A medieval king was nothing without his sage advisers. It’s not so very different in the Silicon Valley of 2023.

Elon Musk — officially, per Tesla Inc.’s corporate filings, the company’s “Technoking and Chief Executive Officer” — has just lost the man bearing the Game of Thrones-esque title “Master of Coin and Chief Financial Officer,” Zachary Kirkhorn.

In a business so indelibly associated with its chief executive’s antics, you might not think that would make much of a difference. But Tesla’s financial management under Kirkhorn since March 2019 has been crucial to its transformation from a basket case weeks away from bankruptcy into a disciplined and cashed-up manufacturer.

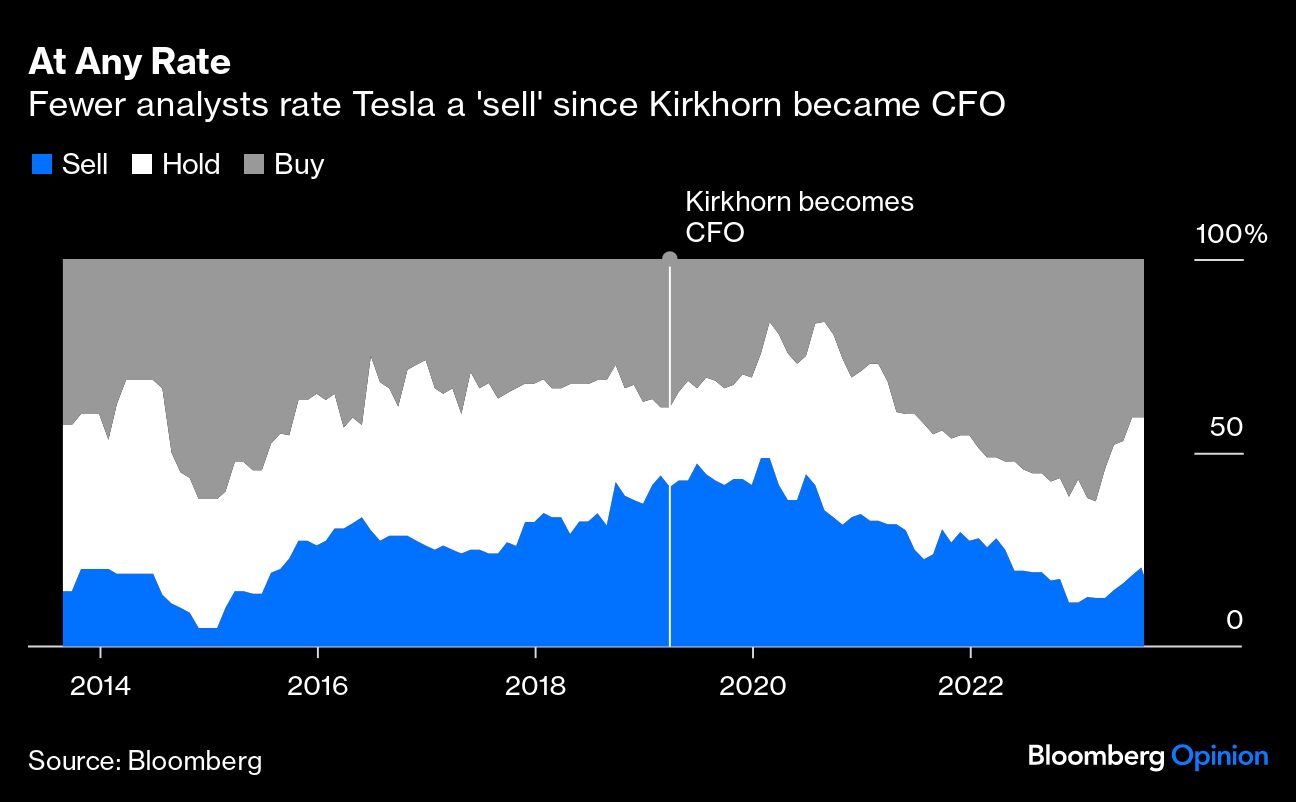

Over the past year, Tesla has withstood the storm of official interest rates rising by 5.25 percentage points just as capital spending was switching into ludicrous mode. Though the company’s sky-high valuation has fallen to an almost pedestrian 74 times forward earnings, investors haven’t been spooked. The share of analysts surveyed by Bloomberg with a “sell” rating on the stock fell to 11.4% last November, the lowest level since 2015 (it was 42% in March 2019 when Kirkhorn took on the CFO role). Though it’s ticked up to 18.4% since that’s been on the back of a 28% gain in the stock price.

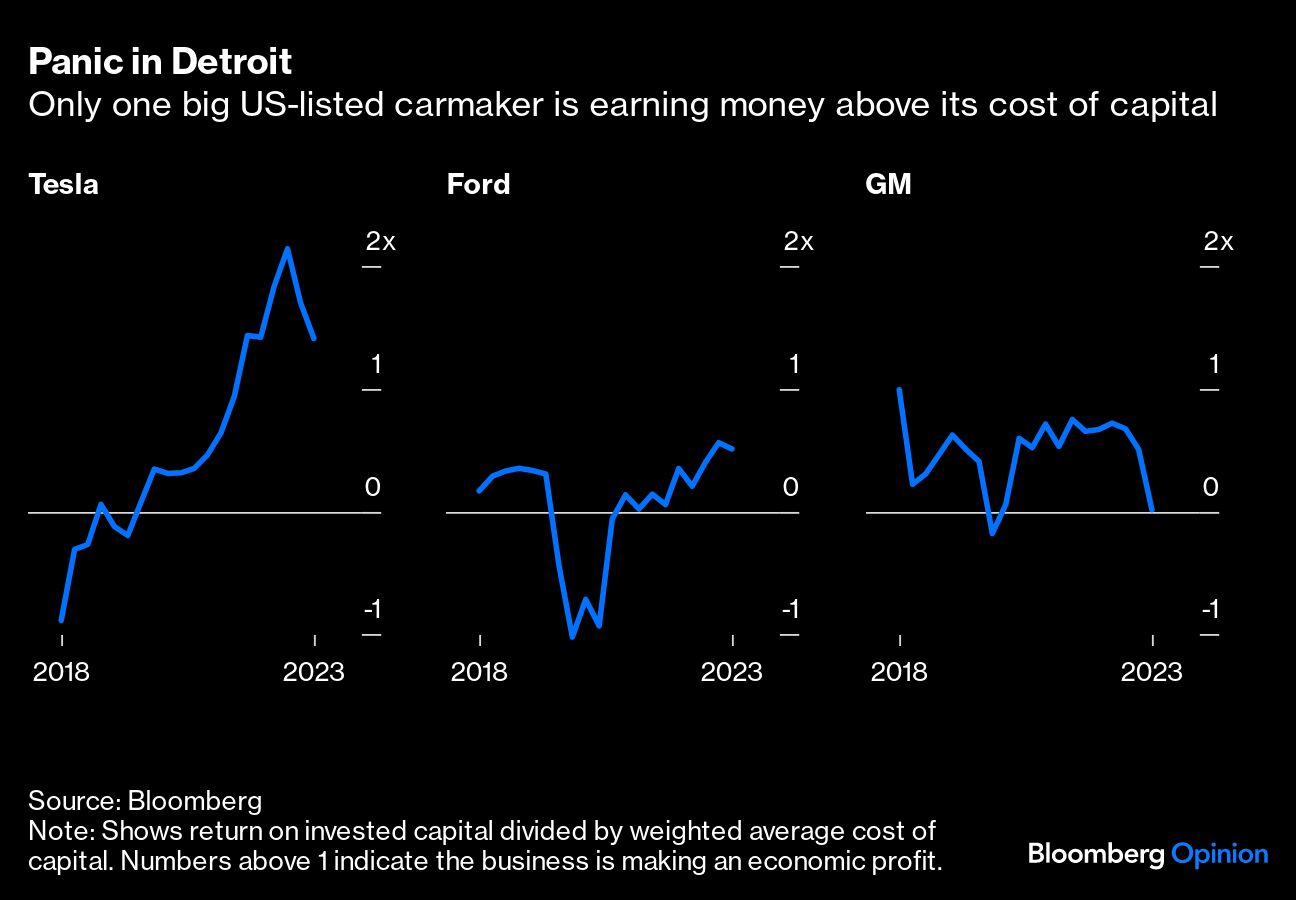

Their confidence has been backed up by solid financial management. Sales in the June quarter ran at 95% of working capital, outstripping General Motors Co. at 80% and Ford Motor Co. at 24% — evidence that Tesla is using its short-term assets as efficiently as any of its competitors. Return on invested capital is running comfortably ahead of funding costs, the only one of the three listed large US automakers to achieve that feat.

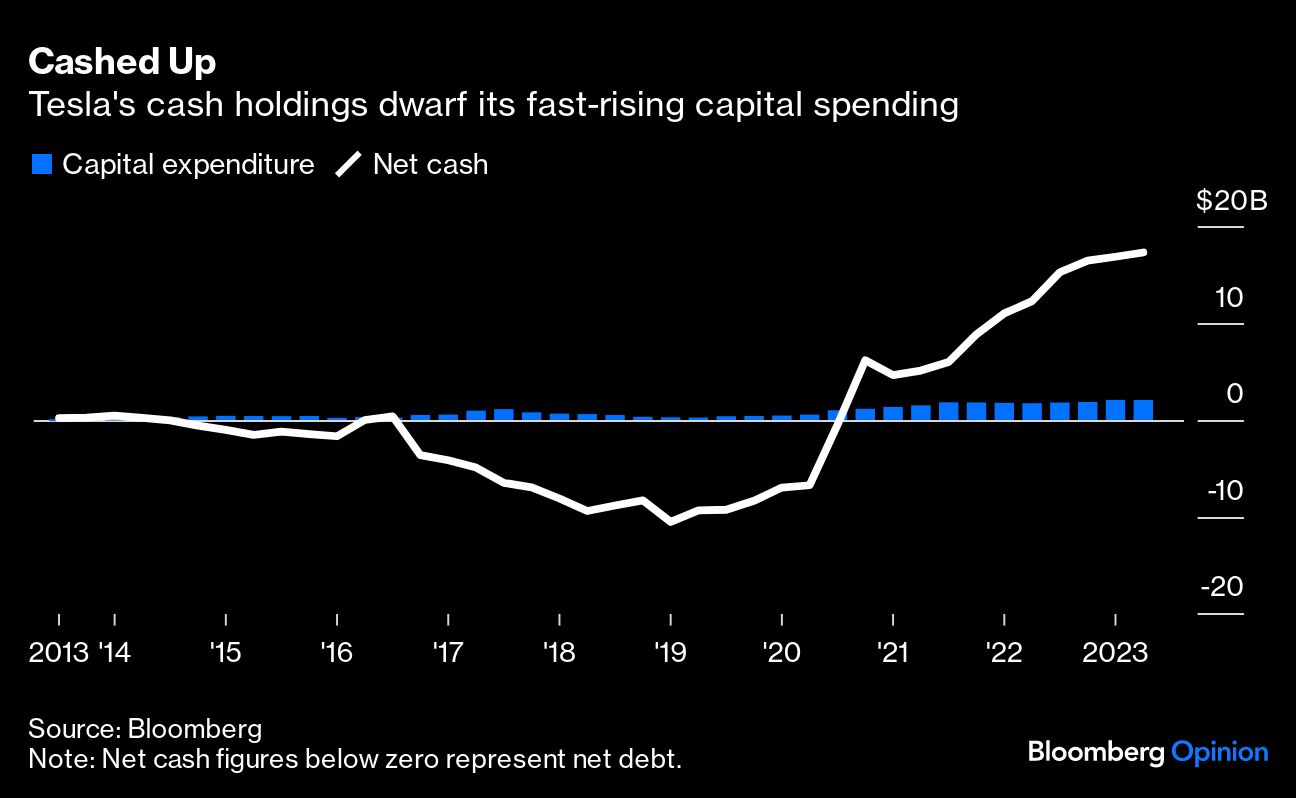

Capital spending is about $7.8 billion a year now, nearly six times the level when Kirkhorn started the job — but in contrast to that era, when expenditure was funded almost entirely by debt, it’s now backed by a $17 billion cash pile. That buffer started to accumulate, with exquisite timing, just before the Federal Reserve began lifting interest rates last year, making cash on hand a much more attractive way to finance growth.

The optimistic take on Kirkhorn’s departure is that his successor, former Chief Accounting Officer Vaibhav Taneja, was cut from similar cloth. Neither man had a prominent role before being elevated to the CFO job. Both had backgrounds in consulting before putting in time working deep in Tesla’s financial engine room. Taneja, if anything, is older and has a longer track record — he’s been Chief Accounting Officer ever since Kirkhorn, unknown at the time, was appointed as CFO.

A more pessimistic view comes from asking why exactly Kirkhorn should be leaving. Though his time with the company has given him a $590 million fortune, he’s been with Tesla for 13 years — the vast majority of his 17-year working life. The boss’s inability to focus, moreover, had left him as de facto chief executive officer. The official statement gives no clue, aside from the information that he stepped down on Aug. 4 and would stay until the end of the year to support the management transition. A post to Kirkhorn’s LinkedIn page is equally uninformative.

At a business with decent corporate governance, such transitions shouldn’t cause upsets. The departure of senior executives should be telegraphed months in advance, with handpicked successors lined up to take their places. At Tesla — whose eight-person board includes Musk’s brother Kimbal, long-time Silicon Valley associates such as Ira Ehrenpreis and Jeff Straubel, and, for some reason, James Murdoch — things are far less predictable.

Taneja might be able to repeat Kirkhorn’s trick of keeping Tesla humming while Musk distracts himself with cage matches against Mark Zuckerberg, SpaceX launches, and crude jokes on social media. Or he might not. There’s simply no way for outsiders to know.

One thing is certain, however: Musk has far more toys to grab his attention than he did four years ago. Neurotechnology business Neuralink Corp., artificial intelligence startup xAI and satellite internet platform Starlink were all in their infancy or didn’t exist when Kirkhorn took over, while Twitter Inc. was a leisure distraction rather than a suck on management time.

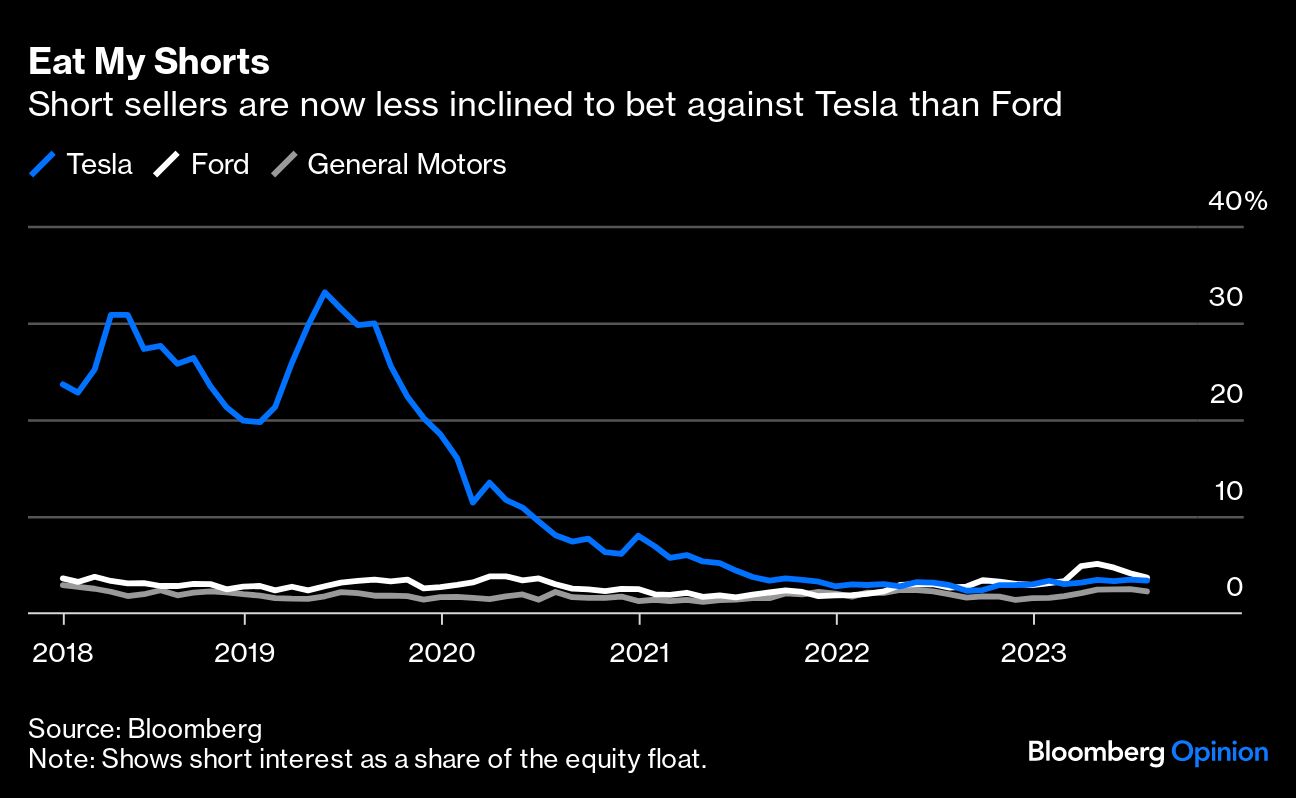

Short sellers have moved on, with just 3.4% of the equity float on loan to them — a smaller proportion than at Ford. Kirkhorn leaves Tesla in good shape with a clean maintenance record. If Taneja can prevent his erratic boss from seizing the wheel, it still has a smooth ride ahead.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by David Fickling