Applying the Actuarial Process to Retirement Planning

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

This article is a follow-up to my September 2015 article, Think Like an Actuary to Become a Better Advisor. I will describe the general process used by actuaries to maintain financial sustainability, to encourage advisors to employ this same process to their client’s retirement planning. For illustrative purposes, I will briefly outline how this process is applied by the Social Security system.

General actuarial process

The general process utilized by actuaries to maintain a financial system’s sustainability over time has six basic steps:

- Make reasonable assumptions about the future (generally deterministic, not stochastic).

- Calculate present values of assets (including future sources of income) and liabilities (balance sheet) based on relevant demographic information, system provisions and assumptions made.

- Periodically (generally annually) compare estimated present values of assets to liabilities to determine the system’s funded status (snapshot comparison).

- Maintain a history of the system’s funded status over time and note trends.

- When warranted or required, make changes to assets or liabilities (or both) to restore desired funded status (and/or to address possible cash flow issues).

- Periodically evaluate/stress test assumptions to see if they need to be changed or to assess risk.

This is a self-correcting process. If explicit or implicit assumptions about the future turn out to be incorrect, the system will incur actuarial gains or losses and the system’s funded status will either deteriorate or strengthen. Monitoring the pattern of such increases or decreases will enable stakeholders to either change assumptions about the future and/or make necessary changes to their system.

This is an ongoing process. The process does not end when changes are made to restore a system’s funded status to its desired level as described in step 5. Actuaries (or others) who employ this process for a financial system should take reasonable steps to make sure that stakeholders understand that achieving the desired funded status is a temporary (snapshot) measure of solvency based on assumptions about the future that, in all likelihood, will not be accurate. Therefore, it is quite likely that future system changes (in assets and/or liabilities) to maintain the desired system funded status may be necessary1.

Illustration – Application of the general actuarial process to Social Security financing

Rather than include an illustration in this article of how the general actuarial process would apply to a client’s personal retirement system (plan), I have chosen to illustrate how it applies to Social Security, as there is a wealth of historical information about the system, and Social Security reform is a hot topic for advisors and their clients. The illustration below refers to the process steps as numbered above:

Step 1 – The Board of Trustees of OASDI selects the deterministic assumptions about the future used to measure the system’s funded status. The chief actuary of the SSA must annually certify that the assumptions used to evaluate the actuarial status of the system are both individually and in the aggregate reasonable for such purpose.

Steps 2 and 3 – The present values of system assets and liabilities are annually determined under three alternative sets of future assumptions (optimistic, intermediate and pessimistic.) These values and the difference between system assets and its liabilities (unfunded obligation) under the intermediate set of assumptions is summarized in Table IV.B6 of the 2023 Trustees Report entitled, “Components of 75-year Actuarial Balance and Unfunded Obligation under Intermediate Assumptions.” The measure of the system’s long-range financial status is referred to as the system’s long-range actuarial balance (or long-range actuarial deficit). In this year’s report, this value was -3.61% of taxable payroll. If system assets were simply divided by system liabilities, and the difference not expressed as a percentage of the present value of future taxable payrolls, the system’s measured funded status as of January 1, 2023, based on the intermediate assumptions, would have been 79.3%

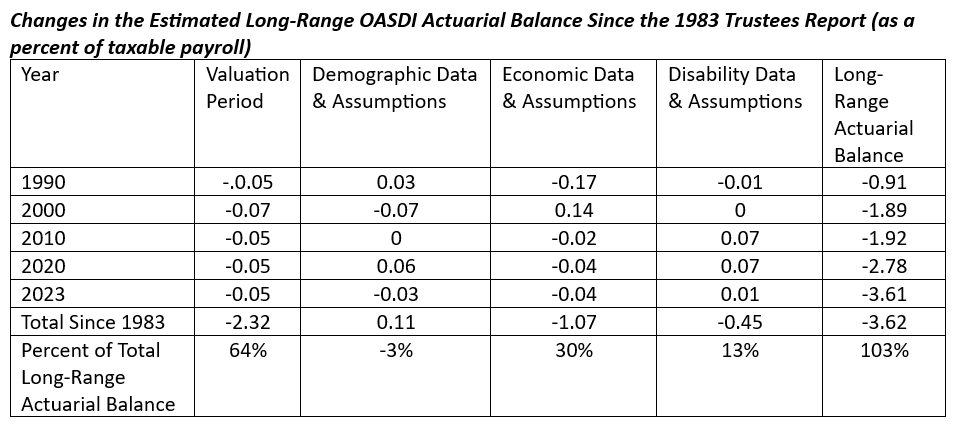

Step 4 – The Office of the Chief Actuary at the SSA annually summarizes the changes in the system’s long-range funded status in Actuarial Note Number Year.8 (This year is 2023.8). This actuarial note is entitled DISAGGREGATION OF CHANGES IN THE LONG-RANGE ACTUARIAL BALANCE FOR THE OLD AGE, SURVIVORS, AND DISABILITY INSURANCE (OASDI) PROGRAM SINCE 1983. This fascinating and frequently ignored document breaks down the sources of the system’s funded status deterioration since 1983, when it was last placed into actuarial balance. It is essentially a gain/loss analysis by source for the system, and it is significantly briefer and easier to read than the annual Trustees Report. I’ve excerpted results for several years and totals from Table 1 of this years’ actuarial note below.

The key takeaways from exhibit 1 of this actuarial note include:

- The system’s funded status (long-range actuarial balance) has declined fairly continuously over the past 40 years.

- Of this decline, 64% is attributable to annual changes in the valuation period (discussed in more detail below), while about 30% of the decline is attributable to economic data and assumptions.

- Demographic data and assumptions, which is frequently cited as a major factor in the system’s funded status decline since 1983, has had a small positive effect.

- Even if all assumptions are realized in the future, the system’s funded status is expected to keep deteriorating under current law because of the annual change in “valuation period” (or valuation date creep).

- Actuarial Note Number 2023.8 serves as an excellent history of the system’s funded status over time, and the trends it highlights are easily seen. Because the system’s funded status is measured over a 75-year period, the shortfalls expected after the end of the 75-year period under current law are ignored until subsequent years’ valuations. This approach implicitly assumes that annual system income will be equal to annual system outgo for years after 75. As shown above, this implicit assumption has produced cumulative actuarial losses for each year since 1983, which have resulted in most of the system’s funded status decline. The effect of this questionable implicit assumption is to overstate the systems’ actual funded status under current law.

Step 5 – Under current law, Congress decides when (and what) changes are necessary to strengthen the system’s financing. There is no requirement under current law for system changes to be made automatically to maintain the system’s actuarial balance. Further, there is no requirement under current law for reform changes to restore the system’s long-range actuarial balance, but congressional action in the past has generally also restored the systems’ actuarial balance. Most experts agree that changes are required at this time (or are perhaps long overdue) to strengthen system financing.

Step 6 – The Office of the Actuary and outside commissions of experts frequently consider the reasonableness of assumptions used to determine Social Security’s funded status, and assumption changes are frequently made. In addition to running three sets of assumptions about the future each year, Social Security actuaries also perform stochastic projections of system cash flows.

Part of their periodic analysis of assumption reasonableness presumably focuses on sources of significant experience gains and losses. But despite incurring large cumulative losses with respect to the implied valuation data assumption discussed above, this implied, and arguably unreasonable, assumption has not been changed.

Summary

The process employed to maintain a system’s sustainability over time can be more important than the assumptions and tools used to project future experience. Therefore, I encourage advisors to utilize the general actuarial process (or something similar) on an ongoing basis when consulting with their clients about retirement finances. If advisors need help with selecting reasonable assumptions about the future or with calculations of present values of household assets or spending liabilities, they can consult the spreadsheets I make available for free on my website.

As discussed above, advisors who use this process should take reasonable steps to make sure that their clients understand that achieving their desired funded status is a temporary (snapshot) measure of solvency based on assumptions about the future that likely will not be accurate. Therefore, future system changes (in assets and/or liabilities) to maintain the desired system funded status may be necessary.

Ken Steiner is a retired actuary with a website entitled "How Much Can I Afford to Spend in Retirement?"

1So, for example, if Congress adopts changes in Social Security’s tax rates or benefit levels (or both) to restore its actuarial balance (temporary solvency), this action should not be considered as “fixing” the system, and the package of changes should not be considered as a “solution” to Social Security’s funding problem. It should be considered as changes designed to strengthen the system’s financing based on (hopefully) reasonable assumptions used to measure the system’s funded status. The success of any system reform will depend on how well the assumptions made about the future compare with actual future experience, and there will be no guarantee that the reformed system will remain in actuarial balance for any specific number of future years following such action.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All