Big money managers are slashing bearish wagers and boosting equity exposure ahead of a week of potentially market-moving news.

Large speculators, mostly hedge funds, trimmed net short positions in S&P 500 e-mini futures from a record high, according to data from the Commodity Futures Trading Commission. The reduction of almost 90,000 contracts over the week through Tuesday ranks among the five biggest episodes of short covering since 2018.

Meanwhile, hedge funds tracked by JPMorgan Chase & Co. saw a spike in net equity purchases that built on the largest four-week buying spree since August. As a result, their net leverage, a measure of risk appetite that takes into account long versus short positions, has jumped to a one-year high.

With inflation data and a Federal Reserve decision in the offing, the buying binge marks a meaningful shift among a cohort of previously steadfast bears whose cautious stance paid off during 2022’s market rout. Skeptics have come under pressure to rethink positioning after the S&P 500 surged more than 20% from its October low.

Money managers “have been forced to grab into exposure to play for a ‘crash-up,’” Charlie McElligott, cross-asset strategist at Nomura Securities International, wrote in a note.

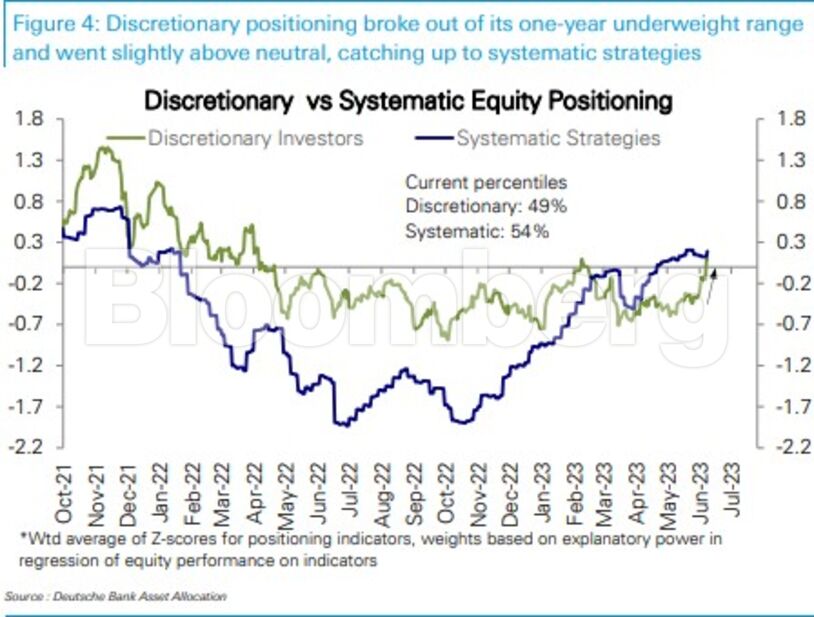

Among investors giving up on their cautious stance are those who use economic and earnings trends to guide their decisions. According to data compiled by Deutsche Bank AG, discretionary investors last week favored stocks after a stretch of aversion since February that had recently stood in contrast with their more optimistic-looking, computer-driven counterparts.

All told the firm’s measure of aggregate equity positioning turned overweight for the first time in more than 16 months, according to strategists including Parag Thatte.

The shift may not be good news to market observers who consider sentiment as a contrarian indicator. Just as the prevailing pessimism at the end of 2022 set the stage for an equity rebound, optimism now can make the market vulnerable to the downside.

With inflation forecast to soften for an 11th month, Tuesday’s release of May’s Consumer Price Index is likely to bode well for stocks, according to JPMorgan’s trading team including Andrew Tyler. Another potential tailwind comes from the Fed, which economists in a Bloomberg survey expected to pause interest-rate increases for the first time in 15 months.

The prospect of cooling inflation and a pause in aggressive monetary tightening have raised hopes that the economy could avoid a serious downturn. This month, investors have flocked to economically sensitive stocks, such as banks and small-caps, betting that a soft landing can breathe life into previously beaten-down sectors.

“The combination of positively surprising macro data and lower inflation should continue to support markets,” Tyler and his colleagues wrote in a note. “If the Fed does not hike in June or July, then it seems likely the market begins pricing in more optimistic outcomes.”

The JPMorgan team on Monday laid out a game plan for stocks on CPI day. In their view, the most likely scenario is that headline inflation comes in between 4% and 4.2%, and the S&P 500 climbs by 0.75% to 1.25%.

The CPI is forecast to fall to 4.1%, according to a Bloomberg survey of economists, from 4.9% previously.

Going by the latest money flows among JPMorgan’s hedge fund clients, skepticism toward the economy is showing signs of easing. The cohort’s equity purchases last week were driven by cyclical shares such as consumer discretionary and commodity producers, data from the firm’s prime brokerage unit show.

At the same time, hedge funds were unwinding their short positions “sharply,” according to the team led by John Schlegel. The process, known as degassing, may have further to go. Compared to prior instances, the team found that the current degrossing episode is likely only 25% done.

While benign economic data and the Fed meeting can propel further equity gains, forcing additional short covering that feeds into the rally, Schlegel and his colleagues warned that a bullish tilt eventually opens the door for a market reversal.

“There also seems to be increasing downside potential for markets due to the recent increases in risk and quite extreme divergences within markets,” they wrote. “We could see the recent rally extend a bit further on ok/good macro data and additional degrossing, but then weaken if the recent buying fades.”

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.