The decision by Fitch to strip the US of its AAA credit rating, lowering it one level to AA+, means little in itself. There is next to zero chance the government won’t be able to pay its creditors and the Treasury Department’s access to funding is determined by forces far more fundamental than a few capital letters tied to a ratings report. That doesn’t mean the US’s rising debt burden isn’t a problem.

There are at least three ways in which increased federal borrowing could disrupt not just the US economy and financial markets, but the global ones as well. The first and most worrying is the potential for a so-called debt bomb. Under this scenario, the government’s debt burden -which currently stands at $32.3 trillion - becomes so great that even a small increase in interest rates means the Treasury needs to borrow just to cover the cost of servicing the debt. This leads to a vicious cycle, with the added borrowing discouraging buyers, driving interest rates higher, and forcing even more borrowing. The resulting sky-high interest rates throw the economy into a deep recession.

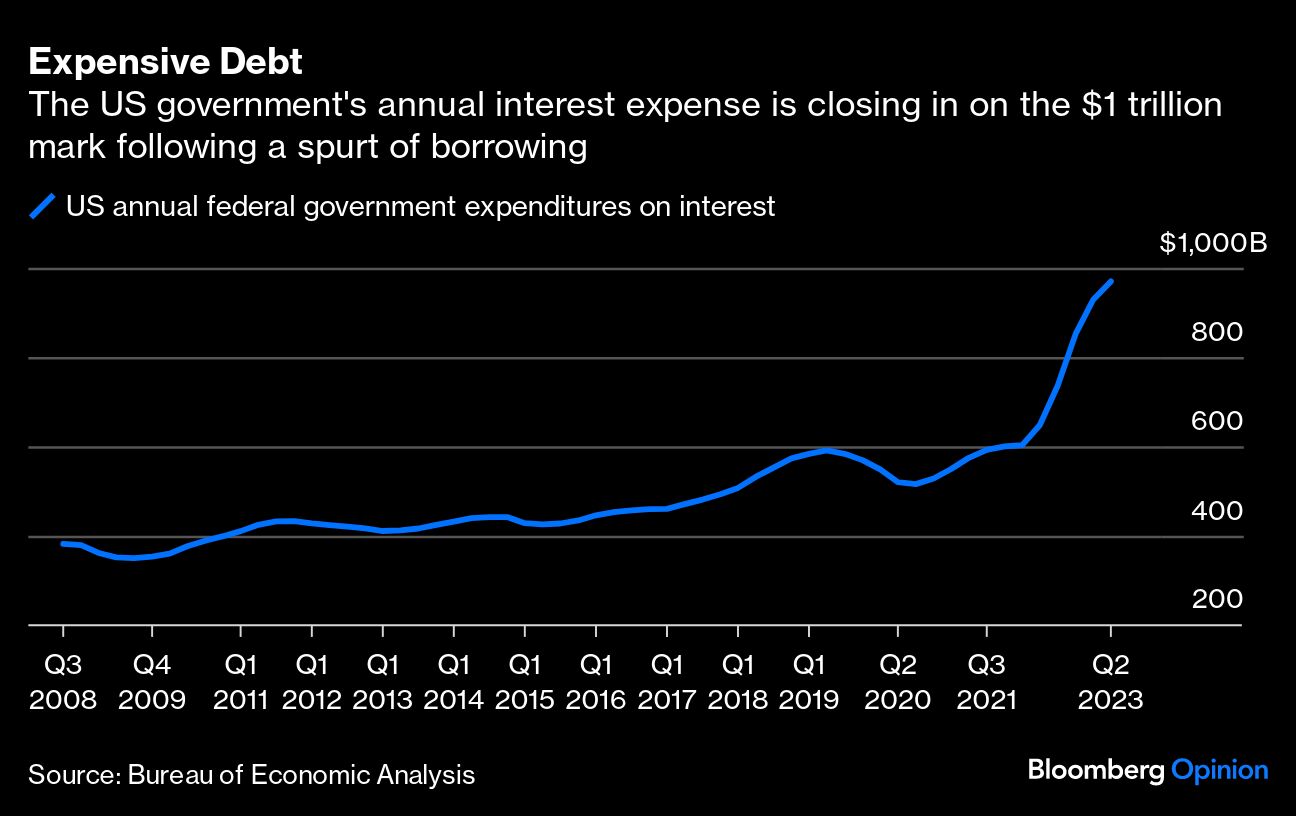

What’s concerning is that the US may be getting uncomfortably close to such a scenario. The Treasury is on track to spend almost $1 trillion on interest payments alone in fiscal 2023, compared with less than $600 billion before the pandemic and around $425 billion in 2011 when S&P lowered its rating for the US from AAA to AA+.

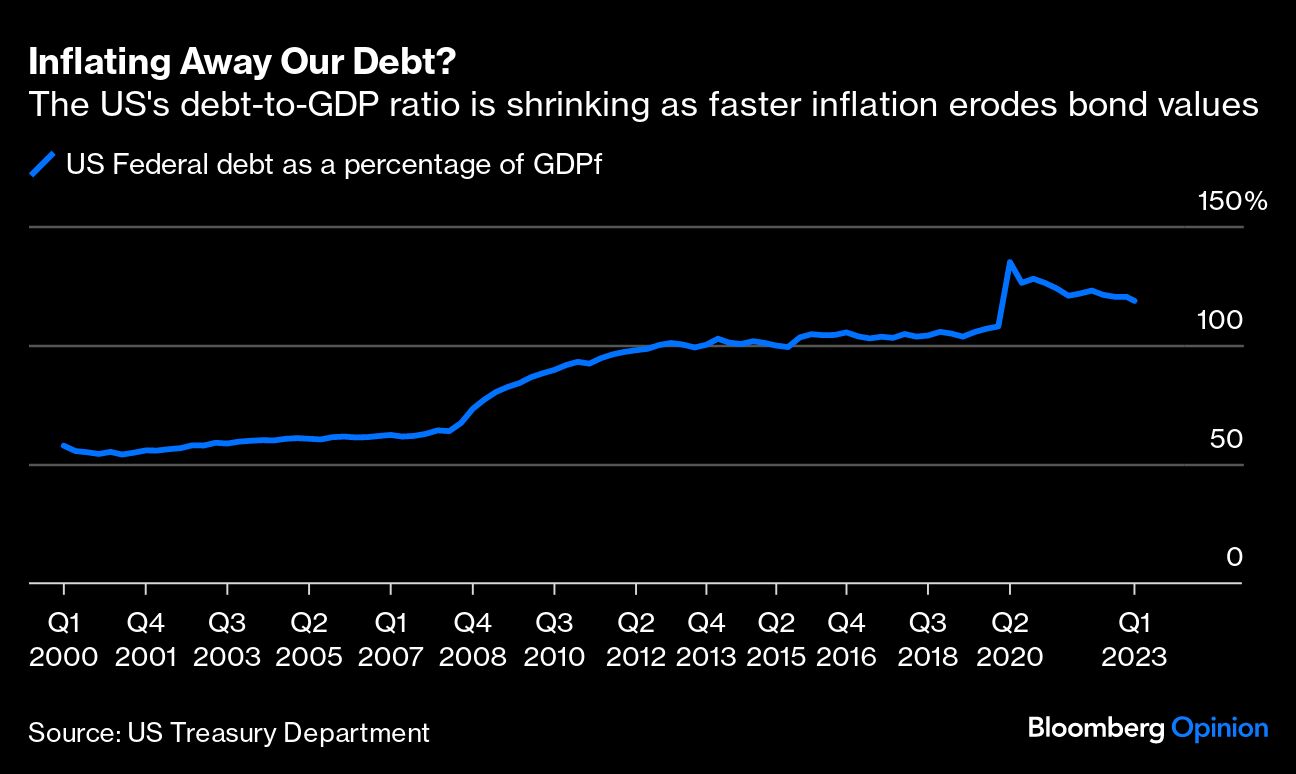

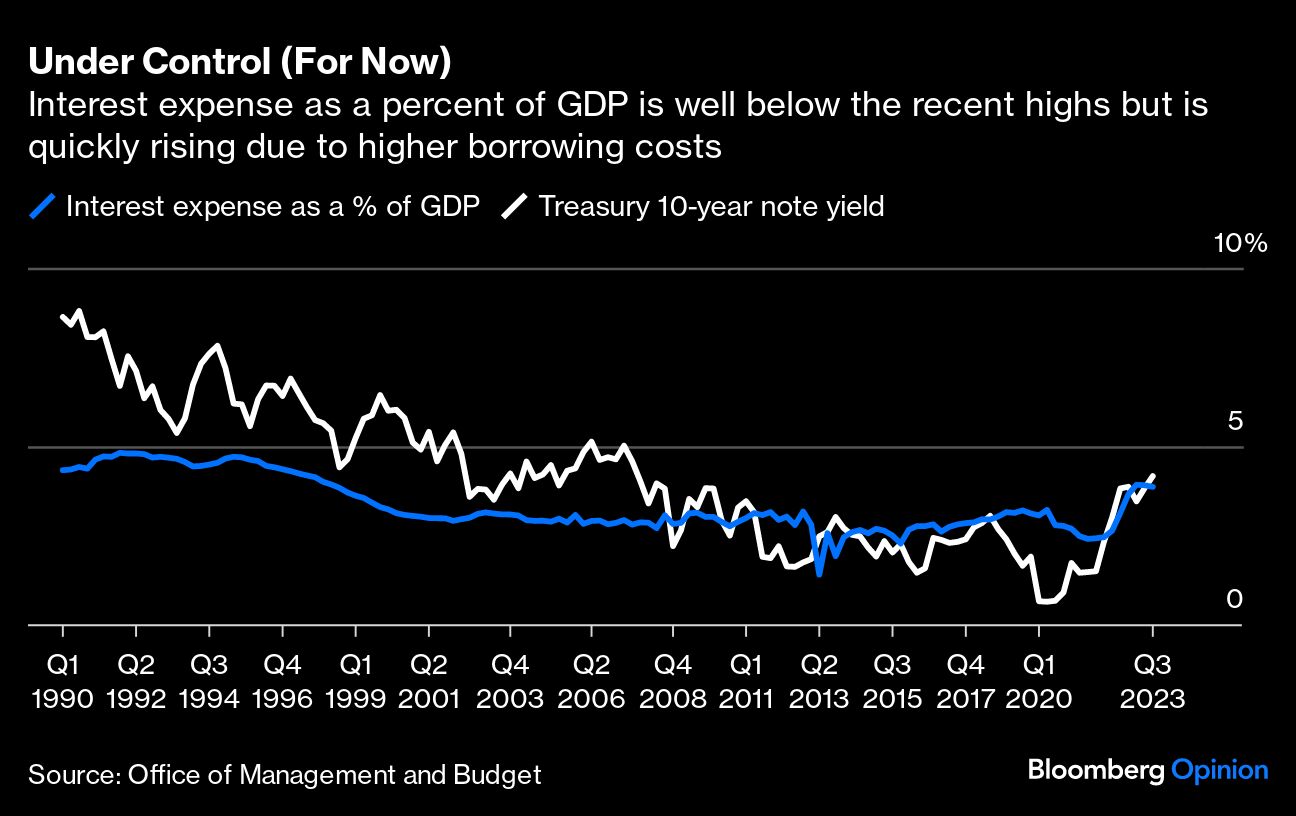

When I examined the potential for a debt bomb in February, the probability was low but quickly rising, based on debt service as a percentage of gross domestic product. Since then, that measure has remained stable, largely because elevated levels of inflation have inflated the nominal growth rate of the economy. This is what economists refer to as “inflating away your debt.” Such a mechanism works ideally in the short run but always comes back to haunt in the long run simply because of the pernicious effects of high rates of inflation over an extended period of time.

This leads to the second way in which unrestrained borrowing could lead to a crisis: the monetization of the debt. In other words, if traditional buyers of US debt went on strike, so to say, the government might resort to selling Treasuries directly to the Federal Reserve. This is different than the Fed’s quantitative easing program, where it bought Treasuries and related securities in the secondary market to inject funds into the financial system.

However attractive it may seem to the government as a way of financing itself, debt monetization is no free lunch. It leads directly to an increase in the monetary base, which then leads to more inflation. Such a policy could easily lead to a collapse in the Treasury market, which is the most important financial market in the world. So, sure, the government would see its debt-to-GDP ratio fall sharply, but only because of elevated inflation and massive losses for holders of Treasuries around the world. No Fed official has ever endorsed anything like monetizing the nation’s debt. And Fed Chair Jerome Powell has made it clear that low rates of inflation are the prerequisite for stable and sustained economic growth.

The third potential crisis stemming from too much debt is political. Recall that when he was president, Donald Trump - who polls show is the frontrunner to win the Republican party’s presidential nomination for the 2024 election - publicly criticized Powell for raising interest rates in 2017 and 2018 in an effort to keep inflation under control. So, it stands to reason that if Trump had his way, inflation rates would probably have been even higher and more sustained than they’ve been. This is significant because if elected, Trump will be responsible for appointing not just the next head of the Fed but filling any vacant seat of on the central bank’s Board of Governors.

Large and sustained budget deficits create an enormous incentive for any politician to appoint officials to the Fed that would do their bidding in the short term while leaving the fallout to the next administration. If such a political dynamic were to prevail, it might only be a matter of time before a debt bomb and debt monetization became a real possibility - ratifying Fitch’s decision.

A message from Advisor Perspectives and VettaFi: Just as artificial intelligence (AI) is helping advisors create videos, write blogs, construct portfolios and coach clients, companies throughout the world are using it to deliver more value to their clients. Learn about the future of AI and the investment opportunities it is creating at our next symposium, on August 30 at 11 am ET. Click here to register.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Karl Smith