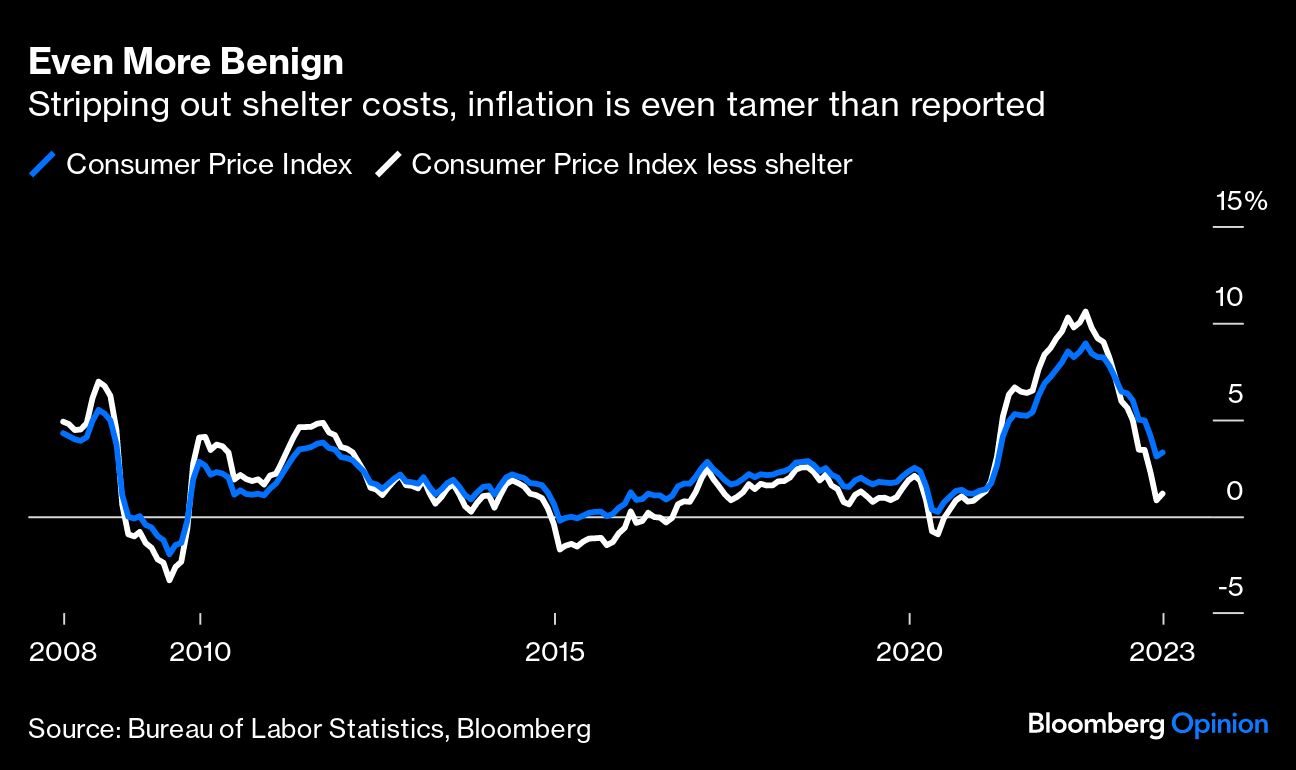

The consumer price index report for July showed the smallest back-to-back monthly increase in two years. This is welcome news in the battle to tame inflation but the even better news was buried deep in the report. There, it was revealed that rising shelter costs accounted for a whopping 90% of the increase in the CPI. Why is that good? Because the category is notoriously out of date and most likely already in decline, making the moderate inflation data even more benign in reality.

Let’s start with what shelter costs are and how they are measured. The Bureau of Labor Statistics calculates this metric - which accounts for about a third of CPI – by looking at changes in actual rents and something called owners’ equivalent rent. That second part is essentially a survey-informed assessment of how much homeowners think they could get by renting their homes.

What this all means is that a backward-looking metric is what’s driving the CPI numbers. How so? We know that the rents landlords are asking for new leases are already in decline. It takes a while for the drop to impact the data as most tenants have one- or two-year leases. A recent report from the Federal Reserve Bank of San Francisco suggests that shelter-cost inflation peaked around April at around 10% on a year-over-year basis. As more leases turn over that rate should continue to drop through the rest of this year and into 2024, reaching zero in May, according to the report. Indeed, more timely data from private sector sources such as Apartment List already show a year-over-year decrease in rents!

This is undeniably good news for the economy because it means the Federal Reserve may not need to raise interest rates again to get inflation back down to its 2% target, or about half of what it is currently. And no more rate increases boost the odds that the economy avoids a damaging recession that puts millions of Americans out of a job. At the least, Bloomberg Economics says the Fed can avoid hiking rates when policymakers next meet in the second half of September.

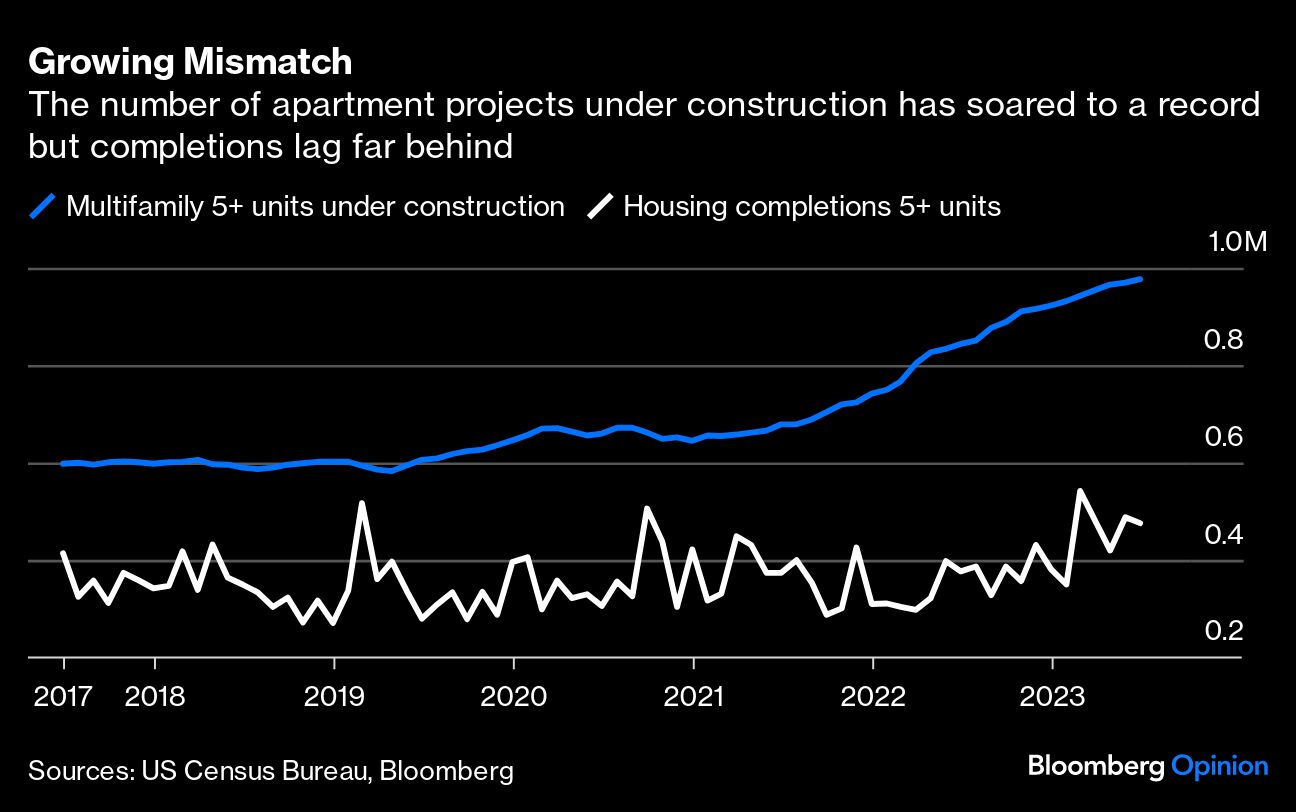

There are two important caveats to consider. First, even though inflation has moderated, prices of goods from food to cars to housing remain elevated. The National Association of Realtors said Thursday that its quarterly Homebuyer Affordability Index fell to a record low in the period ended June 30. Second, the expectation that future rents will decline is driven in large part by more supply coming online. At just under a million units, multifamily housing starts are at a record high, having soared from around 600,000 units before the pandemic. But actual completions have lagged well behind, perhaps due to developers deciding borrowing costs are too steep to make finishing the projects profitable.