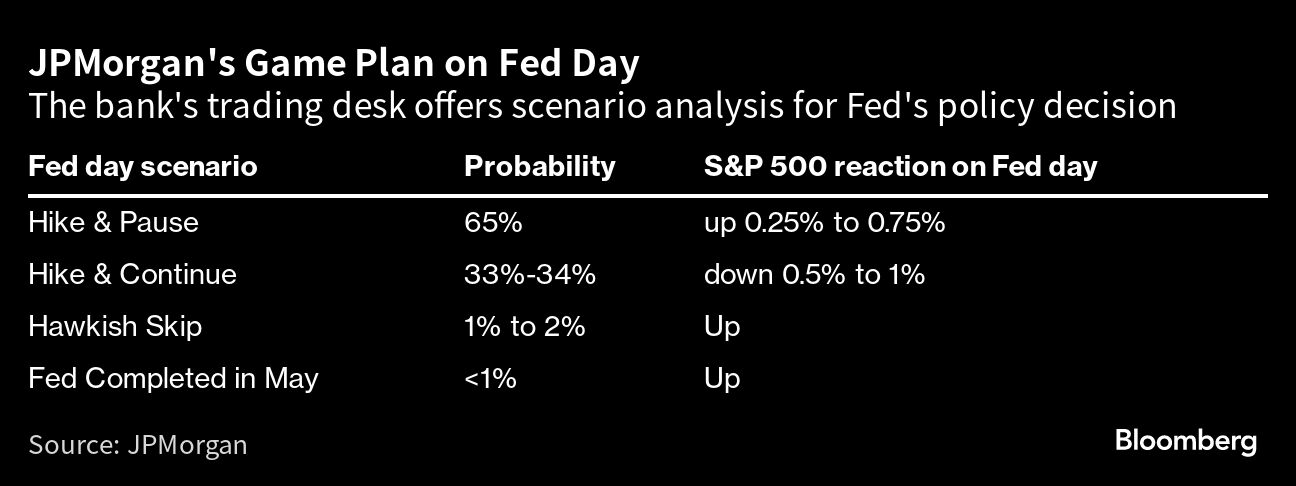

The likeliest outcome of Wednesday’s Federal Reserve announcement is also one that is apt to lift stocks, JPMorgan Chase & Co.’s trading desk says.

An interest-rate hike plus statements suggesting policymakers will hold off at their next meeting could push the S&P 500 as much as 0.75% higher, says the team including Andrew Tyler.

The team assigns a 65% probability for the central bank to raise interest rates this time and then stop. The odds, the team says, are almost twice as high as the other scenario where the Fed keeps tightening monetary policy in coming months.

“We think the Hike & Pause scenario is more likely with potential upside risks that the Fed may confirm the end of the cycle earlier at Jackson Hole,” the team wrote in a note, referring to the Kansas City Fed’s annual policy forum scheduled in late August. “Any language that the market interprets as the Fed may pause after one hike,” they said, citing as an example that disinflationary progress is moving faster than the Fed expected, “should support bonds and stocks.”

For investors who suffered a brutal cross-asset selloff in 2022 as the Fed embarked on its most aggressive inflation-fighting battle in decades, the prospect of the central bank approaching an end to its hiking cycle is welcome news. In this scenario, the JPMorgan team expects the S&P 500 to rise 0.25% to 0.75% during the session. Should the Fed stay on its hawkish path, they say, the index will drop as much as 1%.

Of course, no one can claim to have a crystal ball on the market, and the 2023 stock rally has shocked almost everyone. Moreover, with the second-quarter earnings season in full swing, the Fed may not be the only thing that matters. If anything, the JPMorgan analysis offers a glimpse into the risk that is at stake for investors.

That said, the team’s latest game plan around the inflation data was spot on. Before the release of June’s consumer price index, Tyler and his colleagues saw a four-in-five chance for the print to arrive in line or below the estimate, a range of outcomes that could bolster equities. The headline CPI came in weaker than expected, and the S&P 500 spiked to close the session 0.7% higher.

Not everyone shares the optimism. In a client survey conducted by 22V Research LLC, only about a quarter of the respondents see this Fed day boding well for risky assets. Almost one-third of them expect a risk-off reaction and 44% view it as a non-event.

Stocks have rallied this year in part on optimism that the Fed is almost done with its tightening campaign after a yearlong softening in inflation. While skeptics point to consumer prices still running above the central bank’s target as a reason for caution, equities have wiped out all their losses since the Fed began raising rates 16 months ago, with the S&P 500 now trading roughly 5% above where it was at the start of the hiking cycle.

There has been a growing acceptance among investors that the Fed has so far managed to avoid a recession while taming inflation. That acknowledgment underscores a sentiment shift where money managers are more relaxed on the downside risks and yet reticent to play for more upside, according to Tony Pasquariello, Goldman Sachs Group Inc.’s head of hedge-fund coverage.

“If you had asked at the outset of the cycle if this Fed could break the spine of core inflation without breaking the labor market or the major assets groups (stocks, housing, corporate credit), the odds would have looked very long,” he wrote in a note over the weekend. “I don’t think there’s much of a question there at this point.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Lu Wang