The story of US housing for hopeful buyers in 2023 has been one of frustration. A lack of supply has stabilized a market where affordability remains challenging.

Homeowners with low mortgage rates have chosen not to sell, putting builders of new houses in a stronger position than they had anticipated last autumn when interest rates were surging and the market slowed. While I wouldn’t count on supply conditions getting easy any time soon, there are growing signs that the picture in 2024 should be better, or at least “less bad.”

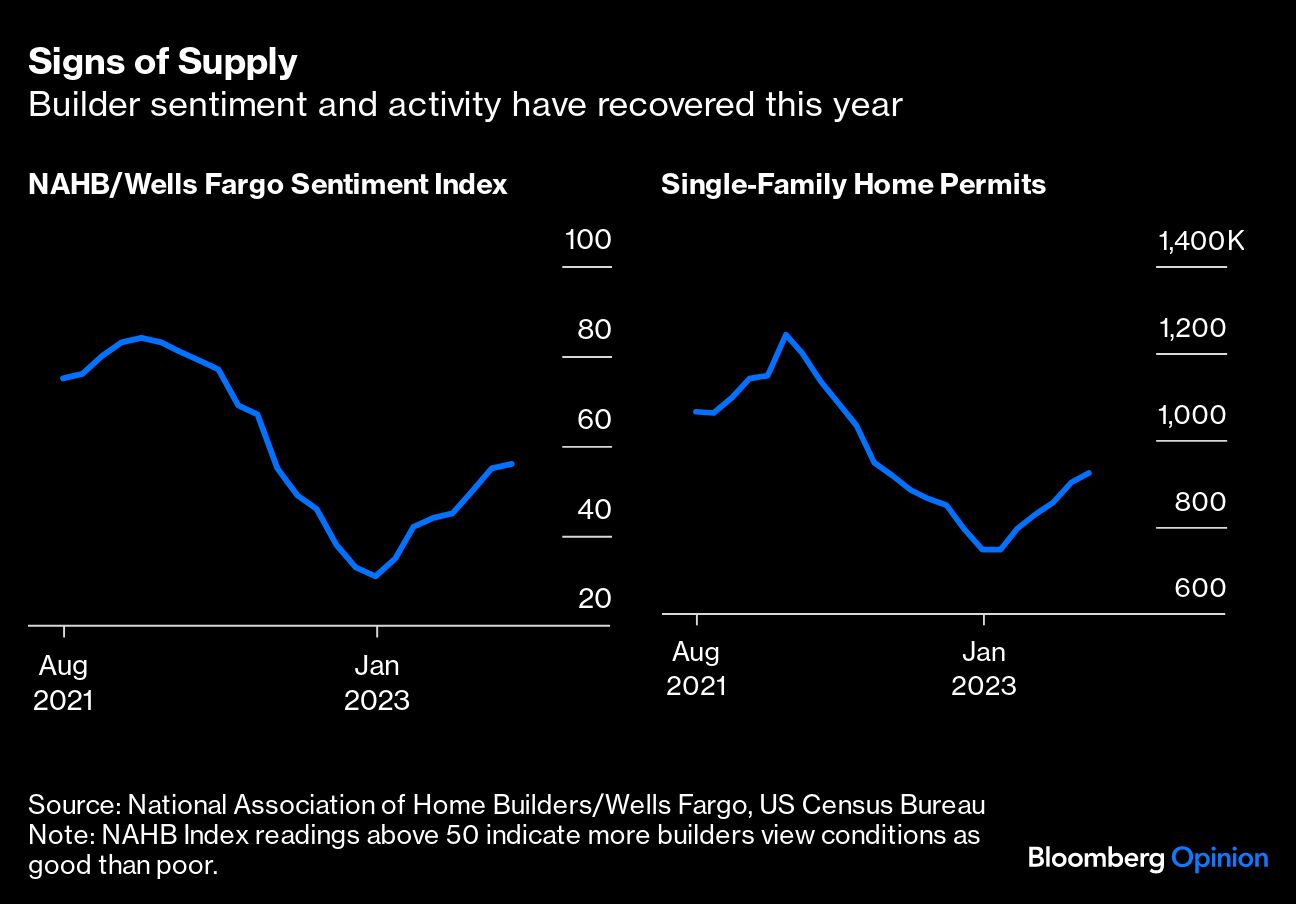

Let’s start with new homes. Builders braced for a challenging 2023 only to find that they were in some ways the only game in town in a supply-constrained market. Resilient prices have given the industry more confidence to increase production. A gauge of the market for new houses from the National Association of Home Builders and Wells Fargo, which measures sentiment on a scale from 0 to 100, surged from 31 in December — representing deep negativity — to 56, suggesting moderate optimism. Single-family housing starts have risen. Healing supply chains have shortened the time to build homes, meaning the ramp-up in construction that's underway should put more completed homes on the market by the first half of 2024.

The resale market, which historically accounted for about 87% of all homes for sale and has seen an acute lack of inventory, is where a pickup in new listings would be most welcome. To be clear, I’m not looking for a wave of fresh supply, but any growth right now would be helpful — something we should start to see early next year.

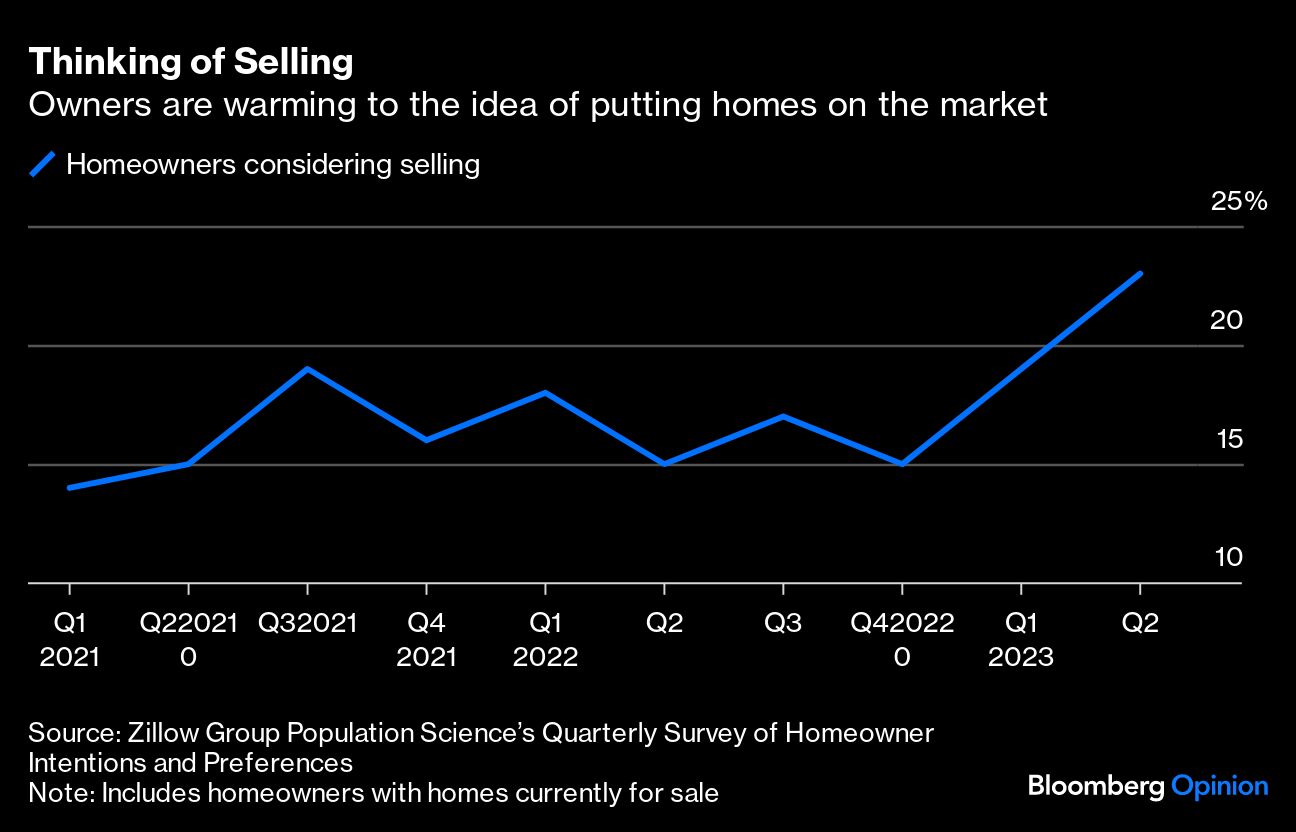

A quarterly survey from Zillow recently found that 23% of homeowners are already selling or considering selling over the next three years, the highest percentage since at least the beginning of 2021.

There are qualitative reasons why this would be the case. The first is that by October, mortgage rates will have been about flat year-over-year since 30-year mortgage rates first hit 7% last October. People with low mortgage rates may not be in a hurry to sell, but it's unlikely that they'll be less willing to sell this October than they were last October. Every month homeowners pay down a little principal on their home loans and get a little older. Incomes have risen, increasing their buying power. Life happens — kids age in and out of school, and people get married, divorced, and pass on. Any increase in resale supply from people with low mortgage rates may be modest, but 2023 should be the peak for the cheap mortgage lock-in effect.