Spare a thought for the other AT1 crowd — not investors in Additional Tier 1 securities extinguished in Credit Suisse Group AG’s rescue, but shareholders in Aroundtown SA, the Frankfurt-listed property firm with the same stock-market ticker. The capital markets of yesteryear allowed the company to amass a sprawling real-estate empire valued on its books at €28 billion ($30 billion). The markets of today are forcing an unravelling.

Founded in 2004 and listed in 2015, the firm hoovered up offices, hotels and residential accommodation, mainly in Germany. Today, Aroundtown is a favorite for short sellers. Its market capitalization has shriveled to just €1.7 billion, representing a near-90% discount to net asset value — one of the lowest valuations in the European sector.

Aroundtown must now contend with a radically different interest-rate environment. At first glance, its leverage looks manageable. Its portfolio valuation would need to fall 40% before loan-to-asset value debt covenants were tested. That seemingly reduces the risk of a sudden crunch.

The flipside of rising yields is that Aroundtown’s €20 billion of total debt is trading below face value, and the company has been buying some of it back — a way of repaying less than originally borrowed. Last week it said it had retired €710 million of its bonds at an average 17% discount so far this year. The company also has decent liquidity. Cash, expected disposal proceeds and vendor loans of €4.1 billion comfortably cover maturities up to the end of 2025.

Why, then, such a terrible valuation? Clearly, the market doesn’t think the value of the firm’s property in its accounts reflects the current environment. Some analysts want clearer disclosure of the assets. But there are some other financial issues, too.

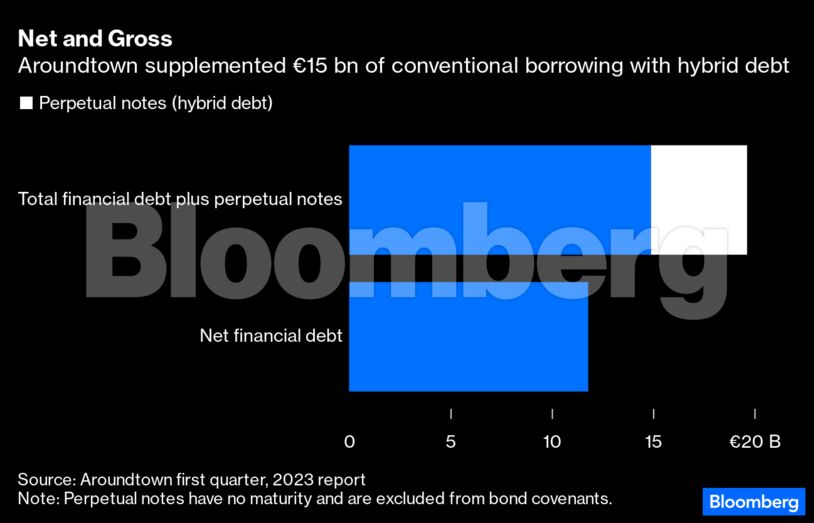

For a start, bond repayments from 2026 look daunting. Furthermore, the debt burden includes nearly €5 billion of so-called hybrid instruments issued by Aroundtown and its main subsidiary. Adding in that flavor of financing gives Aroundtown the highest loan-to-value measure in the sector, UBS Group AG analysts point out.

These instruments are equity-like in that they don’t ever need to be repaid. Yet they’re no free lunch for the issuer. Aroundtown faces penalties if it does not redeem – or “call” – the hybrids at designated dates. The direct punishment is in higher coupon payments. Failing to call provides a motive for credit-rating firms to take a dimmer view of the company.

When the most recent call date came in January, Aroundtown let the coupon on the hybrid reprice higher — to a painful 7.1%. Refinancing wasn’t an option: A new hybrid would have cost even more. But calling would have used up cash reserves better spent on bond maturities and supporting the investment-grade credit rating, currently BBB+ from S&P Global Ratings.

To put that in perspective, the company says its average cost of debt is around 2%. Aroundtown’s yet-to-be-called hybrids have coupons ranging from 1.5% to 3.4% and call dates spread over the next three years.

The coupon resets are tied to market rates — so may not always be so painful. But the looming higher reset costs threaten a big hit to earnings. Of course, inflation ought to be pushing up rental income to compensate, but this can’t help on the scale required (underlying annual rental growth was 3.5% in the first quarter). Analysts at real estate research specialist Green Street reckon earnings could halve by the end of 2026.

How can Aroundtown get out of the hybrid hole and prepare for future bond maturities? Raising cash through an equity issue would be impossible with the shares where they are.

The only realistic option appears to be to go even faster in making disposals. Its Center Parcs resorts in Germany, Belgium and the Netherlands are already up for sale, Bloomberg News reported last month. Then there’s a stake in listed residential landlord Grand City Properties SA. But trickier to offload will be parts of its German office estate.

If Aroundtown sells its best assets, it reduces the overall quality of its portfolio. If it sells lower-quality assets, it likely has to accept prices below their value in its accounts — forcing it to book a loss, and damaging its leverage ratios. Green Street reckons the best way forward for the share price is to “sell the family silver” and use the proceeds to extinguish the hybrids.

There is of course the cross-your-fingers option – essentially hoping that rates will come down and other more competitive sources of finance will emerge, notably from banks. But that is a gamble. Markets can get worse as well as better.

The position mirrors that of other property firms that hoovered up assets in the go-go times. It’s hard to unwind such empires, emotionally and practically. But this company has a good window of opportunity to accelerate asset sales before it becomes a forced seller. It should use it.

A message from Advisor Perspectives and VettaFi: To learn more about this or other topics, please check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.