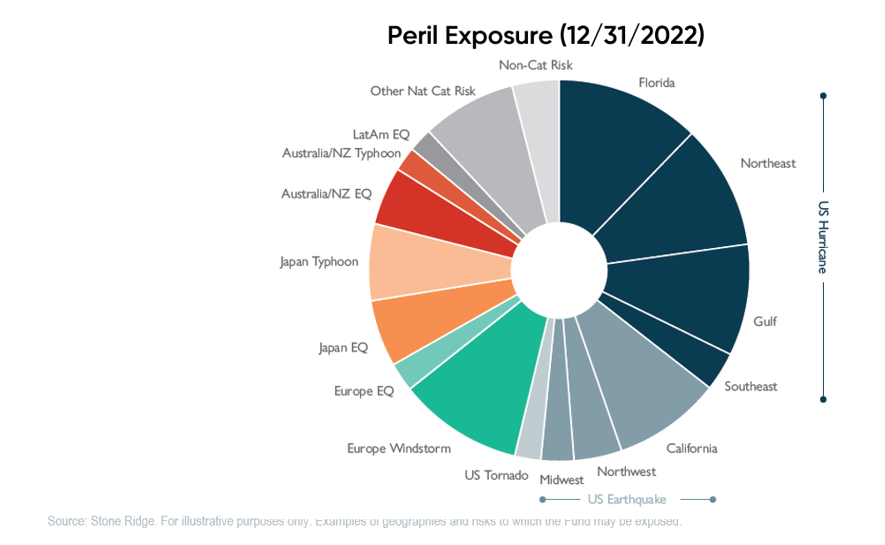

Another advantage of the fund versus SHRIX is that SRRIX is more diversified by both perils and geography, adding European, Japanese and Australia/New Zealand exposures. All else equal, investors should prefer a more diversified fund.

The fund also tends to focus on risks with lower deductibles than those SHRIX is exposed to. Accordingly, it is more exposed to risk for which the fund is compensated, with higher premiums and higher expected returns.

The fund’s expense ratio is 2.42%, higher than that of SHRIX. The higher expense is related to the higher costs of running a fund that uses quota shares versus buying publicly available securities. Stone Ridge is basically running a reinsurance company (having to negotiate quota share agreements with a significant number of reinsurers to diversify risks) without its significant expenses. For example, Munich Re has about 40,000 employees, including hundreds of underwriters and dozens of meteorologists and engineers evaluating risks, while Stone Ridge has about a dozen focused on reinsurance. The net effect is that SRRIX has the same access to business, pricing power, underwriting expertise and risk modeling insights as the largest reinsurers in the world. It also has a similar expected return on investment to a reinsurance company. However, the illiquidity premium and higher premiums provide investors with higher expected returns than SHRIX, more than offsetting the fees on a risk-adjusted basis. For example, risk modeling by Stone Ridge shows that as of the end of February 2023, the 50th percentile return to SRRIX for the full year was 23.1% versus 16.5% for SHRIX and 15.2% for the cat bond index.

Those investors who are concerned about the potential for greater losses (due to smaller deductibles) can allocate a smaller percentage to SRRIX than they would to SHRIX (say, 3% or 6% versus 5% or 10%).

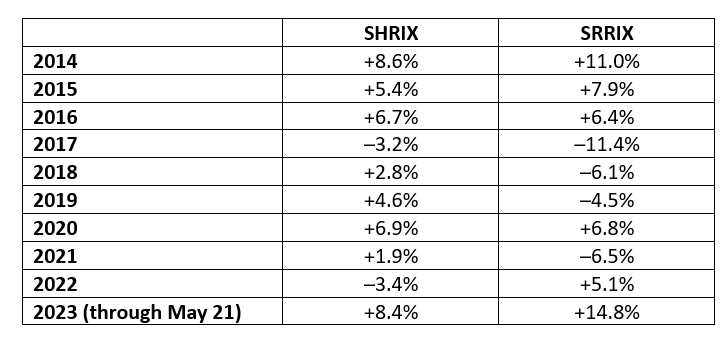

The following table shows the historical annual returns of SHRIX and SRRIX to demonstrate how the risk and expected return dynamics have played out. While SRRIX has a higher expected return than SHRIX, that higher return expectation is compensation for both illiquidity and higher risk (greater volatility of returns). Out of the nine years in the sample, SHRIX experienced negative returns in just two. SRRIX experienced negative returns in four years, three of which were consecutive. The worst calendar-year return for SHRIX was down 3.4%, while SRRIX had four calendar years with losses greater than 3.4%. The worst calendar year return for SRRIX was down 11.4%.

XILSX

The fund, an interval fund, provides broad exposure to reinsurance risks in terms of types of risks and geographic exposures. XILSX can be purchased and sold only once per quarter, while both SRRIX and SHRIX can be purchased daily. It also invests in quota shares, cat bonds and other reinsurance-linked securities (such as warrants and other derivatives). The fund’s expense ratio is 1.91%, between that of SHRIX and SRRIX. The fund also tends to focus on exposures that have greater deductibles (more out of the money), reducing the risk of loss, with a correspondingly smaller risk premium and lower expected returns. XILSX is expected to have a higher risk of loss and higher expected return than SHRIX. As an interval fund, like SRRIX, it provides limited liquidity.

The fund is typically a good fit for those investors who are willing to accept the illiquidity risk (to earn the illiquidity premium) but prefer to have a smaller risk of loss (in exchange for a lower expected return than SRRIX).

Takeaways

Given the expected risk and return characteristics of reinsurance, it is possible (if not likely) that interval funds in this space will experience future extended periods of gating in years following large losses. Thus, investors concerned about this risk of illiquidity should prefer SHRIX. On the other hand, only investors who have a need/desire for liquidity should prefer SHRIX to SRRIX or XILSX, as they sacrifice both the illiquidity premium and have a portfolio that is less diversified in risk exposures. Investors who are more risk averse to large losses can still earn the illiquidity premium investing in SRRIX but with a lower allocation to the fund than investors with greater risk tolerance. Investors seeking the highest return, accepting the risk of greater losses, should prefer SRRIX; and more risk-averse investors (accepting lower expected returns) should prefer XILSX. In addition, since the risks taken by SRRIX and XILSX are not identical, investors with more than a nominal allocation to the asset class could consider owning some of both.

Larry Swedroe is head of financial and economic research for Buckingham Wealth Partners.

Certain information is based on third-party data and may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed the adequacy of this article.

Alternatives strategies for clients should be carefully considered, as the strategies’ risks and objectives may not be appropriate for all clients. There are no guarantees alternatives strategies will achieve long- term higher risk- adjusted returns and may result in the loss of principal. Alternatives strategies involve a high level of risk, including liquidity risk, which should be discussed with the client to determine their willingness, need, and ability prior to implementation.

Investors should carefully consider the funds mentioned herein and their investment objective, as an investment in these funds may not be appropriate for all investors and the funds are not designed to be a complete investment program. There can be no assurance that these funds will achieve their investment objective, or the estimates/projections provided. An investment in these funds involves a high degree of risk and should be discussed prior to implementation. For additional risks, please refer to the prospectus and statement of additional information for these funds.

© 2023 Buckingham Wealth Partners. Buckingham Strategic Wealth, LLC & Buckingham Strategic Partners, LLC (Collectively, Buckingham Wealth Partners). LSR-23-501

Read more articles by Larry Swedroe