A Framework for Deciding Whether to Annuitize

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisors and investors wonder what role annuities should play in retirement planning. Here are the pros and cons of a common annuity product versus consuming out of invested wealth.

There is a bewildering assortment of annuity products. In this article, I analyze the pros and cons of a non-qualified, immediate, fixed-rate annuityi:

- Non-qualified means it’s purchased with post-tax dollars.

- Immediate means its payments begin right away.

- Fixed rate means that the annuity guarantees the annuitant a fixed rate over the life of the policy.

Consider a hypothetical retired couple – a 67-year old and his or her 63-year old spouse – who want to decide how much of their savings to invest in an annuity and how much of it to invest in a combination of stocks and bonds. How should they make this decision? What are the trade-offs involved and how can these be quantified?

Some numbers

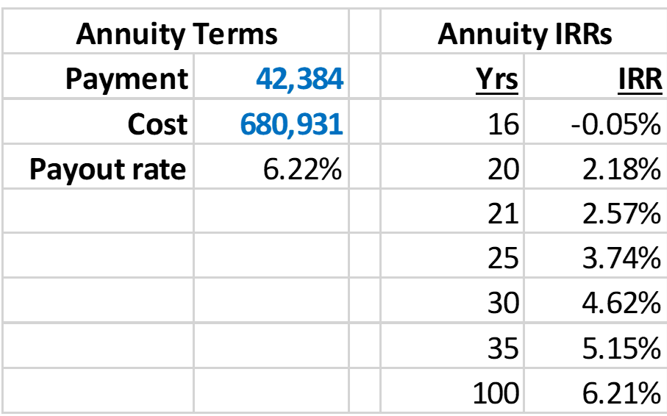

Assume that our couple wants to generate $3,532 in monthly income (which translates into $42,384 annual income). If the 67-year old is a male and a 63-year old is a female, as of June 2023, the approximate cost of this annuity is $680,931 according to the Schwab annuity calculator. This is “approximate” because the actual cost depends on the couple’s exact circumstances and health status, which the website estimate does not consider. The version of the policy I consider is called “joint life with cash refund.” This makes monthly payments as long as either spouse is alive and the minimum benefit paid is equal to the policy premium (i.e., if both annuitants pass away before the total policy payouts equal the premium, their beneficiaries will receive a lump-sum payment equal to the shortfall).

The $42,384 annual payout on a $680,931 premium translates to a payout rate of 6.22%. An important aspect of this structure is that, if the policy makes payments greater than or equal to $680,931, once both annuitants pass away, their beneficiaries will receive nothing from the annuity. The entirety of the annuity premium will then be gone from the estate. For comparison, at the time of this calculation, 30-year Treasury rates were at 3.82%, on an investment that will return its principal after 30 years of making the annual interest payments.

Is the annuity a good deal relative to outside options? One way to think about this is in term of the annuity’s internal rate of return (IRR). Think of the IRR as the implicit rate of return on the initial policy premium. The next table shows the annuity’s IRR as a function of how many years the surviving spouse will live.

The IRR of the annuity increases with the number of years during which it pays out. If the annuity pays out for only 16 years, its IRR is effectively zero because its payments will roughly equal the premium. If the annuity pays out for 20 years, its IRR will be 2.18%. If it pays out for 35 years, i.e., if the surviving spouse lives for 35 years after the start of the contract, the IRR will be 4.62%.

One way to gauge which IRR is relevant is to look at the Social Security Administration’s actuarial life expectancy table (these are only correct on average, and any given individual’s life expectancy depends on their circumstances and health status). For our hypothetical couple, the life expectancy of the 67-year-old male is 15.6 years while the life expectancy of the 63-year-old female is 21.2 years. If the annuity’s annual payments are received for 21 years, the above table shows that its IRR would be 2.57%. (Another nice tool for thinking about life expectancy is this longevity calculator.)

Which is better

From a pure IRR point of view, the Treasury’s 3.82% return will be roughly matched by the annuity if the longer-surviving spouse lives for 25 years. This comparison, however, misses a few important points:

- Annuities are not risk free, in the sense that the insurance company which provides the product has some chance of not being able to make its payments (though there are state guaranty associations which can step in, at least partially, if this happens). This annuity credit risk means that Treasury yields, which are effectively default-risk free, may not be the right benchmark. We can up the 3.82% Treasury yield to, maybe, 4.3% to reflect the additional annuity credit risk. This would take the annuity breakeven life span closer to 30 years.

- The annuity provides longevity insurance. If the annuitants live much longer than their expected life at the start of the policy, the annuity keeps on paying, thus guaranteeing an income stream for life (subject to insurance company credit risk). This insurance is clearly valuable to retirees, and the price of such insurance is the potentially lower IRR on the annuity.

- The payout profiles of annuities and investments in things like Treasury bonds differ in an important way. Even if an annuity and a Treasury investment have the same IRR, the annuity will produce larger annual payments because these payments will contain a partial return of principal, whereas the Treasury will return the principal only at the very end of the investment. The additional annual cash flows that are generated by annuities may be very important for many retirees.

Before we take a deeper dive into these differences in payment profiles, a brief detour on the tax implications of annuities is in order.

Taxes

The tax treatment of annuities is subtle. The philosophical underpinning of annuity taxation is that interest income on the annuity is taxed but the return of principal is not. Here, I go through an example to understand the broad mechanics of annuity taxation. Consider our hypothetical $680,931 annuity which pays $3,532 of monthly benefits for the life of the annuitants. This translates into $42,384 of annual income (our example closely follows this article but the numbers have been modified slightly). This is a non-qualified, immediate, fixed-rate annuity.

The IRS’s exclusion ratio rule says that the interest earnings of the annuity depend on the annuitant’s expected life at the start of the policy. If the life expectancy is 21 years, then the expected income the annuity will generate is $890,064 (21 x $42,384). Of this amount, $680,931 is a return of principal, and $209,133 is considered earnings. The exclusion ratio for this annuity will be 680,931 / 890,064 = 76.5%, which means that this much of each monthly income check is not taxed because it is considered a return of principal. Of the $3,532 monthly income this annuity will produce, $2,702.11 is considered a return of principal and is not taxed. Only $829.89 is considered income on which taxes are owed.

But should the surviving annuitant live longer than the 21-year expected life, then all of the additional income (i.e., the entirety of the $3,532 monthly income check) will count as earnings and will be taxable. In broad strokes, the tax treatment of an annuity is like that of invested wealth – principal is not taxed while earnings and capital gains are – and I will ignore the tax treatment of the annuity in the subsequent discussion. But the tax treatment of annuities is complex and you should consult a tax professional to analyze your particular situation.

Understanding the pros and cons

The IRR analysis I’ve conducted is incomplete because it does not consider the timing of cash flows. Let us consider the pros and cons for our hypothetical retired couple of allocating $1,000 of their savings to an annuity, with the rest invested in a stock/bond portfolio. This analysis requires a few assumptions:

- Our hypothetical retired couple will spend 3.5% of their invested wealth every year for non-discretionary consumption. This is similar to the often-discussed 4% retirement spending rule, which maintains that retirees can spend 4% of their savings every year in retirement without running out of money. In QuantStreet’s own analysis, it has found that a 3.5% annual spending rule is more conservative and it yields both a higher likelihood of not running out of money in retirement and also of allowing the post-spending wealth to keep up with the annual rate of inflation. (I will write more about this in an upcoming article.)

- Invested wealth grows at 4.3% per year. The reason underlying this assumption is that we would like to conservatively project what happens to invested wealth. In QuantStreet’s work on this topic, it has found that in simulations over a 30-year investment horizon, the one-in-five bad case outcome for either a 70/30 (i.e., having a risk level equal to a portfolio that is 70% in a diversified stock index and 30% in a diversified bond index) or an 80/20 stock/bond portfolio is an annualized return of 4.3%. There is a good chance that the realized return of either of these portfolios will be considerably higher over any 30-year period, but we are being conservative in our analysis.

- Any amount invested in an annuity will pay 6.22% per year as long as at least one of the annuitants is still alive. For purposes of my analysis, I will ignore the credit risk associated with the insurance company counterparty in our transaction. (Though, in practice, this is a very important part of your annuity investment decision.)

- Finally, I will ignore the impact of taxes, despite the important and subtle tax considerations involved with investing in annuities.

The all-wealth strategy

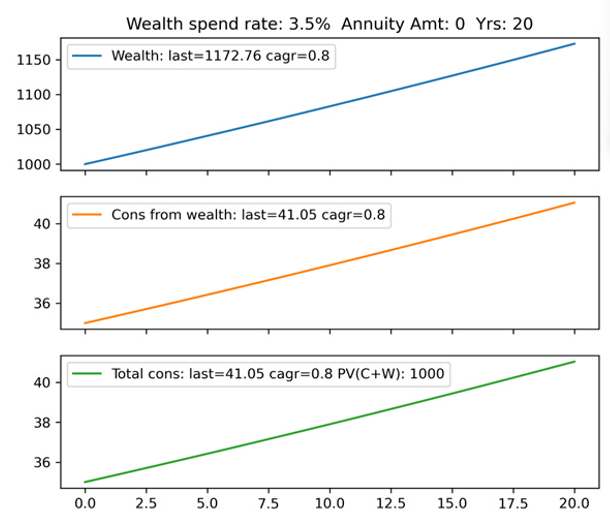

The first scenario I consider is what happens when the full $1,000 is invested in a 70/30 stock/bond portfolio, with zero invested in the annuity. The next figure traces out the growth rate of wealth, consumption from wealth (i.e., annual spending taken out of savings), and total consumption which also includes annuity income (zero in this case).

The initial starting wealth of $1,000 grows at 0.8% per year (4.3% assumed portfolio return minus 3.5% spent on consuming from wealth results in a 0.8% compounded annual growth rate, or CAGR). In 20 years, the $1,000 starting wealth will have grown to $1,172.76. Consumption from wealth starts at $35 and also grows at 0.8% per year since we always consume 3.5% of wealth (which is growing at 0.8% per year). Since there is no annuity income, total spending and spending from wealth are the same.

The initial starting wealth of $1,000 grows at 0.8% per year (4.3% assumed portfolio return minus 3.5% spent on consuming from wealth results in a 0.8% compounded annual growth rate, or CAGR). In 20 years, the $1,000 starting wealth will have grown to $1,172.76. Consumption from wealth starts at $35 and also grows at 0.8% per year since we always consume 3.5% of wealth (which is growing at 0.8% per year). Since there is no annuity income, total spending and spending from wealth are the same.

My final calculation is to determine the present value of all future cash flows from this strategy. In this spending-from-wealth strategy, we receive $35 in year 1, then a little more in year 2 ($35 x 1.008), a little more in year 3, and so on. Finally, after 20 years, we receive the remaining wealth level of $1,172.76. Discounting these cash flows back to today at 4.3% (the assumed return of the stock/bond portfolio) yields exactly $1,000! However, we structure our consumption plan, as long as all invested wealth earns 4.3% returns and we calculate the present value of future cash flows by discounting at 4.3%, we will get the present value of our future consumption and wealth to be equal to $1,000. This will serve as a placeholder for what comes next.

Investing in the annuity option

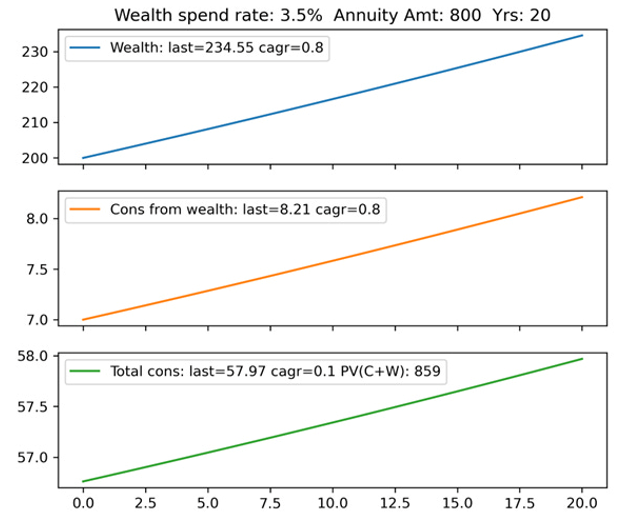

In the second version of the strategy, our hypothetical couple spends $800 of their $1,000 on an annuity, which pays 6.22% annual yield as long as one of the spouses is alive. The remaining $200 is invested as before, at a 4.3% assumed rate of return, and spending from this remaining $200 is assumed to happen at the same 3.5% annual rate.

The $200 of invested wealth grows at 0.8% per year as before. The 3.5% annual consumption from wealth starts at $7 (3.5% of $200) and grows at 0.8% per year. But now, the total consumption in year 1 also involves the annuity payment of $800 x 6.22% = $49.76. Total year-one consumption is $56.76 (the wealth consumption and the annuity income). This grows at a paltry 0.1% per year (bottom panel) because it combines two incomes streams: the $7 from wealth growing at 0.8% per year and the $49.76 payment from the annuity which is a fixed payment for the life of the policy.

The annual cash flow from the annuity option is much higher than from the all-wealth option ($56.76 versus $35 in year 1). But the all-wealth option will result in a projected wealth level of $1,172.76 after 20 years, while the annuity option, after 20 years, will be worth nothing if neither annuitant survives past that point. Applying the present value calculation – which discounts future cash flows at 4.3% – to the annuity option results in a value of only $859, considerably less than the $1,000 precent value of the cash flows from the all-wealth option. The higher cash flows during the annuity policy’s life span are not enough to outweigh the loss of principal at the end of the policy in a present value sense if the policy lasts only 20 years.

Generalizing the results

My analysis has projected forward only 20 years. But what if the life span of the annuity policy is longer? Or shorter? Also, what if the hypothetical couple chooses to invest an amount different than either zero or $800 in the annuity? To better understand how these factors impact the annuity-investing decision, I now repeat the analysis shown in the two figures above for many different combinations of annuity life span and annuity investment amount.

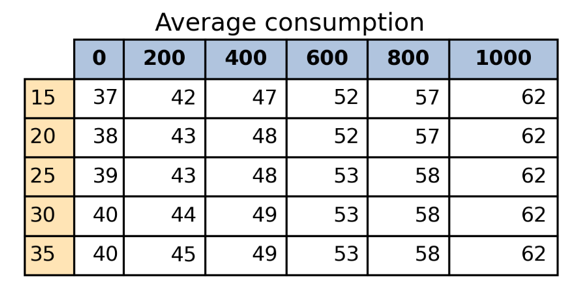

The next table shows the average annual consumption level (which includes spending from wealth and spending from the annuity policy) associated with an investment policy as a function of the numbers of years the policy will be in effect (along the rows) and the dollar amount invested in the annuity policy (along the columns).

The first column shows that keeping all of one’s money in the all-wealth option, i.e., zero annuity investment, results in the lowest average yearly consumption level (between $37 and $40 depending on how long the couple in our example lives). The all-annuity option results in an annual cash flow of $62, which is constant regardless of the time the policy stays in effect. Intermediate options – $200, $400, $600, or $800 invested in the annuity – result in average annual cash flows in between these two extremes.

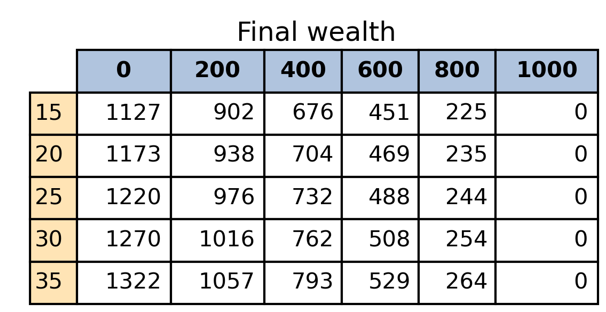

The flipside of the annual cash flow generated by a given annuity-life span combination is how much wealth will be left over at the end.

As the above table shows, with no annuity investment, the wealth remaining in the investment account can be as high as $1,322 if the longest surviving spouse lives 35 years after the policy’s start. In the case of an annuity, the amount remaining will always be zero. (The caveat is that some annuities have a minimum-benefit provision, as I already discussed.) Annuity levels between zero and the full $1,000 result in intermediate-wealth levels that are available for beneficiaries when the couple passes.

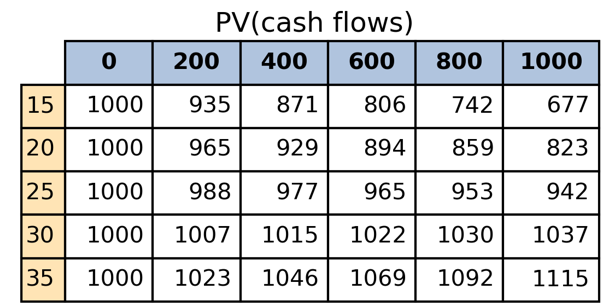

To determine which of these two effects – the higher annual cash flows or the higher residual (i.e., remaining) wealth amount – dominates, I calculate the present value of all future cash flows and the present value of the residual wealth resulting from the different investment policies.

The table above shows that, as already mentioned, the present value of all cash flows and remaining wealth from the zero-annuity policy is always $1,000, which is true by construction. Looking at the all-annuity policy, the present value of all future cash flows is below $1,000 if the term of the annuity is 25 years or less. At a term of 30 years, the present value becomes $1,037, which dominates the all-wealth strategy given my assumptions. At 35 years, the present value of the all-annuity option is $1,115.

For intermediate-annuity investments – between all-wealth and all-annuity – the present values of all future cash flows and wealth fall in between these two extremes. Choosing between the different wealth-annuity options is therefore part art, part science. The science allows for the quantification of the trade-offs, and the art involves deciding which set of trade-offs is most desirable for a given individual or family.

Making sense of everything

Deciding how much of one’s retirement savings to annuitize and how much to keep invested in a stock/bond portfolio is challenging with lots of nuance. For most people, discussing their options with a qualified financial advisor and a tax professional is the right thing to do. Making these decisions on one’s own requires a good deal of financial sophistication. A brief summary of the issues raised in my analysis follows:

- Buying an annuity transforms future wealth into current cash flows.

- The cash flows from an annuity will typically be higher than what can reasonably be sustained by spending from wealth, but the downside is that there is nothing left over at the end to pass to the next generation.

- The longer the life span of the annuitants, the more advantageous it will be to own an annuity.

- Annuities provide longevity insurance, but this insurance comes with a price. For most realistic life expectancies, the annuity option will have a lower IRR and a lower present value of future cash flows relative to the consume-from-wealth option.

- Those who want to leave something to their loved ones, or to their estate more broadly, need to consider options where some wealth is annuitized.

- The cost of this is that the annual cash flows they will generate from their wealth will likely be lower than with the annuity option, resulting in less spending in retirement.

- Finally, our assumption of 4.3% returns on a 70/30 stock/bond portfolio – which is our hypothetical wealth investment target – is a 1 in 5 bad case outcome over 30 years based on QuantStreet’s simulation studies. There is a decent chance that the actual outcome will be better than this, in which case my analysis of the non-annuity options is overly pessimistic.

A few caveats:

- A 70/30 stock/bond portfolio may not be appropriate for many retirees, so this is a discussion that you should have with a qualified financial advisor.

- Assuming a 4.3% return-on-wealth hides some important features of what retirement spending simulations can reveal. Again, a discussion with a financial professional may be helpful to elucidate some of these issues.

Harry Mamaysky is a professor at Columbia Business School and a partner at QuantStreet Capital.

i This is the same as a single-premium immediate annuity (SPIA).

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All